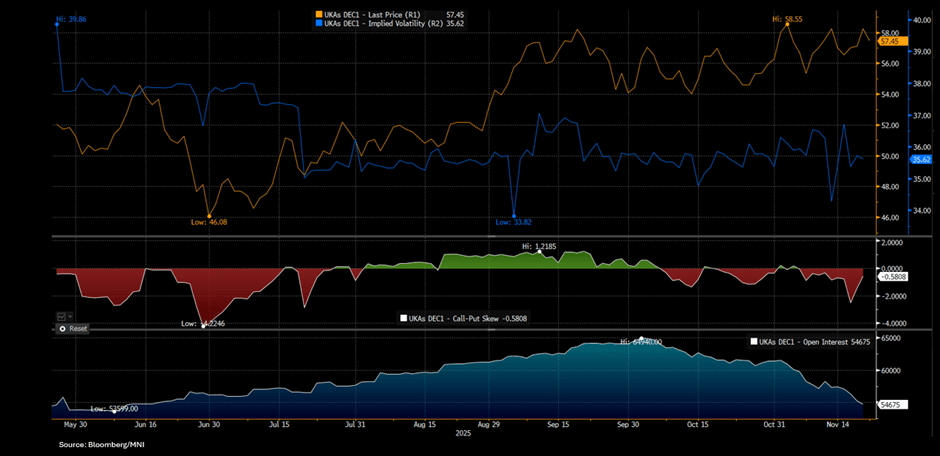

EMISSIONS: UKAs Options Volatility Remains Stable, Call-Put Skew Widens

Nov-21 13:02

UKA Dec25 options implied volatility as of 20 Nov was at 35.62%, remaining stable from the level at early November when the price hit the highest level since June 2023. Call and put open interest remained at a similar level, while the call-put volatility skew widened, signalling stable demand for downside protection.

- Implied volatility fell to 35.62% on 20 Nov from 36.11% on 4 Nov.

- The 25-delta call-put volatility skew widened to -0.58% from -0.14% on 4 Nov.

- The put/call open interest ratio increased slightly to 1.31 on 20 Nov from 1.30 on 4 Nov, with put open interest rising 0.92% to 16,475 contracts, while call open interest edged up 0.20% to 12,605.

- The largest open interest at the €45/t put strike with 6,025 contracts, and the €50/t call strike with 3,225 contracts.

- UKA Dec25 futures open interest fell to 54,675 on 20 Nov from 60,946 on 4 Nov, while the price declined to €57.50/t on 21 Nov from €58.55/t on 4 Nov when the price reached the highest levels since June 2023.

- UKA DEC 25 down 1.34% at 57.45 GBP/t CO2e

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: UPDATE: BLOCK/Screen/Pit Mar'26 SOFR Put Spread

Oct-22 12:41

Total +50,000 SFRH6 96.31/96.37 put spds, 1.5 vs. 96.625 to -.64/0.06%

US INFLATION: MNI US CPI Preview: The Year’s Last ‘Reliable’ CPI Read?

Oct-22 12:27

- We have published and e-mailed to subscribers the MNI US CPI Preview ahead of Friday's release.

- Please find the full report including MNI analysis and views from analysts here: https://media.marketnews.com/USCPI_Prev_Oct2025_f7e5818f86.pdf

Executive Summary

- The delayed September CPI report is due for release on Friday Oct 24 at 0830ET, with the BLS making an exception on social security payments grounds during the government shutdown.

- It’s possibly the last report that won’t be adversely impacted by the shutdown until the new year, although quality concerns were already elevated with high reliance on imputed values back in August.

- We see a median unrounded analyst estimate at 0.40% M/M for headline and 0.30% M/M for core CPI.

- This would mark a marginal sequential acceleration for headline as energy strength offsets a slight moderation in core after a stronger than expected 0.35% M/M in August.

- Monthly core CPI inflation is expected to see firmer goods inflation across a variety of items but softer services, primarily from rents after what’s seen as a temporary upside surprise in August.

- Core CPI inflation is expected to hold at 3.1% Y/Y for a third consecutive month whilst headline CPI firms two tenths to 3.1% Y/Y for its fastest since May 2024 but with chance of rounding to 3.0%.

- Core PCE inflation meanwhile is seen at ~0.30% M/M in September in early analyst estimates, an acceleration from 0.23% in August and 0.24% in July barring potentially wide-ranging revisions. That would see a third month at 2.9% Y/Y, with the median FOMC participant forecasting 3.1% Y/Y for 4Q25.

- There has been no update on potential release date for the September PPI report, likely leaving the Fed with ~65% of inputs for PCE inflation in September ahead of the Oct 28-29 FOMC meeting.

- Markets see a 25bp cut next week as locked in and currently fully price another 25bp cut in December before roughly a quarterly pace thereafter with cuts in March and June.

- The labor market is driving the rate cut profile but broad-based upside surprises in this September report can see this path come into question in the near-term. The median FOMC participant last month eyed two more cuts this year (Oct and Dec) but with a sizeable share looking for a slower pace.

EURIBOR OPTIONS: Large Call Condor vs Put

Oct-22 12:25

ERM6 98.25/98.4375/98.50/98.87c condor vs 97.87p, bought the condor for 1.5 in 10k.