US TSYS: Tsys Futures Pare Earlier Losses, Cash Trading Closed

Jan-02 05:01

- Tsys futures opened the session lower, with all contracts trading below Dec 31 lows, we have however seen a reversal over the past few hours and now trade little changed, volumes are below average, although this isn't surprising as cash trading is closed with Japan out. TU is -00⅜ at 102-25⅜, while TY is trading -00+ at 108-23+

- The trend condition in Treasury futures remains bearish despite the intraday rally into the Monday close. The gains made heading into year-end are considered corrective below the 109-12 20-day EMA. The 10yr contract has traded through key short-term support and the bear trigger at 109-02+, the Nov 15 low. The breach confirms a resumption of the downtrend and opens 108+12+, a Fibonacci projection.

- Cash tsys yields closed December 31 higher, with the 10yr trading to 4.569% just off the monthly highs of 4.635%. The 2s10s curve is at its steepest levels for the past year at 32.5bps, while the 2s30s closed the year at 54bps, just shy of its steepest levels set back in September of 60bps.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer, AU-US 10Y Diff. Tighter, Q3 GDP Tomorrow

Dec-03 04:41

ACGBs (YM +2.0 & XM +2.5) are richer but off Sydney session bests.

- The net export contribution to growth in Q3 was 0.1pp, less than expected, but the strongest public demand contribution since Q1 2022 means that GDP forecasts are likely to be little changed or maybe skewed to the upside.

- Real public demand grew 2.4% q/q after 0.9% in Q2. It is expected to contribute 0.7pp to GDP tomorrow. The increase was driven by state & local government expenditure and public GFCF.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session. Focus now turns to Wednesday's ADP private employment and ISM data ahead of Friday's non-farm payroll release.

- Cash ACGBs are 2-3bps richer with the AU-US 10-year yield differential at +10bps.

- Swap rates are 2bps lower.

- The bills strip has bull-flattened, with pricing flat to +3.

- RBA-dated OIS pricing is flat 4bps softer for 2025 meetings. A 25bps rate cut is not fully priced until May.

- Tomorrow, the local calendar will see S&P Global PMI Composite & Services and Q3 GDP data alongside AOFM’s planned sale of A$700mn of the 3.25% 21 April 2029 bond. The AOFM also plans to sell A$800mn of the 3.75% 21 April 2037 bond on Friday.

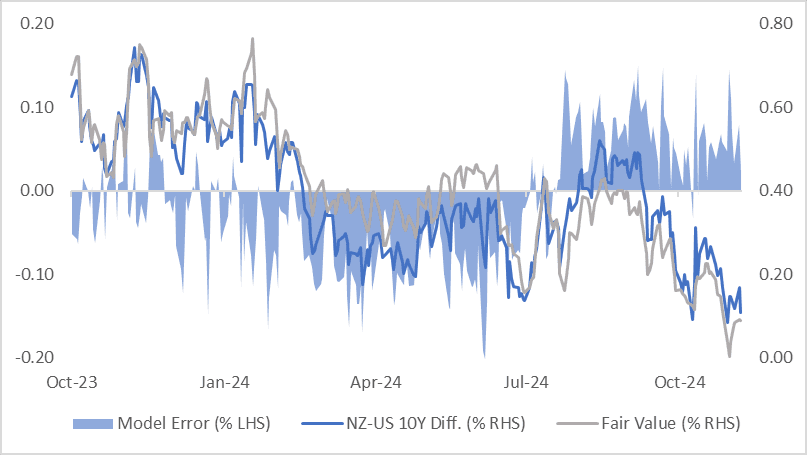

BONDS: NZ-US 10Y Differential Lowest Since Mid-2021

Dec-03 04:18

NZGBs closed the day in a bull-flattening pattern, with benchmark yields ending flat to 4bps lower.

- The 10-year NZGB slightly outperformed, with the NZ-US and NZ-AU 10-year yield differentials tightening by 1-2bps.

- The NZ-US 10-year differential, now at +10bps, is hovering near its tightest levels since mid-2021.

- A simple regression analysis of the 3-month forward swap rate spread (1Y3M) over the past year indicates the 10-year yield differential is close to its estimated fair value of +9bps.

- Notably, the regression error has fluctuated within a range of ±20bps over the past year, highlighting some variability in the relationship.

- The 1Y3M differential continues to be a key driver of market expectations for long-term yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

OIL: Crude Range Trading Pressured By Stronger US Dollar

Dec-03 04:10

Oil prices have been trading in a narrow range and are off their intraday lows to be down slightly on the day. WTI is down 0.1% to $68.18/bbl after a low of $67.91 and Brent is 0.1% lower at $71.93/bbl after falling to $71.68. The stronger US dollar continued to pressure crude (USD BBDXY +0.1%) offsetting mild optimism from China’s manufacturing PMI.

- Cold weather in Europe has increased heating demand boosting natural gas prices, but also distillate which includes heating oil.

- US industry-based inventory data is out later today. Crude stocks have been declining but products rising. The official EIA figures are on Wednesday.

- The focus of the week will be Thursday’s OPEC+ meeting, where it seems likely that supply increases will be pushed out into Q1, and Friday’s US payrolls report.

- Later the Fed’s Daly, Kugler & Goolsbee and ECB’s Cipollone speak. In terms of data, US October job openings and Spanish November unemployment print.