IRAN: Trump Asked Netanyahu Yesterday to Scale Back Lebanon Strikes: NBC

Apr-09 15:17

Trump asked Israeli PM Netanyahu in a phone call yesterday to scale back Israel’s strikes in Lebanon to help ensure the success of the Iran negotiations, a senior administration official told NBC News.

- From the report:

- “While the Trump administration and Israel have both said Lebanon is not covered by the ceasefire, Israel agreed “to be a helpful partner,” the official said.”

- “The phone call came after Netanyahu publicly vowed on Wednesday to continue striking Lebanon forcefully, the official said. Iranian officials have threatened to respond to strikes and end the ceasefire.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHF: EURCHF Consolidates Back Above 0.90, Bearish Trend Intact

Mar-10 15:10

- After printing a fresh cycle/decade low of 0.8981 on Monday, EURCHF has since stabilised back above the 0.90 mark today, consolidating around 0.9030 across early US trade. EURCHF price action has continued to reflect the Swiss Franc’s relative insulation to the dynamics around central bank re-pricing sensitivity to rising energy costs.

- The pair has seen a consistent decline from mid-January, slipping from 0.9300 to current spot levels, with the 20-day EMA continuing to cap corrective bounces. This was particularly visible last week, when SNB comments on a readiness to intervene prompted a swift short squeeze to 0.9131, perhaps improving short-term positioning somewhat.

- Renewed downside would target a move to 0.8913, the 1.236 projection of the Mar 14 - Apr 11 - Aug 18 2025 price swing. The 1.382 projection is at 0.8849.

- Goldman Sachs think short EURCHF is one of the best hedges against inflation risks from a steeper or more prolonged oil price shock. They cite the Franc as being uniquely well-positioned against rising inflation because the SNB is structurally hawkish and targets inflation below 2%, unlike most other G10 central banks.

- If energy prices and Euro area growth risks remain elevated, GS think EURCHF downside should persist and offers useful inflation protection in this environment, primarily in options formats.

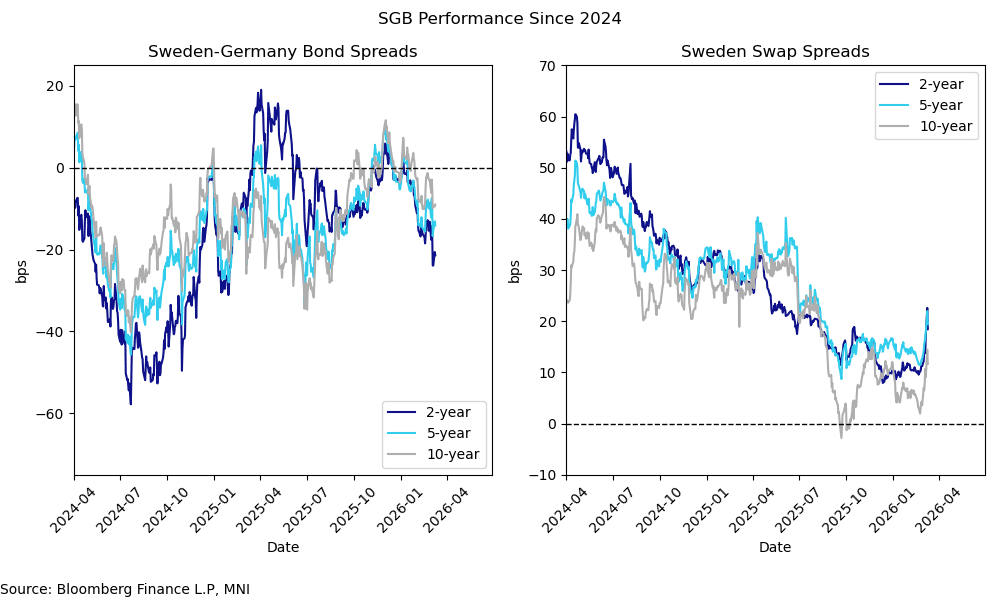

SWEDEN: 10-year SGB Syndi Tomorrow, SGBs Have Performed Strongly This Month

Mar-10 15:04

Sweden will launch the new 10-year Feb-37 SGB via syndication tomorrow. The Debt Office plans to sell SEK20bln, with IPTs set at SGB+5bps area today.

