IRAN: Trump - Iran Wants To Make A Deal Badly

May-19 23:41

"TRUMP ON IRAN: THEY WON'T HAVE A NUCLEAR WEAPON - [RTRS]" *TRUMP: IRAN WANTS TO MAKE A DEAL BADLY" ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Higher Overnight Friday Ahead Of Weekend's M/E Events

Apr-19 23:39

In post-Tokyo trade, JGB futures closed stronger, +17 compared to settlement levels, after US tsys finished Friday 5-7bps richer.

- However, US 10-year and US equity futures are lower and oil higher today following news of the US Navy Seizing an Iranian ship in the Straits of Hormuz and Tehran firing at vessels. In a chaotic weekend for newsflow as a former commander in Iran's Islamic Revolutionary Guards Corps told the BBC that Iran will never give up control of the Straits of Hormuz.

- Despite U.S. negotiators arriving in Pakistan for proposed second round of peace talks, Iranian state media is reporting that Tehran has no current plans to attend. Iran is demanding the immediate lifting of the naval blockade as a prerequisite for any further dialogue.

- "What's the price of real oil amid the Mideast uncertainty? The answer isn't so simple, writes Javier Blas. It depends on what kind of crude is being sold, when it's being sold and where, with prices ranging from $78 a barrel in Kansas to $286 in Sri Lanka. " - BBG

- "The UAE asked the US for a financial backstop in case the Iran war plunges the country into a deeper crisis, the WSJ reported." – BBG

- Today, the local calendar will see the Tertiary Industry Index and Tokyo Condominiums for Sale data.

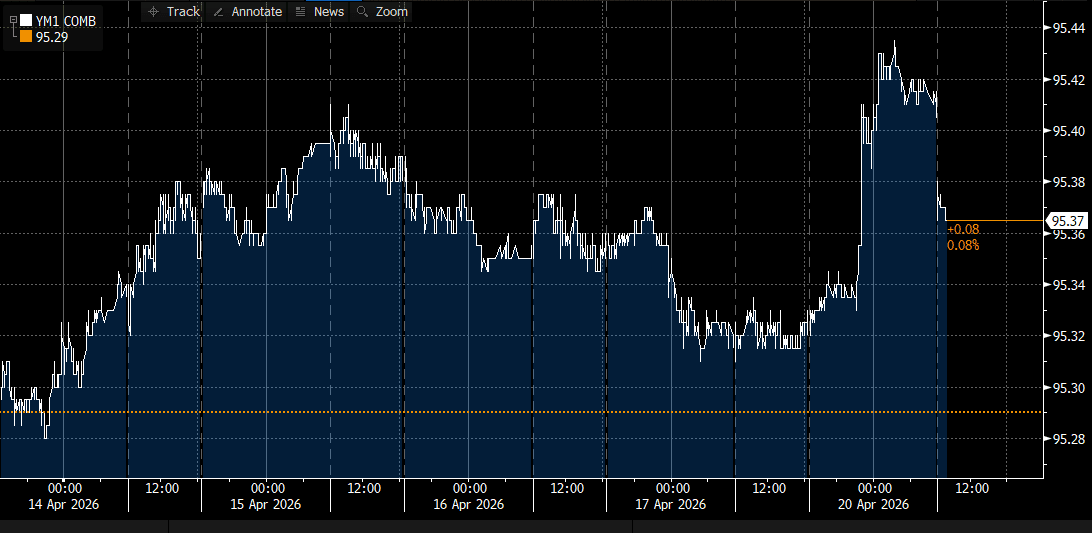

AUSSIE BONDS: Futures Richer But Below SYCOM Highs After Weekend's M/E News

Apr-19 23:34

ACGBs (YM +4.0 & XM +4.0) are stronger but off Friday’s SYCOM bests following the weekend’s Middle East developments. US tsys had finished Friday 5-7bps richer, but US 10-year futures are lower today.

- Despite U.S. negotiators arriving in Pakistan for proposed second round of peace talks, Iranian state media is reporting that Tehran has no current plans to attend. Iran is demanding the immediate lifting of the naval blockade as a prerequisite for any further dialogue. State news described the current outlook for negotiations as non-existent, given the seizure of the ship as a primary reason for the diplomatic freeze.

- Bloomberg - "Australia's fuel reserves rose last week, with more on the way, Energy Minister Chris Bowen said, easing concern of shortages."

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at +71bps.

- The bills strip has bull-flattened, with pricing +1 to +4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 75% for May to 57% by August and 218% by December 2026.

- Today, the local calendar will be empty.

- This week, the AOFM plans to sell A$1000mn of the 3.75% 21 April 2037 bond on Wednesday and A$1000mn of the 2.50% 21 May 2030bond on Friday.

Bloomberg Finance LP

CHINA: Data Preview: Loan Prime Rates

Apr-19 23:16

- The PBoC is widely expected to keep its benchmark lending rates unchanged next week. Market consensus suggests both the 1-year Loan Prime Rate (LPR) and the 5-year LPR will remain at their current record lows, continuing a streak of stability that has lasted nearly a year.

- 1-year LPR: Expected to stay at 3.00%. This serves as the benchmark for most corporate and household loans.

- 5-year LPR: Expected to stay at 3.50%. This serves as the primary reference for residential mortgages.

- Preliminary data for early 2026 shows resilience, with GDP and industrial output, reducing the immediate urgency for further easing.

- The PBoC has recently focused on maintaining exchange rate stability. Aggressive rate cuts could widen yield differentials and exert unwanted downward pressure on the yuan.

- Rising energy prices linked to geopolitical tensions in the Middle East have clouded the inflation outlook, prompting a more cautious approach from policymakers. The strength of the 1Q GDP result put pays to ideas of a rate cut with authorities increasingly favouring moderately loose but targeted measures—such as subsidies for consumer goods and direct credit for high-tech sectors—over broad benchmark rate cuts