US TSYS: US 30yr Yield edges towards 5%

The US 30yr Yield is now probing 4.98% and the key 5% would equate to 111.29 in USM6 Today. (Chart ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Yen Weakness Extending, USDJPY Eroding Post-Election Selloff

- The Japanese yen has come under renewed pressure on Wednesday, keeping this week’s weakening trend a key characteristic across the G10 FX space. USDJPY topside momentum accelerated notably on a break of key resistance at 156.29, the Feb 10 high. The pair has printed session highs of 156.66 so far, extending the recovery from last week’s lows to 2.65% and further eroding the post-election selloff.

- We have highlighted that the holding of support in the low 152’s has managed to keep a bullish USDJPY trend condition intact, and a continuation higher for USDJPY would turn the focus to 157.76, the Feb 9 high.

- Interestingly, Japan Deputy Chief Cabinet Secretary Ozaki stated overnight that he is aware of reports around Takaichi's concern around further BoJ hikes but said that Takaichi didn't have a specific request for BoJ Governor Ueda. Ozaki added that specifics of monetary policy are left to the BoJ.

- While this development has a moderate hawkish lean, it was immediately offset by the government announcing the nominations of Toichiro Asada and Ayano Sato as Bank of Japan board members. Both university professors, the new nominees are reported to be in favour of easy policy and active fiscal spending, stoking the bearish yen narrative.

- Broad yen weakness alongside a firmer Australian CPI print has assisted AUDJPY to its highest point since 1990, reaching 111.22.

