OPTIONS: US Options Roundup - 27 May 2026

May-27 19:41

Wednesday's US rates/bond options flow included: * SFRM6 96.3125/96.25 put spread bought for 0.75 i...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Geo-Pol Risk Remains Ahead Slew of Central Bank Announcements This Week

Apr-27 19:36

- Treasuries look to finish weaker Monday, a little off second half lows as crude prices pared gains despite simmering middle east tensions.

- IRANIAN FOREIGN MINISTRY CONDEMNS US SEIZURES OF IRAN-LINKED TANKERS AS 'OUTRIGHT LEGALIZATION OF PIRACY AND ARMED ROBBERY ON THE HIGH SEAS- POST ON X - [RTRS]

- TYM6 -6.5 at 111-00.5 after the bell vs. 110-30 low, technical support to watch is 110-16, the Apr 2 low. 10Y yield +.0349 after the bell at 4.3355%.

- Data picks up tomorrow with ADP weekly employment and Conference Board Consumer Confidence. Otherwise, focus is on Central Banks this week with the BOJ tomorrow, the FOMC Wednesday, and the BOE and ECB on Thursday.

- Most banks see the BOJ pausing at the 27–28 April meeting while retaining a “hawkish hold” stance, with tightening still part of the forward path. Tankan surveys, corporate earnings, and ~5% spring wage gains for a third year suggest resilient activity, with underlying inflation broadly near 2% supporting gradual normalisation.

- The Federal Reserve is expected to stay on hold this week as officials debate whether tariffs and the weeks-long Iran war have discernably altered the inflation outlook and might eventually require more restrictive policy rates

FED: Macro Since Last FOMC - Labor: Resilient, And If Anything, Improving (2/2)

Apr-27 19:33

- The FOMC will probably be relieved that it has another month to assess the fallout from the Middle East war without being unduly concerned about an imminent collapse in the labor market.

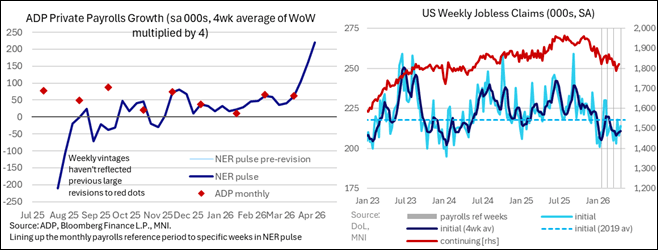

- That lack of immediate concern has been further bolstered by higher frequency indicators with initial jobless claims holding at very low levels and weekly ADP employment accelerating to a monthly equivalent that would be its strongest since Jan 2024.

- The Committee will continue to see a low-hiring, low-firing labor market that is indicative of being roughly in balance, with the underlying data meaning the debate is set to continue over whether it is weakness in labor supply or demand that has the upper hand.

For more detail, see our latest Employment Insight - “Strong Bounce Alleviates Concerns” (link).

FED: Macro Since Last FOMC - Labor: Resilient, And If Anything, Improving (1/2)

Apr-27 19:31

Data in the five and a half weeks since the last FOMC meeting have on balance shown initial resilience to the energy price shock seen in March, especially in the labor market, although surveys warn higher spillover to non-energy prices could be in the pipeline.

Labor Market: Resilient, And If Anything, Improving

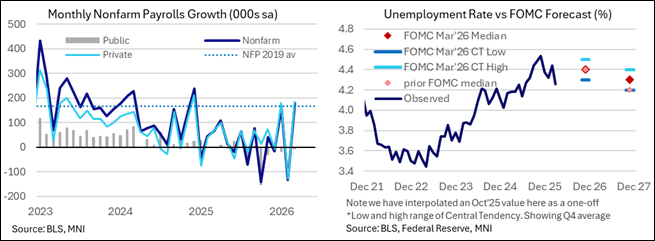

- The March BLS employment report was undoubtedly strong across its main readings and will have allayed concerns that February's pullback in payrolls portended a renewed leg of weakness in the labor market. Monthly nonfarm payrolls growth of 178k was the highest since December 2024, easily beating the 70k MNI dealer median, with private payrolls up 186k vs the 75k expected.

- In addition, the dip in the unemployment rate to a nine-month low 4.26% (consensus 4.4%, 4.44% prior) in the household survey suggested that the headline payroll gains were no fluke.

- But while this was a better-than-expected report, it came in the context of significant volatility in month-to-month figures, including sizeable revisions to February's reading (-113k vs -92k, offset by a +34k upside revision to January). And the rebound, while impressively broad across sectors, was still heavily driven by healthcare employment and other sectors that appeared impacted by one-off factors in February.

- Stepping back, the three-month change in payrolls has firmed to +68k (an 11-month high), with the 6-month average gains rising to 15k from -2k in Feb for the highest since in 6 months. So, an improvement in trends, but not enough to suggest that employment gains are doing anything but treading water. Payrolls have grown by just 0.2% Y/Y.

- Indeed, while the unemployment rate drop was suggestive of reduced labor market slack, it was flattered by a decline in the size in the labor force as well as falls in the participation and employment-to-population ratios. The weakest response rate in survey history is also a concern. Additionally, growth in average hourly wages continued to decline to fresh post-2021 lows on a Y/Y basis and are far off post-pandemic highs.