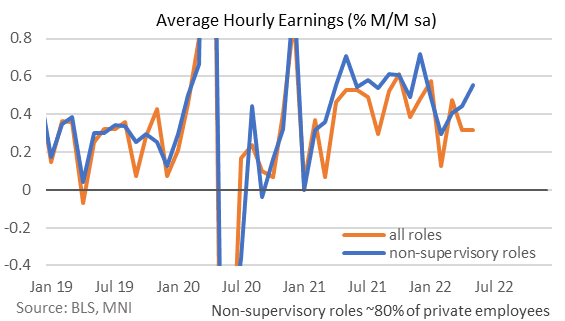

DATA REACT: US AHE Below Consensus But Shouldn't Surprise

Jun-03 12:42

- AHE a tenth lower than consensus at an unchanged +0.31% M/M but as a few analysts had noted in our preview, there was a calendar quirk biasing the number lower in May so it's shouldn't be too surprising.

- For what it's worth, the non-supervisory measure (lower ~80% of earners) continues the theme from the past year of coming in stronger, accelerating from +0.44% to +0.55% M/M.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Market Roundup: Weaker Post-ADP, Tsy Refunding Reduction

May-04 12:36

Brief two-way trade after April ADP private employ data +247k vs. +385k est, FI trading weaker into the NY open -- bounces after quarterly US Tsy refunding annc.

- Tsy plans to continue reducing auction sizes of coupons during the May-July quarter, but by smaller increments than in previous quarters, and left open the door for additional cuts in future quarters if needed.

- Curves flatter (2s10s -3.010 at 15.462) with short end underperforming, modest overall volumes w/Japan and China out on holiday.

- Carry-over weakness in short end as markets pricing in potential for more aggressive rate hikes from the Fed (already at five 50bp hikes) by year end.

- US 10Y technicals: TYM2 currently at 118-12.5 (-4) after probing key support at 118-08 yesterday (Apr 22 low and a bear trigger).

- This signals a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs. MA studies remain in a bear mode. Potential is seen for weakness towards 118-02+ next, a Fibonacci projection and 117-22+, the Nov 8 2018 low (cont). On the upside, key short-term resistance is at 120-18+.

- Stocks holding modest gains, ESM2 at 4183.25 vs. 4168.75 lows. Await more earnings announcements after the bell.

- Cross-assets: WTI Crude Oil (front-month) bouncing +$3.62 at $106.04; Gold weaker -2.22 at $1865.59.

DATA REACT: US ADP Employment Sees Large Drag From Small Businesses

May-04 12:35

- ADP employment rises 247k in April, a 136k miss to consensus. Revisions should make up for it (24k to Mar at 479k, 115k to Feb at 601k), but the larger one in Feb likely receives less attention.

- Those revisions plus the limited reliability of month-to-month correlation with NFPs should limit impact.

- There was however an unusually large hit from small businesses, where jobs fell by 120k, the largest decline since May’19 and before that Feb’09 (barring the 5.2M drop in Apr’20).

- Fed Funds futures pricing of hikes firmed modestly shortly after the release, with cumulative hikes for June sitting off earlier highs but still at 111bps.

US-EU: Sec State Blinken To Meet Swedish Counterpart Amid NATO Speculation

May-04 12:32

11:00 ET 16:00 BST: US Secretary of State Antony Blinken will meet today with Swedish Foreign Minister Ann Linde at the State Department. The meeting with be preceded by joint remarks streamed on the State Department YouTube: www.youtube.com/statedept.

- The meeting comes following a week of speculation that Sweden and Finland may be preparing formal applications to NATO.

- The Swedish parliament is currently conducting a security policy review on the pros and cons of NATO membership with the results expected on May 13.

- The US has encouraged NATO application of the two states with Defence Secretary Lloyd Austin noting last week that the applications would be fast-tracked due to the limited support required for membership.

- Both Sweden and Finland are observers to NATO on all matters of security related to Russia and the war in Ukraine.