SECURITY: US-Iran Strike Risk Rises Amid Diplo Moves, Lack Of Clarity From Talks

The implied probability US President Donald Trump authorises strikes on Iran in the coming weeks has...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

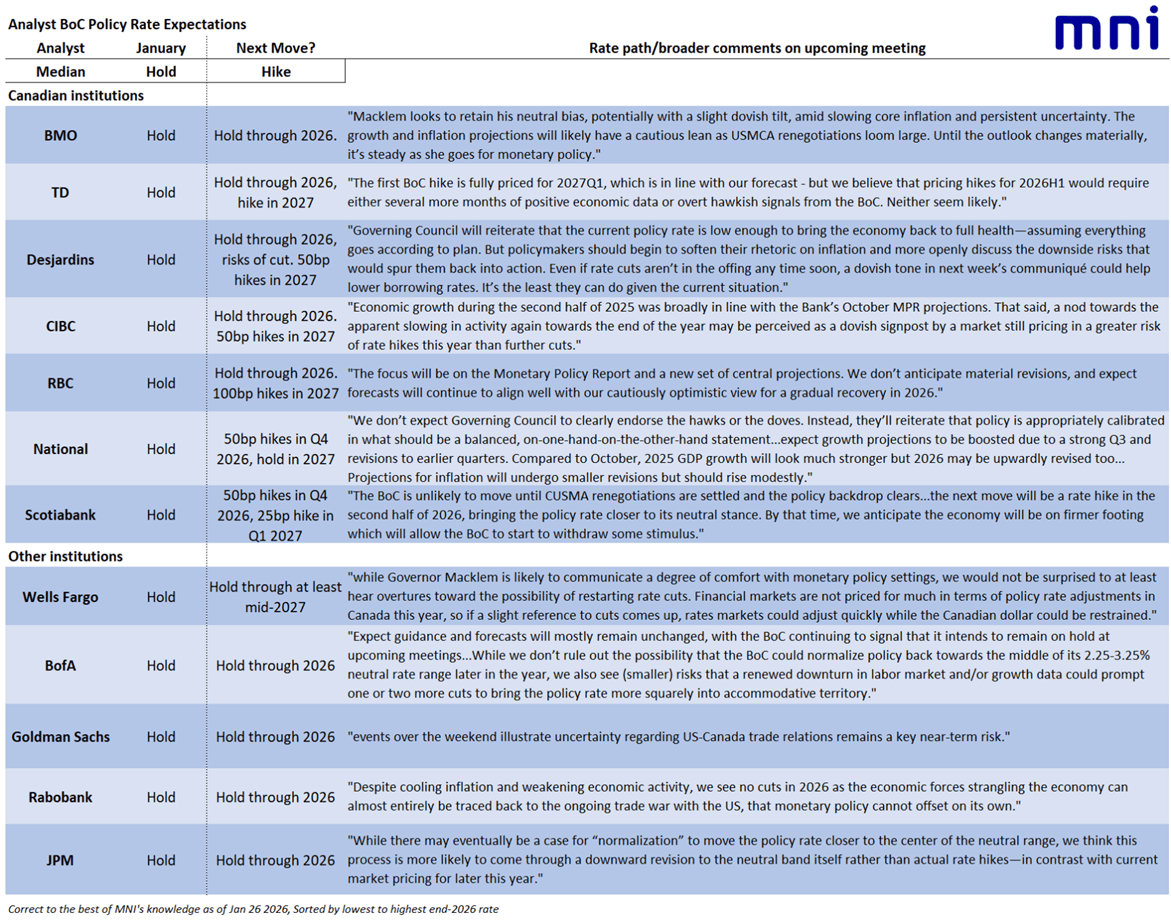

BOC: Uncertain Tone On Near-Term Outlook Seen Accompanying Rate Hold (Again)

The Bank of Canada is overwhelmingly expected by both markets and analysts to maintain its overnight rate at 2.25% for a 2nd consecutive time at its January meeting (announcement at 0945ET), as we explain in our preview (link). Markets go into the meeting implying a slight bias toward a cut by mid-year (~8-9bp cumulative easing through July), but rates actually ending the year higher (by about 10bp vs current levels).

- In other words, no moves are expected by the BOC this year, but lingering downside risks to the economy largely via trade uncertainty are seen keeping the BOC circumspect on rate hike potential in H1 and open-minded to a little bit more easing if warranted by an unforeseen economic shock. By year-end though, the market's base case appears to be that the summer's CUSMA renegotiations relieve lingering uncertainty, fiscal stimulus begins to feed through, and the BOC considers bringing rates up a little within its neutral band. A collation of sell-side analyst opinions is in the table in image below.

- Press Conference: It would be surprising if today Gov Macklem signaled a bias in one direction or another - at the last meeting he largely downplayed the surprising strength in incoming data and we'd expect him to do likewise to the softer prints received since then. In December Governing Council debated "whether it was more likely that their next move would be to raise or lower the policy interest rate" and left it an open question.

- Rate Announcement: The statement in turn should largely repeat December's semi-guidance: "If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment. Uncertainty remains elevated. If the outlook changes, we are prepared to respond." MNI's Instant Answers (see below) will be watching for any signs of deviation from that guidance and the degree to which policymakers are concerned about an apparent resurgence in geopolitical risks.

