US: Trump's Win In Indiana Primaries Could Lead To Second Redistricting Push

President Donald Trump scored a major political victory in a slate of Indiana state Senate primaries...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: NKY and KOSPI Up Cautiously Whilst SE Asia Losses Mount

With China out, Asia looked to South Korea and Japan as the main markets opened Monday. The AXIOS report ended a weak start with the NIKKEI touching 53,200 early before rebounding back above 54,000, before settling around 53,500 and gains of +0.85%. AI stocks continued to perform from the positive spillover from Microsoft's AI partnership in Japan. Banks continue to deliver modest returns as the higher yield environment bodes well for their balance sheets.

In Korea, Samsung led the charge with gains of over +3.6% Monday driving the KOSPI higher by +1.3%. Early trading was bolstered by reports that the South Korean government is considering a new supplementary budget for the second half of the year to cushion the economy against high oil prices and supply chain disruptions. Banks are performing also given the higher yield environment perceived to have a positive impact. Gains were tempered in the afternoon with investors wary of the April 6 deadline

Malaysia, Thailand and Indonesia have all had a weak start to the trading week with losses of around -0.40% to -0.80% on the ongoing Middle East concern. The woes for the JCI started with concerns over the fiscal spend due to the government's growth objectives, was further pressured by concerns raised by the index provider MSCI (and hence rating agencies) and now the price of oil. This sees the JCI floundering with year to date losses of -19% whilst projecting a full year growth rate of around 5%

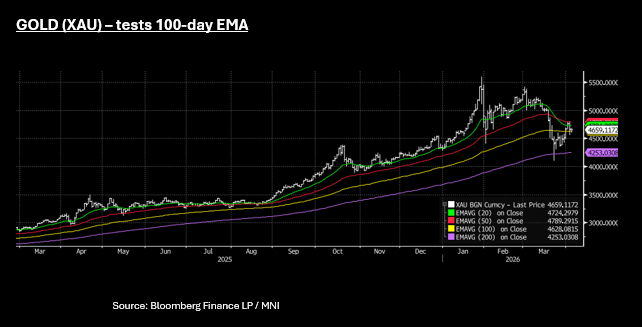

GOLD: Gold Holds Near Key Tech as Trump's Tuesday Deadline Looms

- Despite strengthening in the afternoon session, gold's weak open sees it holding onto modest losses in the Asia trading day.

- Currently near US$4661, gold is down around -0.32%

- This keeps bullions wedged between the 20-day EMA of $4,789 and just above the downside resistance from the 100-day EMA at $4,628.

- Should a break below the 100-day occur, there appears reasonable support at $4,500.

- Gold's next move will hinge on the Trump Tuesday deadline and how the USD and UST Yields react with both markets watching closely for signs of a potential ceasefire.

US TSYS: Yields Edge Higher Ahead of US Open

With so much news to digest US treasuries had a cautious start to the trading week. Yields were higher by around 1 to 1.5bps higher across the curve whilst volumes for futures remained low.

- The 2-Yr is up +1.2bps at 3.858%

- The 5-Yr is up +1.6bps at 4.004%

- The 10-Yr is up +1bps at 4.36%

- The 30-Yr is up +1bps at 4.924%

The rally has seemingly stalled for now as markets look for the next direction. Trump's threat of a Tuesday deadline to open the Strait of Hormuz clashed with reports of a push for a ceasefire of up to 45 days with a pathway to a permanent end (as reported by Axios). This calmed oil markets with WTI around $3 lower than early morning highs.

The outcome of the next 24 hours will dictate the next move in yields as short term momentum indicators remain neutral. A 45 day pause should cap any further move higher, whereas a resumption in US/Israel bombing could see 10-Yr yields back above 4.40%

Looking ahead to Monday, March services PMI is the main focus along with ADP employment change and durable goods.

Auction wise sees a US$13-week US$89bn and a US$77bn 26-week as the primary focus.