SECURITY: Trump Says EU Must Halt RU Oil Purchases, Defers Penalties For Putin

Sep-04 14:31

President Donald Trump has again warned of consequences for Russia if President Vladimir Putin doesn’t agree to a meeting with Ukrainian President Volodymyr Zelenskyy.

- Trump told Zelenskyyy/Euro leaders that “there could be consequences if they don't meet”, per WH official quoted by Reuters. Trump added: “We'll see what happens over week or two, at that point I’ll step in,” appearing to punt a possible US response to Moscow.

- According to the official, Trump told European leaders, “Europe must stop purchasing Russian oil” and place economic pressure on China, for funding Russia's war efforts."

- Trump’s comments suggest that he is willing to extend an informal deadline for Putin to make progress on a ceasefire, perhaps in response to Putin’s statement yesterday that he would meet Zelenskyy in Moscow, an offer that Kyiv is unlikely to accept.

- Semafor noted this morning that Trump’s, “July-issued deadline for Russia to end the war within 50 days expired on Tuesday.... The subsequent two-week deadline he set last month for Russia-Ukraine peace talks lapses Friday — and that will likely bring renewed calls for Congress to pass bipartisan sanctions.”

- Reuters notes that French President Emmanuel Macron said “26 countries” committed to taking part in “reassurance force in Ukraine,” adding that US support to security guarantees will be financial in the “next few days.” However, it should be noted that the ‘coalition of the willing’ is discussing a security architecture for a peace deal that now appears remote, rather than strategy for achieving peace.

- Macron and Finnish President Alexander Stubb both hinted that the US could join new EU sanctions on Russia if Russian oil purchases are halted, per Reuters.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION PREVIEW: On offer next week

Aug-05 14:31

The DMO has announced it will be looking to sell GBP4.75bln of the 4.375% Mar-30 Gilt (ISIN: GB00BSQNRD01) at its auction next Tuesday, August 12.

STIR: Fed Rates Look Through A Mixed ISM Services Report

Aug-05 14:28

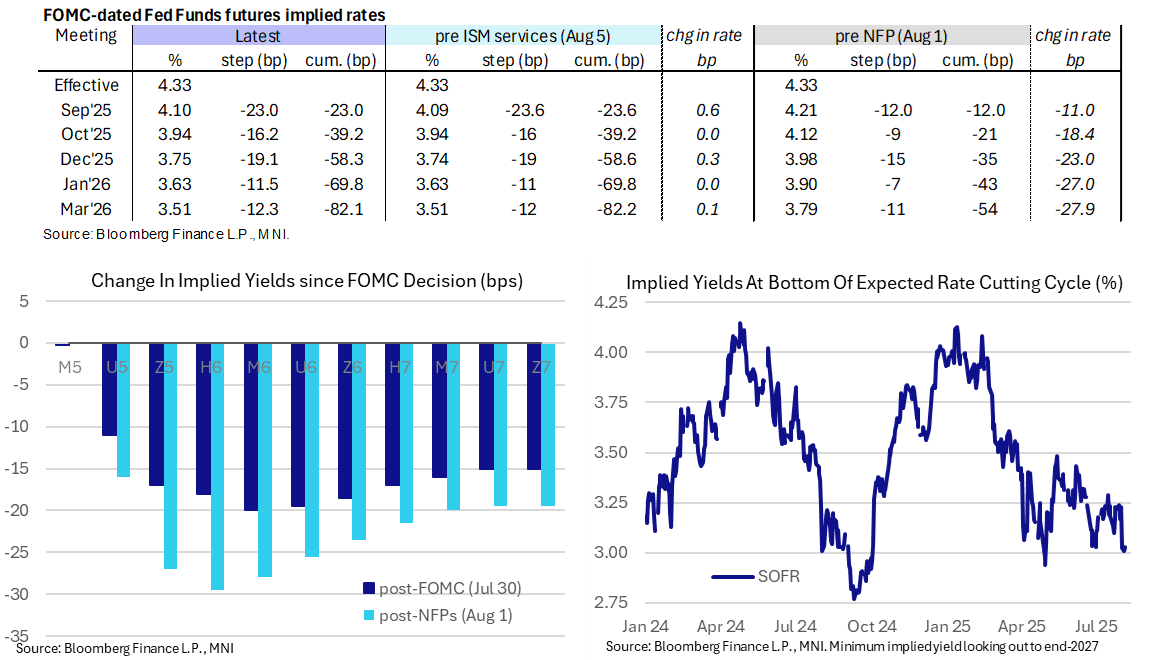

- Fed Funds implied rates have seen almost no reaction to the ISM services report for July, rising at most 0.5bp for meetings out to 1Q26.

