US: Trump Struggles To Sell Trade Agenda To Voters

Feb-23 18:39

G. Elliot Morris at Strength in Numbers reports: https://www.gelliottmorris.com/p/trump-decides-hell...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

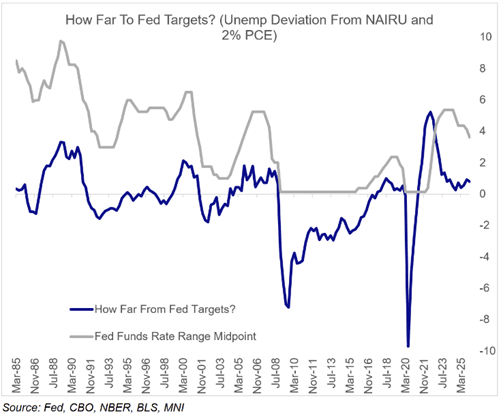

FED: MNI Fed Preview - January 2026: New Year, Same Divisions

Jan-23 22:16

We've published our preview of the January FOMC meeting - Download Full Report Here

- The FOMC's January meeting appears poised to deliver a neutral hold, with heated debate continuing about the appropriate pace of easing over the coming year.

- Divisions within the FOMC over the way forward are unlikely to have narrowed much since the December cut. The center of the Committee is likely to hold sway in maintaining an easing bias, albeit with no rush to make the next move now that rates have been brought down to within plausible estimated ranges of neutral policy.

- If anything, the Committee may be even more patient now than it was 6 weeks ago.

- Recent data have done little on net to affirm the case for another near-term cut, with the unemployment rate steadying and economic activity proving more resilient than expected.

- With government shutdown-related distortions failing to clarify the overall picture, Chair Powell is likely to repeat his message from the December meeting that the FOMC is "well positioned to wait to see how the economy evolves", with plenty of data to consider before the next decision in March.

- The new Statement is likely to see only limited changes, but should acknowledge both reduced near-term concerns over the labor market as well as the above-expected economic activity since the last meeting. It will maintain the rather vague forward guidance adopted in December that the “extent and timing” of future easing will depend on the data.

- That would likely be taken in stride by rate markets which price only around a 3% implied probability of a 4th consecutive 25bp cut, with the next easing expected only by July.

- Our roundup of analyst expectations will be published on Monday January 26.

USDCAD TECHS: Reversal Extends

Jan-23 21:00

- RES 4: 1.4023 76.4% retracement of the Nov 5 - Dec 26 bear leg

- RES 3: 1.3977 High Dec 4

- RES 2: 1.3950 61.8% retracement of the Nov 5 - Dec 26 bear leg

- RES 1: 1.3852/3929 50-day EMA / High Jan 16

- PRICE: 1.3743 @ 16:06 GMT Jan 23

- SUP 1: 1.3734 Low Jan 23

- SUP 2: 1.3710 76.4% retracement of the Dec 26 - Jan 16 bull leg

- SUP 3: 1.3643 Low Dec 26 and the bear trigger

- SUP 4: 1.3576 Low Jul 23 ‘25

Recent weakness in USDCAD appears corrective - for now. However, price has breached support at the 20-day EMA, at 1.3833, and continues to trend lower. This highlights a stronger reversal and signals scope for a deeper retracement - towards 1.3710, a Fibonacci retracement. Key short-term resistance and the bull trigger has been defined at 1.3929, the Jan 16 high. A move through this hurdle is required to reinstate the recent bull theme.

US TSYS: From Pieces of Ice to Naval Blockades, Geopol Risks Rattle Markets

Jan-23 20:50

- Treasuries extended session highs late - revisiting late overnight highs - possibly spurred by geopol risk again, Politico reporting the US is weighing a naval blockade of Cuba oil imports. Note WTI Crude had risen (+1.78 at 61.14 late) as the market assesses Iran-related geopolitical risks amid building military presence in the region alongside disruption to Kazakhstan’s oil output.

- Earlier data saw Treasury futures gain after flash PMI data comes out slightly lower than anticipated (Services steady to a tick higher for Mfg & Composite vs. prior release): January's flash PMIs came in slightly on the soft side of consensus, with Manufacturing at 51.9 (52.0 expected, 51.8 prior) and Services 52.5 (52.9 expected, 52.5 prior).

- Treasury futures extended higher after UofM sentiment gains while inflation expectations for 1Y and 5-10Y recede slightly: Consumer Sentiment, an index of 56.4 represented a 5-month high (better than the 4-month high implied by the initial 54.0). Main change was on the near-term inflation front, with 1Y expectations at 4.0% (4.2% prelim) for the lowest since January 2025 (5-10Y was revised down 0.1pp to 3.3% to remain in the general range of the prior 2 months).

- TYH6 currently +3.5 at 111-22.5 vs. 111-23.5 high. Curves mildly mixed: 2s10s -.402 at 63.293; 5s30s +.569 at 99.609. Initial firm resistance is at the 20-day EMA, currently at 112-03.

- The Japanese yen has been the main topic of conversation in currency markets Friday, as a sharp turn lower for USDJPY has prompted mounting speculation that the Ministry of Finance may have intervened. This has all followed the Bank of Japan holding rates unchanged during the APAC session, and while maintaining a hiking bias, Governor Ueda failed to provide any firm details surrounding the tightening timeline.

- Focus turns to next week's FOMC policy announcement on January 28.