JGBS: Twist-Flattener Leaves 2/30 YC Near Lower Bound Of Recent Range

In Tokyo morning trade, JGB futures are weaker, -12 compared to settlement levels.

- Japan Aug core machine orders were below forecast and lost y/y momentum, implying some downside capex momentum risks (which has been a resilient source of Japan's GDP growth). We were -0.9%m/m versus +0.5% forecast, whole July fell 4.6%. This dragged the y/y outcome down to 1.6%, with the market consensus looking for an unchanged 4.9% outcome in Aug.

- BOJ Board Member Tamura reiterated his hawkish stance, saying rates should move closer to neutral (at least 1%) as inflation risks rise. He warned inflation could exceed the BOJ’s outlook, noting firms’ strong investment and persistent price pressures, including food. Tamura said Japan’s real rates remain negative and that the BOJ is entering a rate-hike decision phase.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks, pivoting at the 10-year, with yields 2ps higher to 4bps lower.

- Today’s move leaves the 2/30 yield curve at 224bps, within its recent trading range, but approaching the lower bound around 220bp. (See chart)

- Swap rates are 1bp higher to 2.5bps lower.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: VIEW: Westpac Expects Inflation To Be Below 3% By End 2025

NZ food inflation stabilised at 5.0% y/y in August, its highest since November 2023, while increases for existing rents moderated 0.3pp to 2.1% y/y, the lowest since 2011. The stabilisation or moderation, especially travel-related prices, in August is likely to be welcomed by the RBNZ as it sees a risk that Q3 could print above 3%, the top of the band. Westpac believes that it will be below this level by year end.

- In line with RBNZ signalling, 25bp rate cuts are generally expected at its last two meetings in October and November bringing rates to 2.5%.

- The monthly series released today account for 46.5% of the quarterly CPI with Q3 to be released on October 20.

- Westpac observes that while August prices were lower than it was expecting, inflation is trending higher and it is forecasting it to reach 3.1% y/y in Q3 up from Q2’s 2.7% y/y. There is “a little downside risk” to its Q3 forecast for inflation “due to the volatile travel categories, which can swing around sharply month-to-month”, so it’s keeping its “forecasts as they are for now but will watch how those costs shape up over the coming month”.

- Electricity and gas price pressures remain elevated at 11% y/y and 14.1% y/y in August respectively. Westpac notes that “household energy costs up more than 10% this year”.

USD: BBDXY - Testing 1195 Ahead Of FOMC

The BBDXY range overnight was 1194.44 - 1198.95, Asia is currently trading around 1195, +0.03%. The USD continues to grind slowly lower, pressing and probing its recent support. A sustained break below 1195 is needed to regain the momentum lower and retest the year's lows towards 1180 where demand should return initially. A break sub 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. The USD is trying to break its recent support ahead of the FOMC with the market pricing in a dovish outcome, there are obvious risks to this buy the rumour strategy. I would prefer to have optionality around FOMC and trade the event than going in naked short with a low bar to disappoint.

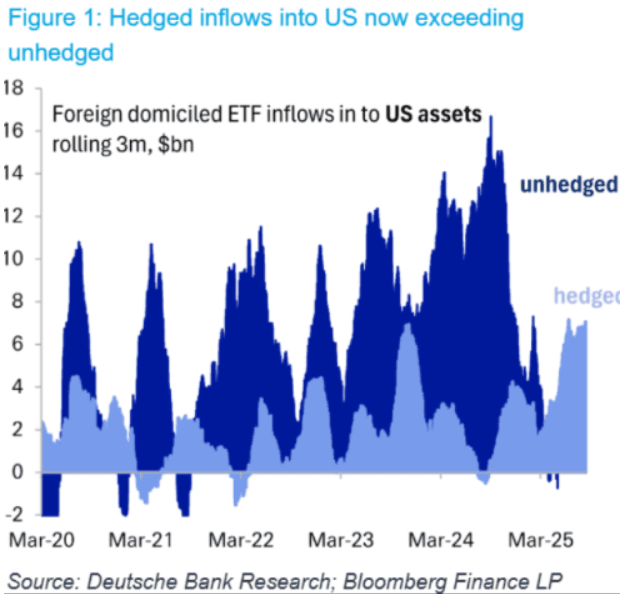

- Bloomberg - “Investors Cut Dollar Exposure at Record Pace, Deutsche Bank Says. Overseas investors are slashing their dollar exposure at “an unprecedented pace” as they put on currency hedges when buying US stocks and bonds.“The FX implications are clear: foreigners may have returned to buying US assets (albeit as we wrote last week at a reduced pace), but they don’t want the dollar exposure that goes with it,” Saravelos wrote. “For every hedged dollar asset that is bought, an equivalent amount of currency is sold to remove the FX risk.” See Graph Below

- RenMac on X: “Fed Should Go 50… But Likely Won’t – Neil Dutta”

- “The risk, however, is that Fed Chair Jerome Powell could push back at his post-meeting press conference by indicating a more cautious approach and stressing the need to monitor data on employment and inflation. “Powell will offer balance,” Thierry Wizman, a global FX and rates strategist at Macquarie Group, said in a note. “He’ll highlight again the downside risk to employment growth, but refrain from signaling a long string of cuts after September.” - BBG

- Data/Events : Retail Sales, New York Fed Services Business Activity, Industrial Production, NAHB Housing Market Index

Fig 1: Hedged Inflows Into US Exceeding Unhedged

Source: MNI - Market News/Bloomberg Finance L.P/Deutsche Bank

AUSSIE BONDS: Holding Early Gains

ACGBs (YM +3.5 & XM +5.0) are holding stronger after a positive overnight lead-in from US tsys.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest rally.

- Cash ACGBs are 3-5bps ricer with the AU-US 10-year yield differential at +19bps.

- The bills strip is +1 to +3 across contracts, with a flattening bias.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 10% probability, with a cumulative 28bps of easing priced by year-end.

- The focus this week, however, will be on Thursday's August jobs data. Employment is forecast to rise 21k after July's +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 1.00% 21 December 2030 bond on Friday.