ASIA STOCKS: Trump Takes Aim at Pharma

Some of Asia's pharma stocks took a hit today as President Trump aimed his tariff sights firmly in their direction. Pharma shares in Australia, Japan, South Korea and India are down by 2-3% after Trump said in an interview that he will be putting tariffs on Pharmaceuticals.

Following yesterday's better than expected GDP, Indonesia's Jakarta Composite has consolidated above 7,500 over 25% off the March lows.

A government initiative to provide free preschool education has given Chinese childcare related stocks a boost with rises of +2-4% .

- The Hang Seng posted modest gains of +0.18% as it attempts to trade above 29,500. The CSI 300 is up +0.18%, Shanghai Comp is up +0.27% and Shenzhen up +0.55%.

- The Nikkei has had a strong day rising +0.60% after Tuesday's gains of +0.64%.

- The TAIEX in Taiwan is the worst regional performer, down -0.77%

- The KOSPI followed the TAIEX down by -0.18%.

- Malaysia's FTSE KLCI couldn't follow up on yesterday's gains of +0.76% and is lower by -0.16%.

- The Jakarta Composite is one of the best performers in July but could only rise marginally today by +0.08%.

- The FTSE Straits Times is down -0.07% and the PSEi in the Philippines up +0.62%.

- The NIFTY 50 in India declined -0.30% yesterday and has opened marginally lower this morning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

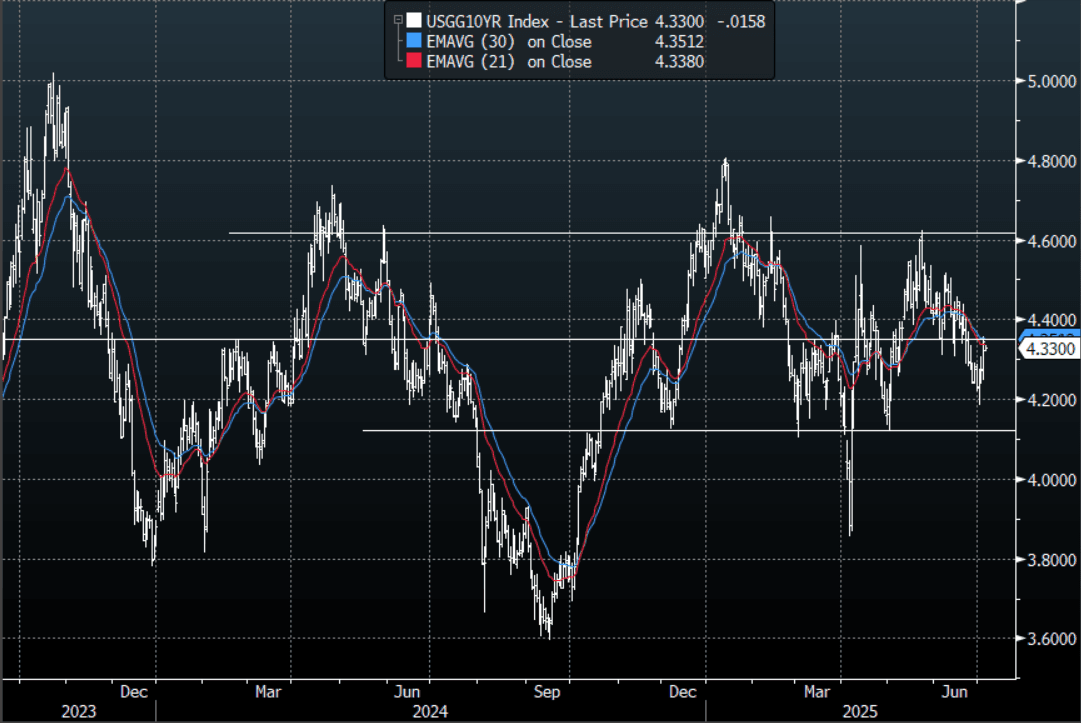

US TSYS: Asia Wrap - Yields Open Lower After Long Weekend

The TYU5 range has been 111-08+ to 111-12+ during the Asia-Pacific session. It last changed hands at 111-10+, up 0-03+ from the previous close.

- The US 2-year yield has moved lower trading around 3.855%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.33%, down 0.02 from its close.

- The 10-year yield saw a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- (Bloomberg) -- The Treasury’s willingness to fund more at the short-end of the yield curve will further compromise the Federal Reserve’s independence and increasingly leave monetary policy de facto in fiscal hands. The dollar will be a casualty, and the yield curve will steepen.

- Data/Events: Bond investors will be focusing on the Fed Minutes and the demand for 10 & 30-year maturities this week.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

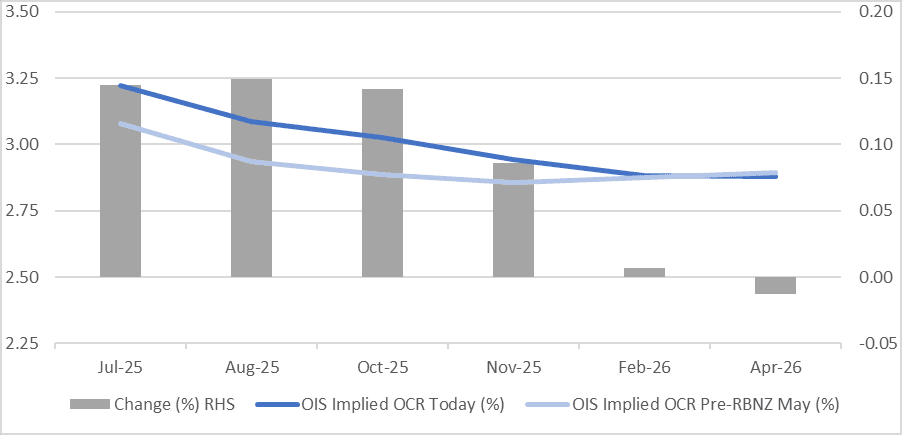

STIR: RBNZ-Dated OIS Firmer Than Pre-RBNZ Decision Levels (May)

RBNZ dated OIS pricing is little changed across meetings today. 3bps of easing is priced for this week's meeting, with a cumulative 31bps by November 2025.

- Notably, pricing is 9-15bps firmer across 2025 meetings compared to pre-RBNZ decision levels on May 28.

- (Bloomberg) -- A majority of members in the NZIER Monetary Policy Shadow Board recommend that the Reserve Bank of New Zealand keep the cash rate on hold at 3.25% at the July 9 review. While activity remains soft in the New Zealand economy, there are both upside and downside risks to inflation in the near term, given the recent pick-up in annual CPI inflation and heightened global risks.

Figure 1: RBNZ Dated OIS Today vs. Pre-May RBNZ Decision Levels (%)

Source: MNI - Market News / Bloomberg

CHINA: Bond Futures Drift Lower in the Morning Session

- China's bond futures have drifted marginally lower in a lackluster trading session this morning despite a sizeable liquidity withdrawal from the OMO.

- The 10yr is down -0.01 to 109.10 to maintain its position above all major moving averages. The nearest being the 20-day EMA of 109.02

- The 2yr is down -0.01 at 102.50 and is between the 50-day EMA of 102.50 and the 20-day EMA of 102.49

- The CGB 10yr is at 1.64%.

- Wednesday sees the release of June PPI and CPI, which have both struggled to post positive outcomes in recent months.