FED: Two 2026 FOMC Voters Headline Today's Fedspeak

It’s a heavier day for Fedspeak today and could provide a better sense of Fed reaction to recent NFP and CPI reports. That’s primarily from two of the less hawkish 2026 voters, with our sense that Paulson is the most dovish of the four on rotation with Kashkari more hawkish than her but less so than Hammack or Logan. A Goolsbee interview with local radio should also be published at some point. Miran is unlikely to surprise, with a well-touted view of the need for significant rate cuts with 150bps pencilled in for this year, whilst Williams being confined to 10mins of opening remarks could limit headlines there.

- ~0600ET - Goolsbee ('27 voter). NPR local radio was scheduled to publish an interview with Goolsbee "about the latest inflation numbers and President Trum's attack on Fed Chair Jerome Powell" but no sign yet - it will presumably be released at some point this morning. He dissented at the Dec meeting as he wanted more clarity on post-shutdown developments, but sees rates going down a fair amount if inflation is on track. Speaking on Dec 18, he saw a lot to like in the November CPI report.

- 0950ET – Paulson (’26 voter) on the economic outlook (text only). We judge her to have been one of the four 2026 dots which saw one cut this year (3.375%, the median on a divided committee) back in the Dec SEP, but she could be a notch lower on the dot plot having since expressed openness to modest additional cuts by year-end should the data cooperate.

- 1000ET – Gov. Miran (voter) on regulation and mon pol (text tbd)

- 1200ET – Kashkari (’26 voter) in town hall. The town hall set-up could limit mon pol discussion but for what it’s worth he sounded patient on the prospect of future rate cuts on Jan 5, deeming mon pol to be neutral and data dictating the next direction.

- 1200ET – Bostic (’27 voter retiring end-Feb) in moderated discussion. He said on Dec 16 that he would have preferred to hold rates in December and didn't pencil in any cuts in 2026, which we assume to mean a steady 3.875% rate throughout.

- 1410ET – Williams (voter) opening remarks (no text or Q&A)

- A reminder that the FOMC media blackout will start this weekend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

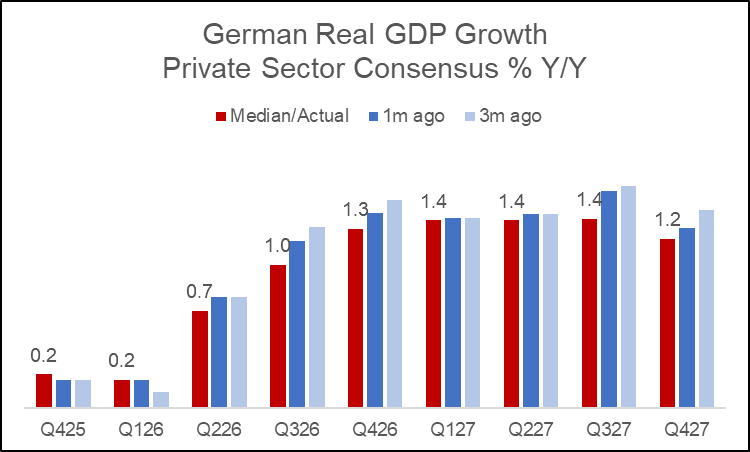

MACRO UPDATE: Downward Adjustment Of German Growth Forecasts Continues

Private sector German medium-term GDP forecasts have again seen a deterioration with hard data continuing to lag improving sentiment and an apparent stagnation in terms of wider economic reform from the government. The downward revisions across 2026 provide an interesting contrast to the most recent hawkish ECB repricing, and should be weighed against analysts' expectations for upward revisions to the ECB's Eurozone GDP forecasts which are to be published Thursday.

- Updating a median estimate from seven sellside analysts that we track, Y/Y growth is expected to start accelerating in Q2 of next year before topping out at 1.4% Y/Y over the course of 2027. However, these medium-term forecasts have seen downward pressure in recent months, with broad downward revisions of ~0.3pp in most of 2027 comfortably outweighing a marginally higher median for 4Q25.

- This comes after IFO published on Friday a material downside growth revision - to 0.8% Y/Y for 2026 (from 1.3%). 0.8% is exactly where their 2026 view stood right before IFO started incorporating the government's fiscal easing announcement from last March, suggesting this has been crowded out to a large extent by underlying weakness in the private sector. "The German government's measures will help in the short term but are insufficient to expand the production capacities of the German economy in the long term", IFO commented.

- The government also shared their view this morning, concluding that "the German economy continues to face conflicting pressures: on the one hand, external factors are weighing on the economy in the form of weak foreign demand, declining competitiveness, and isolated bottlenecks for certain intermediate goods; on the other hand, there are signs of a gradual stabilization of the domestic economy, supported in part by the increasingly noticeable fiscal stimulus measures implemented recently".

US 10YR FUTURE TECHS: (H6) Bear Threat

- RES 4: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 2: 112-27+ High Dec 5

- RES 1: 112-21/23 20-day EMA / High Dec 11

- PRICE: 112-11 @ 11:10 GMT Dec 15

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bearish theme in Treasuries remains intact and short-term gains appear corrective. The rally last Thursday topped out at 112-23, meaning resistance at the 20-day EMA, currently at 112-21, remains intact. A continuation lower would refocus attention on key short-term support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and signal scope for an extension towards 111-19, a Fibonacci projection.

EQUITIES: Option Expiry in Notional Terms

Equity Option Expiry in Notional Term for 19th Dec Triple Witching. These can of course change throughout this Week.

Very large expiries for the SPX, the last big one was September 2024 with 3.73T.

- SPX: $4.16T.

- NDX: $164.12bn.

- Amazon: $23.98bn.

- Apple: $25.35bn.

- SX5E: €457.99bn.

- SX7E: €38.48bn.

- Dax: €52.38bn.