US: Trump Remarks On Economy And Affordability Underway Shortly In Rome, GA

US President Donald Trump is shortly due to deliver remarks on the economy and affordability in Rome...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Retracement Mode

- RES 4: 1.4023 76.4% retracement of the Nov 5 - Dec 26 bear leg

- RES 3: 1.3977 High Dec 4

- RES 2: 1.3950 61.8% retracement of the Nov 5 - Dec 26 bear leg

- RES 1: 1.3929 High Jan 16

- PRICE: 1.3814 @ 16:18 GMT Jan 20

- SUP 1: 1.3790 Low Jan 7

- SUP 2: 1.3752 Low Jan 6

- SUP 3: 1.3701 Low Jan 2

- SUP 4: 1.3643 Low Dec 26 and the bear trigger

USDCAD has pulled back from last week’s high. The move down appears corrective - for now. However, price is testing support at the 20-day EMA, at 1.3839. A clear break of this EMA would highlight a stronger reversal and signal scope for a deeper retracement - towards 1.3752, the Jan 6 low. Key Short-term resistance and bull trigger has been defined at 1.3929, the Jan 16 high. Clearance of this level would open 1.3950, a Fibonacci retracement.

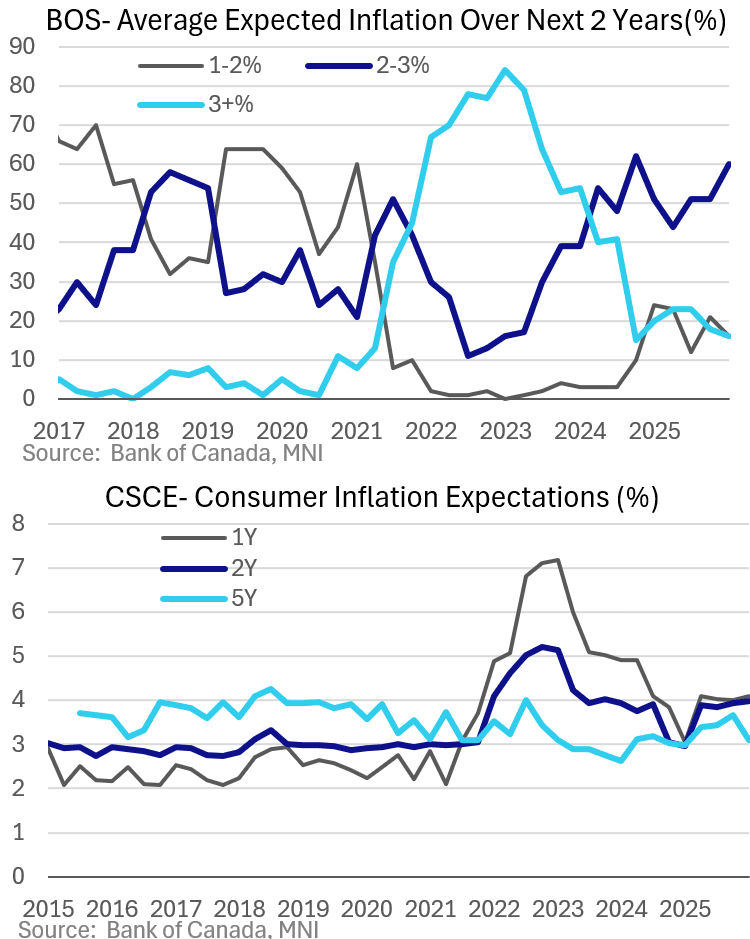

CANADA DATA: BOC Surveys More Mixed On Inflation Outlook (3/3)

The Bank of Canada's quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations (CSCE) for 4Q 2025 were a little more mixed on the inflation front than the CPI data released earlier in the session.

- The BOS showed the share of firms seeing inflation 2% or above increase to 76% (60% of which was 2-3%) from 69% prior (16% apiece saw 1-2% or 3+%).

- And the CSCE showed household views of inflation in one year climbed to 4.1%, highest since 1Q 2024, from 4% prior. 2Y out price expectations edged up marginally to 4.0% for a post 3Q 2023 high. But the BOC will be encouraged that longer-term expectations are diminishing: the 5-year out expectation was 3.1%, down from 3.7% a quarter prior.

- Bank of Canada Governor Macklem's comment last month that "inflation pressures continue to be contained" is likely to be repeated in some form at the January decision next week.

- We will be interested to hear how Governing Council interprets the latest mixed data, though we doubt there will be much change in the inflation outlook in the quarterly Monetary Policy Report (which showed CPI inflation Y/Y projected to come in at 2.2% in 4Q 2026 and 2.1% in 4Q 2027) despite a slight overshoot for 4Q 2025 vs October's expectations (2.2% Y/Y vs the 2.0% projected; trim/median was 0.1pp below the 2.9% expected).

- BOC rate hike pricing was little changed after the data and surveys released January 19. Near-term cuts are slightly priced from the current policy rate of 2.25%, with about 12bp of hikes on aggregate seen through the year as a whole.

US TSYS: Rates & Stocks Extending Lows as Trade Tensions Heat Up Again

- Treasuries look to finish broadly lower Tuesday, initial weakness tied to JGBs meltdown over fiscal concerns, Tsys accelerating the sell-off as trade tensions reignited after Trump’s threat to impose tariffs on countries opposing his plans for Greenland.

- Indexes gapped lower this morning after Trump’s threat to impose tariffs on countries opposing his plan to control Greenland: 10% tariffs on Denmark, Norway, Germany, the UK, France, the Netherlands, Sweden, and Finland by February should they continue to oppose the sale of Greenland to the US, which would increase to 25% by June.

- The Mar'26 10Y contract has fallen back to appr mid-August level, TYH6 currently -11 at 111-13 (111-09 low vs. 111-31.5), confirming a resumption of the bear cycle and paves the way for an extension towards the 111-00 handle next. A head and shoulders reversal pattern on the daily chart also highlights a bearish threat.

- Tsy curves twist to the steepest levels in 4 years with the short end holding steady: the 2s10s curve taps 70.868 high - steepest level in 4 years - currently +6.095 at 69.361; 5s30s +3.827 at 105.782 vs. 109.328 high.

- Limited data: The ADP Pulse weekly private payrolls tracker showed a slowdown in the 4 weeks to Dec 27, with a 4-wk moving average in the net week/week change falling to 8.0k from 11.25k for the lowest since the Nov 22nd wk.

- The Philadelphia Fed's Nonmanufacturing Business Outlook Survey saw a substantial improvement in January, with softer inflation evident. This is another positive sign for services sector activity momentum (ISM Services posted a 14-month high in December) going into 2026, following the improvement in the NY Fed's equivalent index.

- The Supreme Court opted to not comment on Pre Trump's IEEPA tariff actions for the third time (and no word as to when they may make any comments).