- Monetary Policy Report: Additionally the January MPR is likely to show an upgrade to GDP growth projections for 2025 as a whole with a potential slight upgrade to 2026 at a still-soft level. We’ll be watching for adjustments to the estimated output gap from the -1.5 to -0.5% range in Q3, which looks to be largely closed due to historical GDP revisions as well as the stronger Q3 GDP reading itself. CPI forecasts also look set to be raised slightly due to higher-than-expected headline readings in the latter months of the year, but as we explain in our preview, the more important underlying metrics have been subdued.

A reminder that we have chosen the following questions for our Instant Answers service with the BoC decision at 0945ET:

- Overnight Rate Target (level in x.xx%)

- Does the Bank signal it is prepared to lower rates in the future?

- Does the Bank say the policy rate appears appropriate if its economic forecast is realized?

- Does the Bank signal it intends to leave rates on hold?

- Does the Bank mention added risk from recent global geopolitical changes?

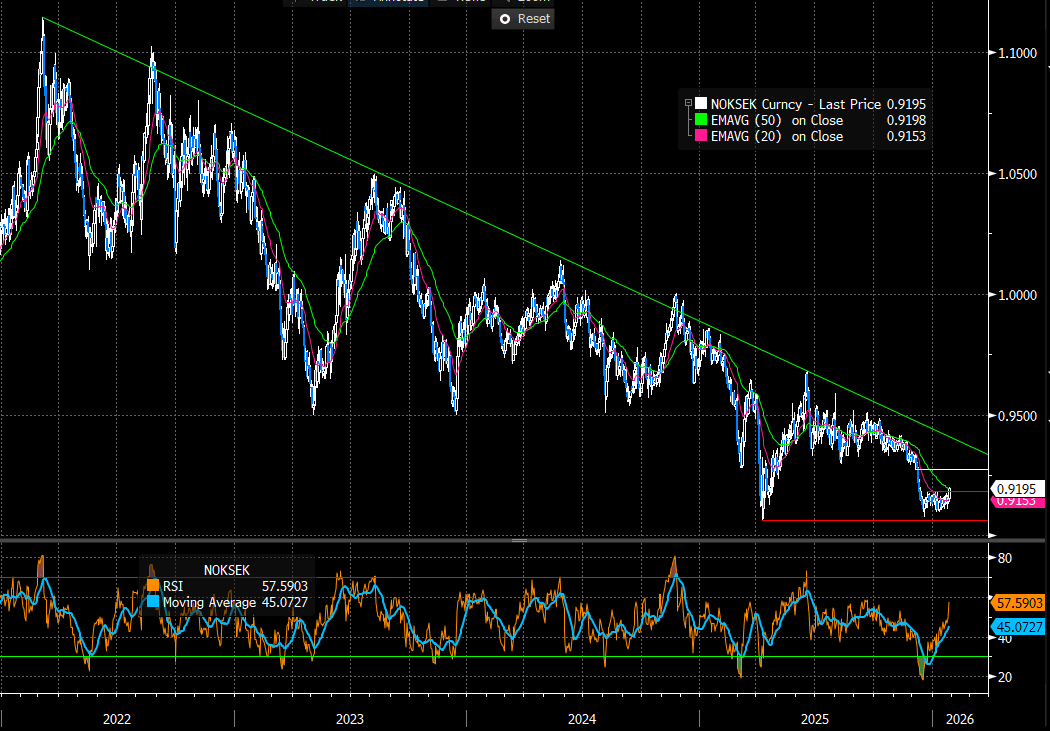

SCANDIS: NOKSEK Tests Key 50-day EMA Resistance; Riksbank and Growth Data Thurs

NOKSEK has tested key resistance at the 50-day EMA of 0.9198. A clear break of this average would be a bullish development, and set the stage for a push towards 0.9276, the December 4 low and prior breakdown level. We noted last week that the cross had been incrementally registering higher highs and higher lows since mid-Jan, potentially signalling the start of an uptrend.

- Today’s 0.45% rally mostly reflects SEK underperformance versus the G10 basket, with European equity futures down 0.6% at typing. Meanwhile, NOK is a little more insulated owing to the intraday rebound in crude oil futures.

- Tomorrow’s calendar includes the Riksbank decision, alongside a significant amount of Swedish growth data. Q4 flash GDP is expected at 0.5% Q/Q, a tenth above the Riksbank’s December MPR projection. Of course, the flash reading should be taken with a pinch of salt given its revision prone nature.

- The Riksbank is expected to hold the policy rate at 1.75%, while reiterating that it is “expected to remain at this level for some time to come”. We expect communication to re-iterate that a cyclical economic recovery is underway, but believe lingering downside inflation concerns, the much stronger-than-expected krona and spare capacity in the labour market will guard against any hawkish pivot for now. Geopolitical uncertainty and a (brief) return of tariff risks will likely also provide the Board a reason to stay cautious.

- MNI’s full Riksbank preview is here

Figure 1: NOKSEK Since 2022 (Source: Bloomberg Finance L.P)

GERMANY: Economy Ministry Downwardly Revises 2026 Forecast

The German economy ministry sees 2026 growth now at 1.0%, 0.3pp below the previous forecast for this year. The fiscal stimulus is seen to drive two thirds of German growth this year. 2027 growth is now seen at 1.3% (from 1.4%).

- On the 2026 revisions: "This is primarily due to a less favourable statistical carryover from the previous year as a result of economic development in the second half of 2025 being somewhat weaker than expected at the time. An economic recovery is still expected for 2026, driven primarily by stronger domestic economic momentum, accompanied by a slight easing of external economic pressures."

Full report here.