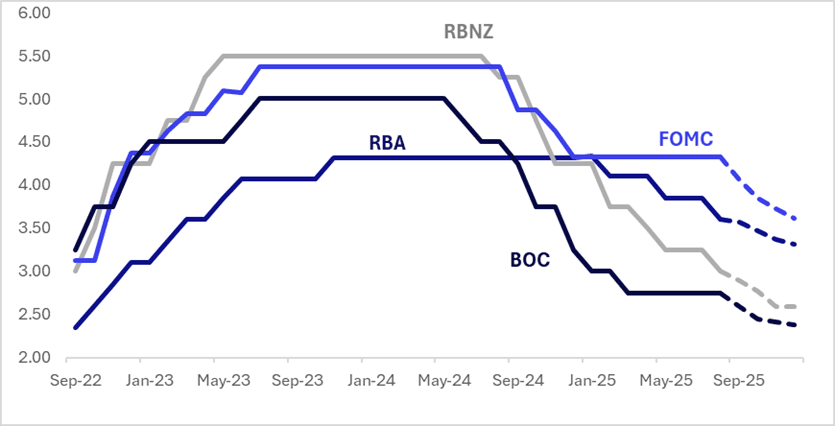

STIR: US Leads Bloc Markets Rates Lower Since Late August

Interest rate expectations across the $-bloc showed mixed performances over the past few weeks, with the US (-22bps) and Canada (-16bps) sharply lower, New Zealand slightly lower (-4bps) and Australia slightly firmer (+7bps).

- In the US, the key focus this week was on the August CPI print. In terms of key information, MNI believes that core PCE-relevant components from the August CPI report were, on net, benign, despite a slightly above-consensus core CPI reading. Since the release, multiple sell-side analysts have revised their core PCE % M/M projections to the downside. MNI now estimates a median of 0.20% (unrounded forecast range of 0.18-0.25%), vs a median a little above 0.3% at the start of the week. If correct, that would mean at least a 3-month low on a M/M basis, but also a slowdown on a 6-month annualized rate basis to 2.4% from 3.0% prior (3mma steady at 3.0%).

- MNI INTERVIEW: Fed To Cut Every Meeting To End Year - Bullard. The Federal Reserve is on track to lower interest rates by a full percentage point over the next six months, starting with three 25 basis point cuts at each of this year's remaining meetings, as tariff continue to have only muted effects on inflation and a fairly static labor market persists, former St. Louis Fed President James Bullard and a contender to become the next Fed chair, told MNI.

- Looking ahead, the next key regional events are the FOMC’s and BoC’s decisions on September 17, with market pricing giving a 25b85 cut at these meetings a probability of 109% and 85% respectively.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing are as follows: US (FOMC): 3.62%, -71bps; Canada (BOC): 2.38%, -37bps; Australia (RBA): 3.31%, -29bps; and New Zealand (RBNZ): 2.50%, -41bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 5-Year JGB Auction Results

The Japanese Ministry Of Finance (MoF) sells ¥ 1,842.1bn 5-Year JGBs:

- Average Yield: 1.056% (prev. 0.989%)

- Average Price: 99.74 (prev. 100.05)

- High Yield: 1.062% (prev. 0.993%)

- Low price: 99.71 (prev. 100.03)

- % Allotted At High Yield: 67.7077% (prev. 6.9288%)

- Bid/Cover: 2.9616x (prev. 3.5411x)

