SECURITY: Europeans Ready To Provide Security Guarantees To Kyiv - Macron

Macron echoes European rhetoric of readiness to provide security guarantees to Kyiv but we await further details. Earlier today, NATO Secretary General Mark Rutte said he expects clarity at a summit of Ukraine's allies on Thursday "or soon after" on what security guarantees Europe can offer Kyiv after Russia's war in Ukraine comes to a halt.

- "*MACRON: EUROPEANS READY TO PROVIDE SECURITY GUARANTEES TO KYIV

- *ZELENSKIY: UNION OF EUROPE AND US WILL HELP PRESSURE RUSSIA

- *UKRAINIAN PRESIDENT ZELENSKIY SPEAKS IN PARIS ALONGSIDE MACRON" - bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

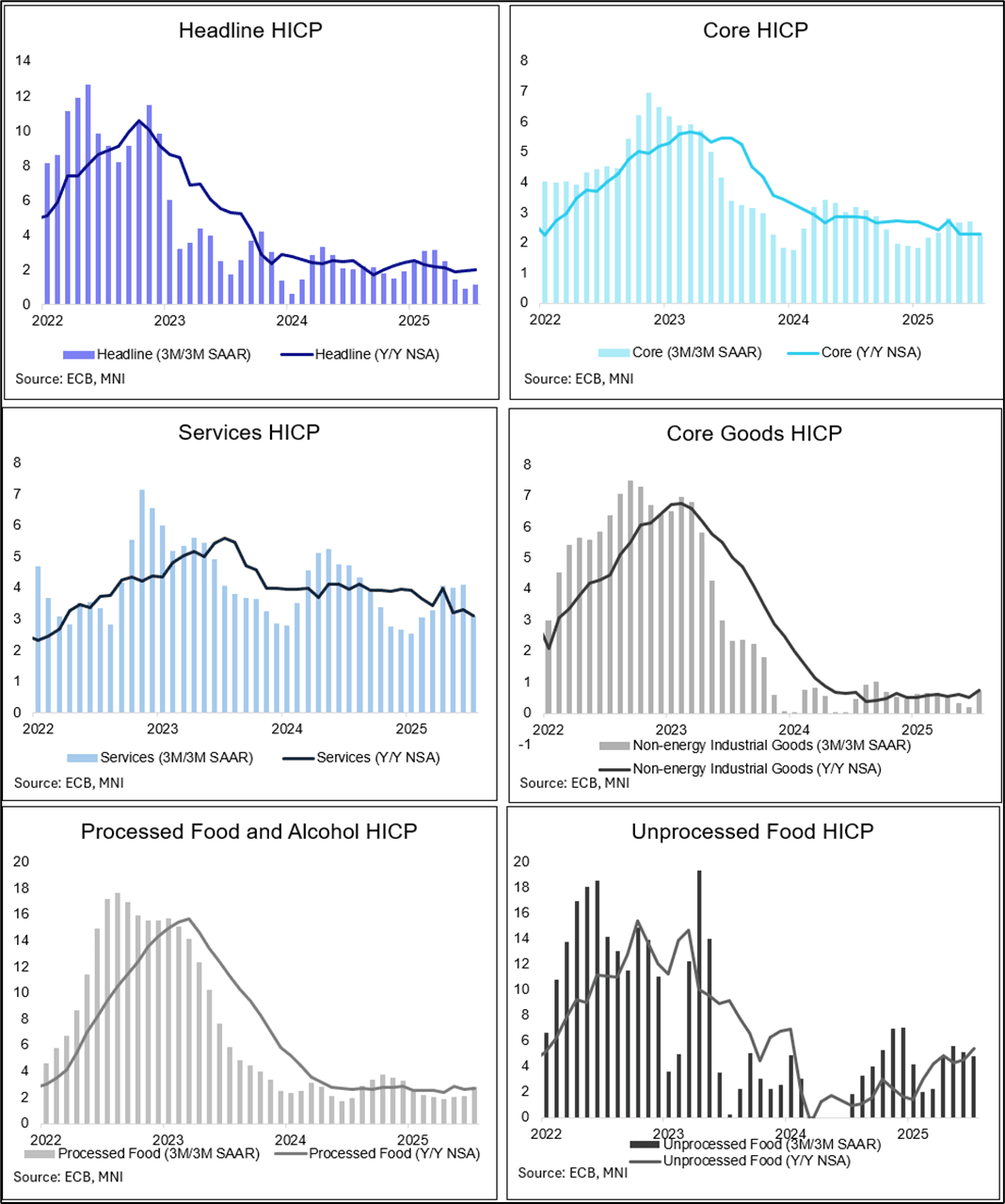

EUROPEAN INFLATION: July SA Data Questions Narrative Around Residual Seasonality

The ECB’s seasonally adjusted data on the July inflation round (released Friday) saw Eurozone core inflation at 0.24% M/M in July after 0.30% in June. Services prices rose 0.17% M/M (vs 0.45% prior), while non-energy industrial goods prices rose 0.36% M/M (vs 0.04% prior).

- This brought down much-eyed services ‘momentum’ (3m/3m SAAR) to 3.07%, materially below the 4% level around where it stood for the last three months. Crucially, July’s drop comes in the summer period, which during the last two years was characterized by well elevated readings – prompting some questions around residual seasonality in the ECB seasonally adjusted data. This year’s July developments pose a counterargument to such a narrative, pointing in favour of ongoing disinflation even if at 3.1% it’s still only back in line with the 3.1% Y/Y.

- Momentum in non-energy goods inflation meanwhile ticked up in July to 0.71% (0.21% prior). This was the highest reading since last September, with the increase since June potentially underpinned by changing or less material seasonal summer clothing sales, national-level data suggests.

EURUSD TECHS: Corrective Cycle

- RES 4: 1.1851 High Sep 10 2021

- RES 3: 1.1829 High Jul 01 and the bull trigger

- RES 2: 1.1789 High Jul 24

- RES 1: 1.1617 20-day EMA

- PRICE: 1.1562 @ 17:15 BST Aug 4

- SUP 1: 1.1401 Low Jul 30 and a bear trigger

- SUP 2: 1.1373 Low Jun 10

- SUP 3: 1.1313 Low May 30

- SUP 4: 1.1184 38.2% retracement of the Feb 3 - Jul 1 bull cycle