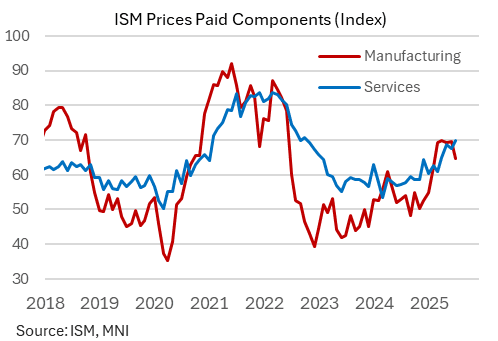

- The overall index underwhelmed in July at 50.1 (cons 51.5) after 50.8 in contrast to a strong rise in the S&P Global US services PMI, but prices paid surprisingly increased to 69.9 (cons 66.5) after 67.5 for a fresh high since late 2022.

- Cumulative cuts from 4.33% effective: 23bp Sep, 39bp Oct, 58.5bp Dec, 70bp Jan and 82bp Mar.

- Echoing the growth negative aspects of the report, the SOFR implied terminal yield of 3.03% (SFRH7) is 1bp lower post-ISM to limit the day’s increase to 2bp.

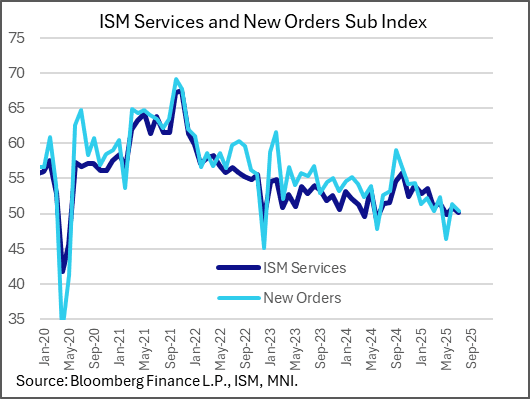

US DATA: ISM Services Points To Stagflationary Developments Amid Tariffs

Aug-05 14:25

July's ISM Services data were more "stagflationary" than anticipated, with a dip in activity amid a pickup in price pressures. The report overall suggests that firms' tariff-related concerns linger, with momentum failing to build on a brief improvement in June. Combined with the headline index, the subcomponents of the survey show a clear slowing in activity since late 2024.

- The headline Services PMI reading fell by 0.7 points to 50.1 (51.5 expected, 50.8 prior), merely a 2-month low but suggesting that an expected pickup in momentum and sentiment is not materializing. The ISM report writes that the index is consistent with 0.5% annualized real GDP growth. Business activity fell 1.6 points to 52.6.

- The main worrying point was new orders, which fell 1 point to 40.3 (no expectations). That was led by a 3.2 point drop in new export orders (47.9) - which apart from March 2025's tariff driven low (45.8) was the joint-weakest since March 2023. Imports fell 5.8 points from 51.7 - one firm's anecdote was “Imports have increased in price, to be less competitive than domestic vendors.”

- Employment, too, was a weak spot - down 0.8 points at 46.4, it's now declined in 2 consecutive months after a brief return above the 50.0 mark in May. It's now been below 50 in 4 of 5 months (i.e. contractionary). However, the anecdotes of the latest report make it difficult to know whether this squares with the broader "low hiring, low firing" theme in data elsewhere, with firms reporting supply-side restraints rather than weaker demand ("Comments from respondents include: “Lost a few service technicians; still difficult to recruit in this market” and “We have lost employees due to normal attrition and are having issues backfilling these positions with qualified candidates.”)

- Inventories fell by a second consecutive month, by 0.9 points to 52.7 (further evidence of pre-tariff buildup reversing; inventory sentiment pointed to inventories were "too high" at 53.2 albeit down from 57.1 prior and the lowest since Oct 2024), while supplier deliveries rose 0.7 points to 51.0 (slower supplier deliveries, which is a positive for the headline reading).

- Prices paid meanwhile ticked up 2.4 points to 69.9 (66.5 expected, 67.5 prior), a fresh 33-month high. While MNI had flagged potential upside risks to the prices reading, based on regional Fed surveys and the flash PMI report, this was even higher than we would have anticipated and defies a pullback in its manufacturing counterpart.