FED: US TSY 17W BILL AUCTION: HIGH 3.625%(ALLOT 11.83%)

Apr-15 15:32

* US TSY 17W BILL AUCTION: HIGH 3.625%(ALLOT 11.83%) * US TSY 17W BILL AUCTION: DEALERS TAKE 42.05% ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

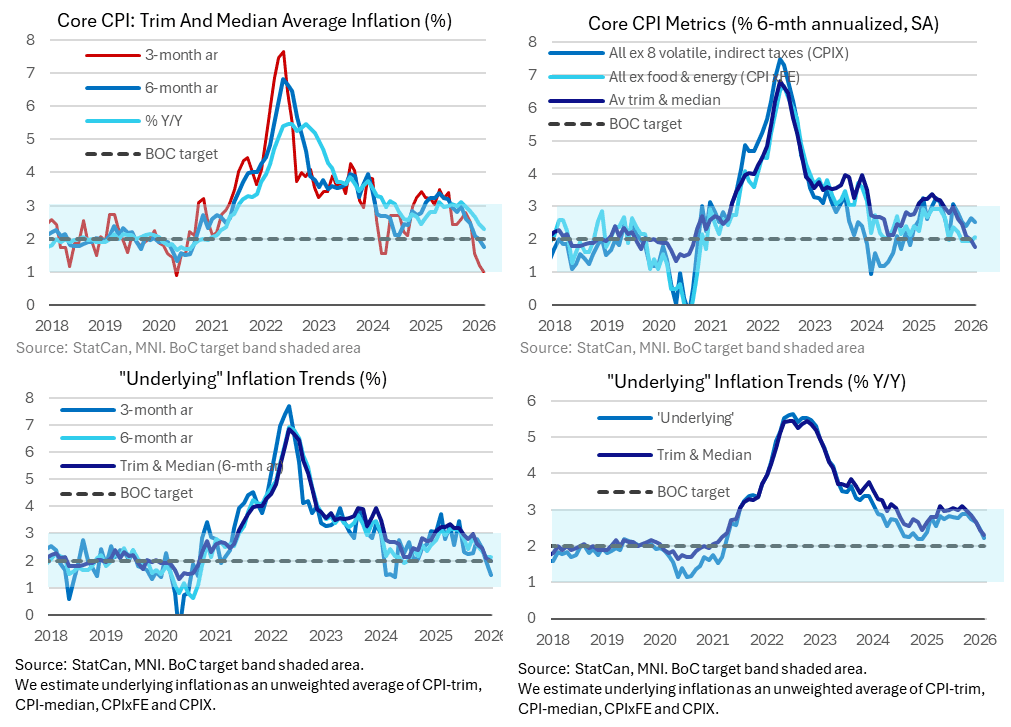

CANADA DATA: BOC May Acknowledge CPI On The Soft Side, Eyeing Downside Risks

Mar-16 15:31

A below-expected set of inflation data in February applied some downward pressure to the expected Bank of Canada rate path, but only in limited fashion. Cumulative hikes through end-2026 resolved steady at 35bp after a brief dip to the low 30s post-CPI release, though expectations appear to be capped for now in the low-40bp area seen late last week. The timing for the first 25bp hike however looks more decisively an October prospect, with September pricing down to 15bp after closer to 20bp pre-release.

- As such the overall hiking bias has held in, but the report won't affect immediate BOC rate move prospects at all. The BOC had already sounded fairly sanguine on the inflation front, agreeing that it was "evolving as expected" as of the January meeting.

- That said, for the BOC, there may have to be an acknowledgement at Wednesday's meeting that CPI is tracking on the soft side the January Monetary Policy Report projections. Through the first 2 months of Q1, headline CPI Y/Y is averaging 2.04% vs the MPR's 2.0% expectation, but the 2.5% core (trim/median average) projection looks set to be breached to the downside (averaging 2.38% so far). Overall, core run rates are between the middle-to-bottom ends of the BOC's range.

- What will bear most attention on this front this week however is how the BOC sees upside risks to inflation from the geopolitically-induced energy price spike from March onward.

- Additionally, the January deliberations noted in its risks to outlook from trade disruptions/structural economic adjustments that "while spillovers to other [non-directly-trade-related] sectors remained limited, production and employment could still decline more sharply than expected, weakening the broader economy and putting downward pressure on inflation".

- Labour market reports like February's very weak and broad one could be perceived as a preliminary signal that the downside risks are indeed materializing, particularly when placed alongside signs of weakening underlying inflation dynamics in the month.

- Heading into the meeting, our reading of analysts' previews points to broad consensus that the BOC will be able to look through any near-term pickup in headline inflation as a result of higher energy prices (and a Y/Y boost implied from energy base effects from April 2025's removal of consumer carbon taxes).

- It's probably too early for Governing Council to make a decisive assessment on this front, and they'll probably say so Wednesday. But the degree to which it emphasizes the perceived transitory nature of higher Y/Y inflation in the months ahead could be telling as to whether the market's expected bias toward hikes this year should be dampened somewhat on account of recent data.

US TSY FUTURES: BLOCK: Jun'26 5Y Sale

Mar-16 15:28

- -5,000 FVM6 108-22.75, sell through 108-23 post time bid at 1120:00ET, DV01 $222,000.

- The 5Y contract trades 108-23.25 last (+8)

EGB OPTIONS: Large Bobl Call Fly

Mar-16 15:23

OEK6 116.75/117.25/117.75c fly, bought for 7.5 in 10k.