Despite Friday's rally, EURUSD maintains a bearish tone. The recent breach of key support at the 50-day EMA, at 1.1548, highlights a stronger reversal and the start of a correction. This opens 1.1373 next, the Jun 10 low. Firm resistance is seen at 1.1617, the 20-day EMA, where a break is required to signal a reversal. Today’s gains highlight a key short-term support and bear trigger at 1.1401, Jul 30 low. A break would resume the downtrend.

FOREX: USD Stabilizes, But Little Sign of a S/T Bounce

- Following Friday's sharp downdraft in the USD, FX markets were more stable Monday, with the USD pulling back only a small part of the post NFP weakness. The ICE USD Index saw some support into the 50-dma at 98.303 - however Monday's price action took the form of stabilization rather than any bounce in prices.

- The more stable market Monday aided a recovery in GBP. GBP/USD traded either side of the 1.33 handle - topping Friday's high in the process. Moves come ahead of this Thursday's BoE decision at which markets fully discount a 25bps rate cut. The vote split among the MPC will be carefully watched as a clue for future easing plans across the second half of the year. The bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

- JPY was the firmest in G10 - prompting a second session of losses for USD/JPY. The rate is now through Friday's low and going further to erase the rally off the mid-July low. Layered support comes in between 145.71 - 145.86 - marking the confluence of the 100-dma, 50-dma and the mid-July lows.

- Meanwhile, CHF was the weakest in G10 - seeing very little reprieve from Trump's decision to install some of the most sizeable tariffs against Switzerland. Reports that the Swiss government are to make a more attractive offers as part of negotiations did little to reverse the CHF weakness, which sees USD/CHF continue to trade either side of the 0.8074 50-dma.

- Focus Tuesday rests on China composite and manufacturing PMI data, final PMI prints across Europe and the US as well as the US ISM services index for July. BoJ minutes are the sole central bank release in G10 - however any further commentary from Fed officials will be carefully watched considering the focus on who could replace Fed's Kugler after her resignation over the weekend.