GLOBAL: US Treasury Secretary to Meet China Vice Premier March 15-16

- "On March 15-16, Secretary of the Treasury Scott Bessent will meet with Vice Premier He Lifeng of the People’s Republic of China (PRC) in Paris, France."

- “Thanks to the bonds of mutual respect between President Trump and President Xi, the trade and economic dialogue between the United States and China is moving forward,” said Secretary Bessent. “Under the guidance of President Trump, our team will continue to deliver results that put America’s farmers, workers, and businesses first.” - (US Treasury Press Release)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Feb12 $1.1750-60(E2.1bln); Feb13 $1.1800(E2.7bln), $1.1850(E3.7bln), $1.1950(E2.2bln)

- USD/JPY: Feb12 Y154.00($1.3bln); Feb13 Y154.00($1.2bln), Y155.00($1.2bln), Y156.00($1.4bln), Y158.50($1.6bln), Y159.00($2.0bln), Y160.00($3.1bln)

- GBP/USD: Feb13 $1.3470-75(Gbp1.0bln)

- EUR/GBP: Feb13 Gbp0.8736-45(E1.0bln)

- AUD/USD: Feb13 $0.6800(A$1.6bln)

- USD/CAD: Feb13 C$1.3770-75($1.0bln)

- USD/CNY: Feb12 Cny6.9000($1.1bln); Feb13 Cny6.9000($1.2bln), Cny6.9700($1.2bln)

US TSY FUTURES: Revisiting Session Highs

Treasury futures are back at this morning's highs, trading desks note heavier buying, appr 30k TYH6 from 112-18 to -18.5, 112-19 last (+13). Extension higher would undermine the bear theme, focus on resistance at 112.-22, the Jan 7 high.

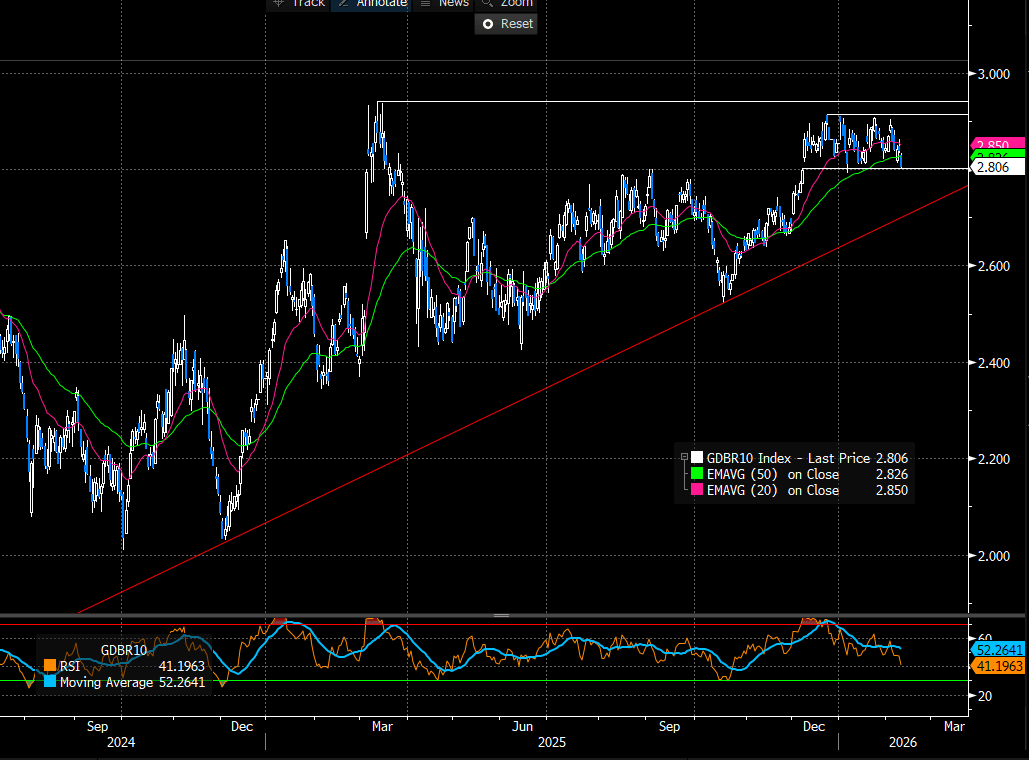

EGBS: 2.80% Contains Downside In 10-year Bund Yields

Downside in 10-year Bund yields has stalled a little around the 2.80% level, keeping the broad 2.80-2.90% range seen since the middle of December intact for now. Bunds face several cross currents this year, with well-documented domestic fiscal/issuance risks potentially offset by lingering geopolitical uncertainty and shifting investor demand patterns (e.g. away from 30-year maturities and towards the 10-15-year segment). Meanwhile, the ECB outlook is broadly steady, with rates set to be in a “good place” at 2% for some time.

- Today’s 3.5bp decline has come despite a heavy sovereign and corporate supply calendar (the EU’s E11bln dual tranche syndication has just priced). Bunds have largely taken cues from global peers, with JGBs stabilising overnight, Gilts benefitting from some near-term political reprieve and USTs supported by a soft retail sales report.

- Earlier today, we highlighted some analyst views suggesting CTA reaction functions were skewed towards fixed income buying, which may be another factor supporting the pullback in global yields.

- Tomorrow’s Eurozone calendar includes syndications from France (30Y) and Slovakia (20Y), alongside conventional issuance from Greece, Germany and Portugal. In data, the ECB’s latest wage tracker is released. President Lagarde noted in last Thursday’s press conference that “Negotiated wage growth and forward-looking indicators, such as the ECB’s wage tracker and surveys on wage expectations, point to a continued moderation in labour costs. However, the contribution to overall wage growth from payments over and above the negotiated wage component remains uncertain.”

- The US labour market report remains the primary global market focus tomorrow.

Figure 1: 10-year Bund Yields (Source: Bloomberg Finance L.P)