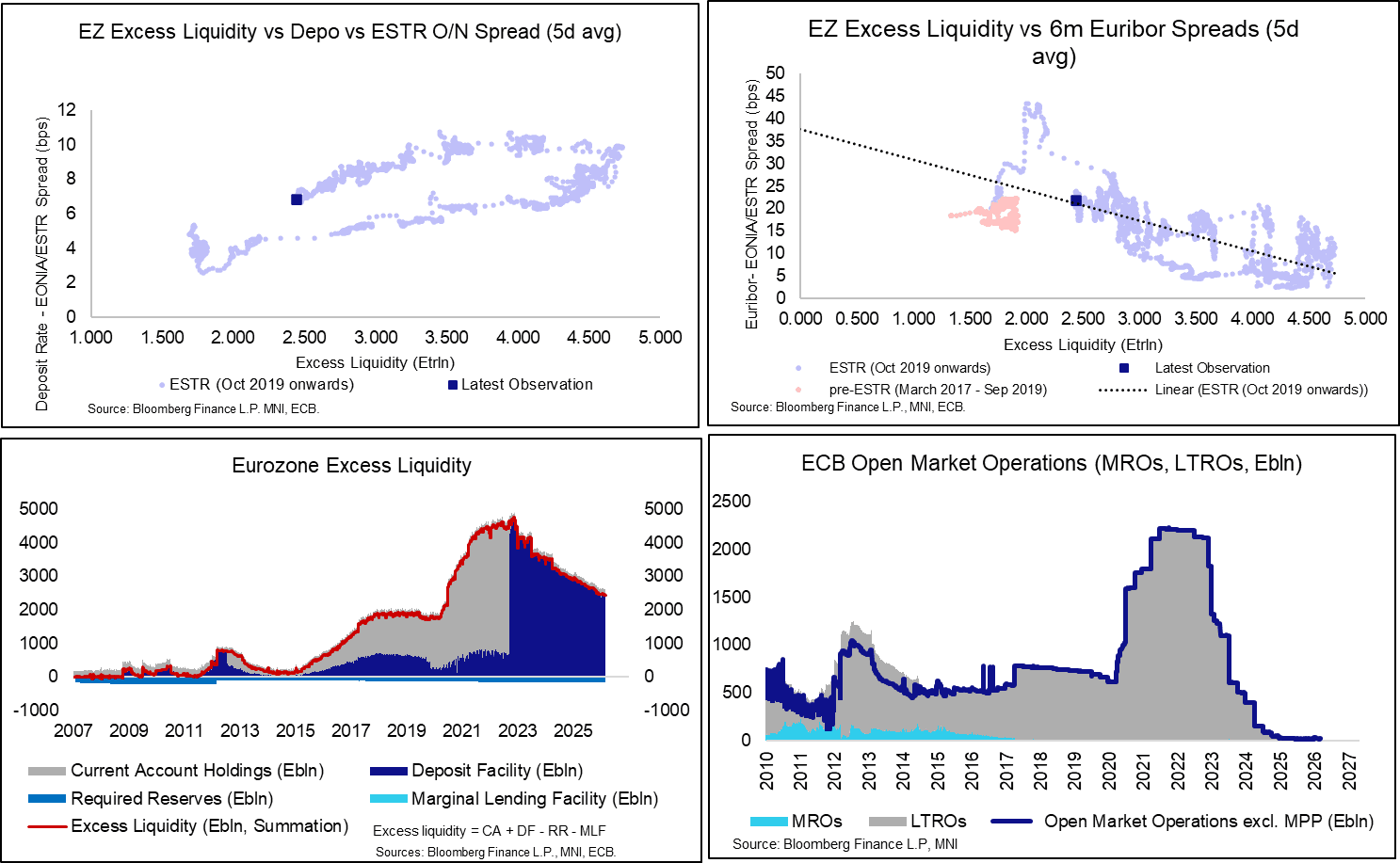

ECB: Eurozone Excess Liquidity Still Seems Abundant

Eurozone excess liquidity is around E2.44trln, down from E2.49trln in the middle of January and E2.90trln at the start of 2025. At current levels, excess liquidity remains above the ECB’s “upper scenario” for reserve demand of around E2.2trln (150% LCR target & 30% reserves/HQLA). There is considerable uncertainty around where bank’s demand for reserves will settle in the coming years, and therefore when the ECB needs to progress its implementation of structural operations/ the structural bond portfolio. For now, unsecured money market spreads appear well-behaved, and take-up of the ECB’s open market operations remains low – this suggests the supply of reserves is still abundant relative to bank’s demand.

A reminder in the latest ECB Economic Bulletin, staff presented estimates of the time-varying reserve elasticity of Euro-area money market rates.

- Staff concluded that there is currently no statistically significant evidence of heightened ESTR rate sensitivity to liquidity conditions in the euro area. This isn’t too surprising – the ECB noted that the unsecured segment makes up just 9% of total money market turnover in its 2024 study.

- Repo rates exhibited a larger elasticity to liquidity fluctuations (the secured segment made up 30% of total money market volume in 2024). Staff noted that “repo rate sensitivity strengthened during periods of liquidity growth (e.g. in 2021 and early 2022) and weakened during times of balance sheet reductions (e.g. in 2018/19 and late 2022).

- “This pattern suggests the presence of a collateral scarcity channel, where Eurosystem asset purchases constrain collateral availability in repo markets. As collateral becomes scarce, repo rates are subject to more – rather than less – downward pressure relative to the deposit facility rate when excess liquidity expands further”….”Conversely, when collateral supply increases, the scarcity premium diminishes, reducing repo rate sensitivity, all else being equal"

- “Since early 2023 repo rate sensitivity has been rising again in line with the traditional patterns, and secured rates have become mildly more sensitive than unsecured rates.”