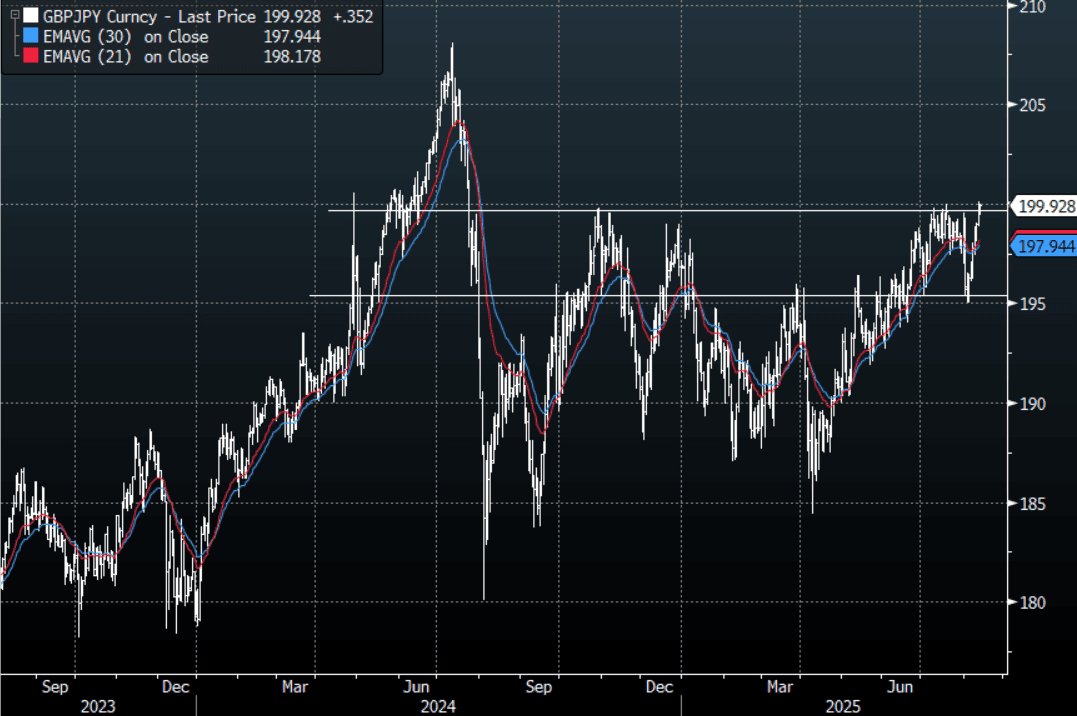

FOREX: JPY Crosses - Push Higher As US Stocks Makes New Highs, GBP/JPY Tests 200

US Equities stormed to new all-time highs in the N/Y session as the market gears up for a potential series of rate cuts. This morning US futures have opened pretty muted albeit still at their highs, ESU5 -0.04%, NQU5 +0.03% The JPY crosses remain better bid as risk extends higher, GBP/JPY leads the move eyeing a test of 200.00.

- EUR/JPY - Overnight range 172.08 - 172.86, Asia is trading around 173.00. This pair bounced off its support just below 170.00 and has put a base in now around 170.00. While risk continues to trade positive this will remain bid now on dips.

- GBP/JPY - Overnight 198.13 - 200.08, Asia trades around 199.90. Risk has broken higher again overnight and there has been no sign of a pullback which has seen the pair blow through what should have been decent resistance. A move back above 200.00 could generate fresh impetus higher and dips back towards 198.50 should now find support first up.

- NZD/JPY - Overnight range 87.80 - 88.18, Asia is currently dealing 88.20. The pair found solid demand towards the 86.50 area, I felt sellers should remerge on a bounce back towards 88.50 first up but the price action in the other JPY crosses would make you question a fade for now. A sustained move back above 89.00 would reinstate the momentum higher.

- CNH/JPY - Overnight range 20.5518 - 20.6465, Asia is currently trading around 20.6100. This pair found solid demand back towards its first support area around 2.4000. A sustained break back below 2.3000 is needed to turn momentum lower again, until then dips will probably continue to be supported.

Fig 1 : GBP/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Slightly Richer After Today's Q2 Wages Data

ACGBs (YM +1.5 & XM +0.5) are slightly stronger after today’s wages data.

- The Q2 WPI rose 0.8% q/q leaving annual inflation at 3.4% y/y after a recent trough at 3.2% in Q4 2024 and 4.1% in Q2 2024. Public sector quarterly wage gains outpaced the private sector for the third consecutive quarter at 1.0% q/q compared with 0.8%. Public wage growth is now up 0.1pp to 3.7% y/y, while private was 3.4% y/y. The RBA had forecast 3.3% for Q2 and in its August projections is expecting the WPI to trend lower to around 3% by Q2 2026. 2025 to date is showing some stabilisation in wage inflation.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are flat to 2bps richer with a steeper 3/10 curve and the AU-US 10-year yield differential at -5bps.

- Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.22bp through prevailing mids. Moreover, today’s cover ratio rose to 3.2417x from 2.6500x.

- The bills strip is +1 to +3.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 41% probability, with a cumulative 40bps of easing priced by year-end.