- This will be the first 10-year SGB to be launched via syndication since 2021. The previous three benchmarks were launched via a conventional auctions, with subsequent exchange auctions utilised to build up volumes.

- Demand for SGBs has been resilient since the Middle East war began. Sweden’s AAA rating and healthy fiscal metrics have allowed SGBs to outperform both Bunds and SEK swaps through this period (see charts).

- Monetary policy considerations will have also played a role, with the bar to a Riksbank pivot to hikes much higher than that of the ECB. Although recent rises in energy prices have led to concerns around upside inflation (and inflation expectations) risks in many economies, in the Riksbank's case it may actually help with anchoring expectations around the 2% target in the medium term.

- Danske Bank noted last week that they see FV for the new 2037 SGB at around 2bps above the current on-the-run 2.50% Oct-36 SGB.

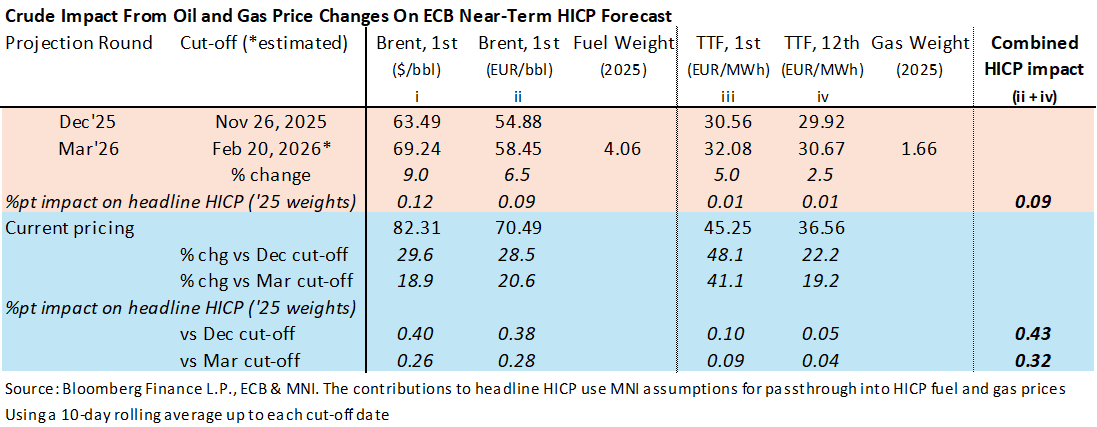

ECB: Taking Stock Of Latest Commodity Price Moves On ECB HICP Projections

Mar-10 14:59

- Next week’s ECB decision will see new economic projections with a likely cut-off on Feb 20, missing the sharp rise in energy prices seen since then despite having reversed yesterday’s huge increases.

- We estimate oil and gas energy prices will have added 0.1pp to near-term HICP inflation compared to the previous December forecasts.

- Were the cut-off to be today, this would have been closer to a 0.4pp boost to HICP inflation, and a little larger if taking a more front-loaded TTF natural gas contract (we use the 12th as a base case to try and account for utility company hedging).

- An important point to consider here: these figures are using a ten-day rolling average per ECB methodology so this recent impact will continue to drift higher if prices stay at current levels.

- The December forecast saw headline inflation revised +0.2pp to 1.9% in 2026 and -0.1pp to 1.8% in 2027, whilst core was revised +0.3pp to 2.2% in 2026 and +0.1pp to 1.9% in 2027.

- Recall that the February ECB press conference saw some comments from President Lagarde which could have been as a subtle critique of the national central bank’s December projection after a soft January inflation reading: “I just want to take you back to the undershooting. We have projected undershooting in 2026 for a long time. And if you go back to our September projections, for instance, which were the last projections conducted by the ECB, we had actually this 1.7%, for the entire year. This was changed and moved up in December. In a way, we are going back to the track that we had anticipated, and this is also what markets and economists are anticipating. But if you look at our medium-term target, which is what we rely upon, we are at 2% in 2028.”

Trending Top

May-22 16:54