US DATA: UMichigan: Inflation Expectations Softens Amid Recessionary Sentiment

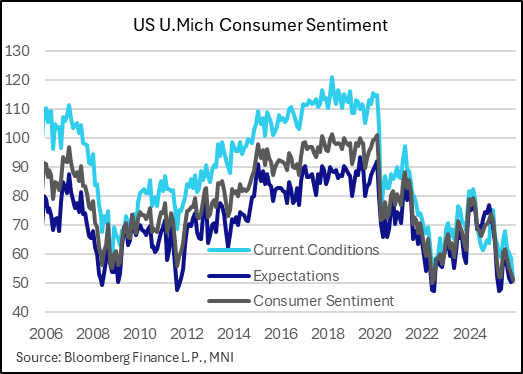

The final University of Michigan consumer survey for November represented an upgrade from the preliminary readings on overall sentiment with inflation expectations showing continuing signs of moderation at a high level. However, current conditions fell to an even poorer level than the all-time worst recorded in the preliminary survey, with extremely pessimistic sentiment regarding the labor market, signaling that consumer conditions remain weak.

- Regarding the upgrade to the headline sentiment reading (51.0, lowest since June 2022) from the prelim (50.3), the report notes: "Following the end of the federal shutdown, sentiment lifted slightly from its mid-month reading. However, consumers remain frustrated about the persistence of high prices and weakening incomes."

- Current economic conditions were downgraded however to 51.1 from 52.3 (still way down from October's 58.6), with expectations bumped up to 51.0 from 49.0 (just up from October's 5-month low 50.3). That's especially noteworthy for current conditions since the preliminary reading was already the lowest on record.

- On that note, the report highlighted "considerable differences in economic views across the wealth distribution", which manifested itself in a downgrade to prelim readings in one regard: "current personal finances and buying conditions for durables both plunged more than 10%, whereas expectations for the future improved modestly. By the end of the month, sentiment for consumers with the largest stock holdings lost the gains seen at the preliminary reading. This group’s sentiment dropped about 2 index points from October, likely a consequence of the stock market declines seen in the final two weeks of the interview period."

- Also regarding socioeconomic divides, "income expectations declined from last month for younger consumers, while middle age and older consumers held steady or inched up to relatively low levels." Sentiment worsened across all political affiliations, with the gauge of opinion of government policy at new lows.

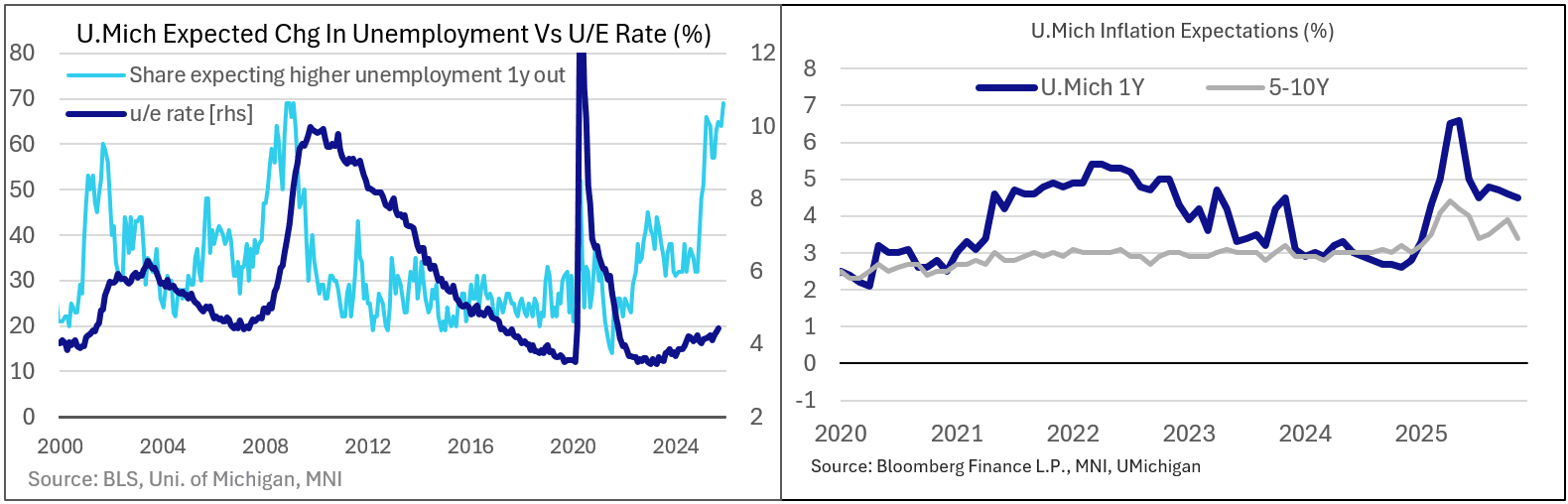

- The report notes that the overall probability of personal job loss rose to the highest since July 2020; the percent expecting higher unemployment in 1 year was the highest since the 2008-09 financial crisis.

- The 4.5% 1Y inflation expectations reading was a 3rd consecutive monthly dip (vs the uptick to 4.7% seen in the prelim vs 4.6% in October), while the long-run gauge pulled back considerably to 3.4% (vs 3.6% in the prelim and 3.9% in October). But the report notes "Despite these improvements in the future trajectory of inflation, consumers continue to report that their personal finances now are weighed down by the present state of high prices."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Large Nov'25 10Y Put Buyer

- +30,000 TYX5 113.75 puts from 16-17 - expiring this Friday

FED: US TSY 17W AUCTION: NON-COMP BIDS $475 MLN FROM $69.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $475 MLN FROM $69.000 BLN TOTAL

US 10YR FUTURE TECHS: (Z5) Bull Cycle Intact

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-21 @ 16:01 BST Oct 22

- SUP 1: 113-03+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-22 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

Bullish conditions in Treasuries remain intact. The recent breach of key resistance at 113-29, the Sep 11 high, confirms a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 11303+, the 20-day EMA.