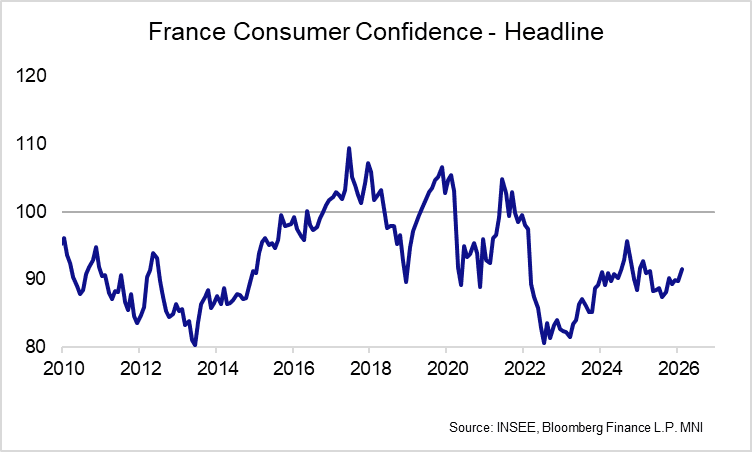

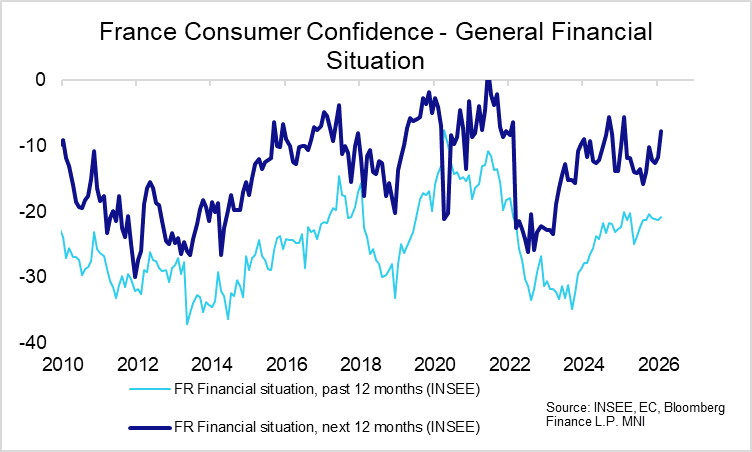

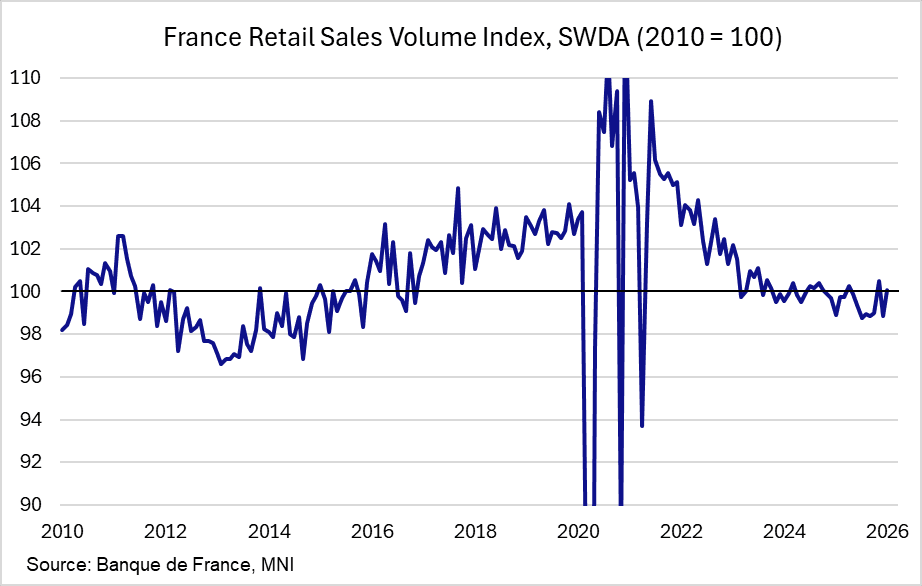

FRANCE DATA: Consumer Sentiment Rises in Feb; Jan Retail Sales Partially Rebound

INSEE's consumer sentiment indicator rose 1.7 points to 91.5 in February (rounding down to 91), above (rounded) consensus of 90. The rise was driven mainly by improved views on future personal financial situation and improved current savings capacity, alongside a decent reversal lower in price expectations for the next year. The Banque de France's January retail sales data showed a partial rebound from a sharp (but upward revised) December drop.

- Expectations for consumer prices in the next 12 months fell 4.1 points to -29.9, more than unwinding January's rise. It is still a touch less negative than the long-term average of -32 (since Jan 1973). This fall could also be helped by the soft domestic inflation print for January.

- Views on consumer prices over the last 12 months also fell a sharp 5.6 points to -12.1, the lowest since June 2021.

- The view of personal financial situation in the next 12 months gained 4.0 points to -7.7, now close to the long-term average of -7.

- Current savings capacity grew 3.4 points to 23.6. Year-ahead savings intentions, however, dropped 1.4 points (now 38.7 - though noting a sharp rise in Jan), while expected savings capacity rose 2.8 points to 17.4.

- Elsewhere, the view on the general economic situation over the next year grew 3.6 points to -53.9, but still remains well below the long-term average of -29, while unemployment expectations increased 2.3 points to 47.9, notably above the long-term average of 33. All other subcomponents remained relatively stable on a rounded basis.

- Responses were collected from 27 Jan - 16 Feb 2026, so encompass some time before the eventual passing of the 2026 budget (on 2 Feb) - though most of the survey period is after the budget was passed. The removal of that political uncertainty could have helped the rise.

- Also released this morning, French Jan retail sales volumes partially reversed December's sharp fall, at 1.2% M/M, SWDA (-1.6% Dec, revised up 0.2ppt), continuing the series' recent volatility. The Banque de France highlights rebounds in both food (1.2% M/M after -0.7% Dec) and manufactured goods (1.3% M/M after -2.3% Dec) driving the move, with particularly sharp monthly reversals in footwear and sports equipment. Bikes and motorcycles were the overwhelming negative driver at -10.6% M/M (after 1.7% Dec).

- This left retail sales 3M/3M growth at 0.9% 3M/3M (vs 0.6% Dec), driven mostly by non-food sales growth. The index level still sits below November's high, but is back above 100.

- Domestically, focus turns to Friday, which sees Feb flash inflation, Q4 final GDP, Q4 final payrolls, as well as Jan consumer spending and PPI.