USDCAD TECHS: Trend Signals Remain Bearish

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3749 50-day EMA

- PRICE: 1.3697 @ 17:10 BST Jul 16

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD faded fast off intraday highs. The 50-day EMA was very briefly pierced, but sharp intraday volatility dragged the price lower into the close. This affirms the view that short-term gains appear corrective. As such, resistance at the 50-day EMA, at 1.3749 remains valid. A clear break of the EMA would signal scope for a stronger recovery and highlight a possible reversal. For bears, sights are on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend and open 1.3503, a Fibonacci projection.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Instant Answers For June FOMC Meeting

The Instant Answers questions that we have selected for the June FOMC statement and projections are as follows (due to be released at 1400ET Wednesday):

- Federal Funds Rate Range Maximum

- Number of dissenters on size of rate move

- Median Projection of Fed Funds Rate at End of 2025

- Median Projection of Fed Funds Rate at End of 2026

- Median Longer Run Projection of Fed Funds Rate

- Number of 2025 Dots > 4.375%

- Number of 2025 Dots > 4.125%

- Number of 2025 Dots > 3.875%

- Number of 2025 Dots < 3.875%

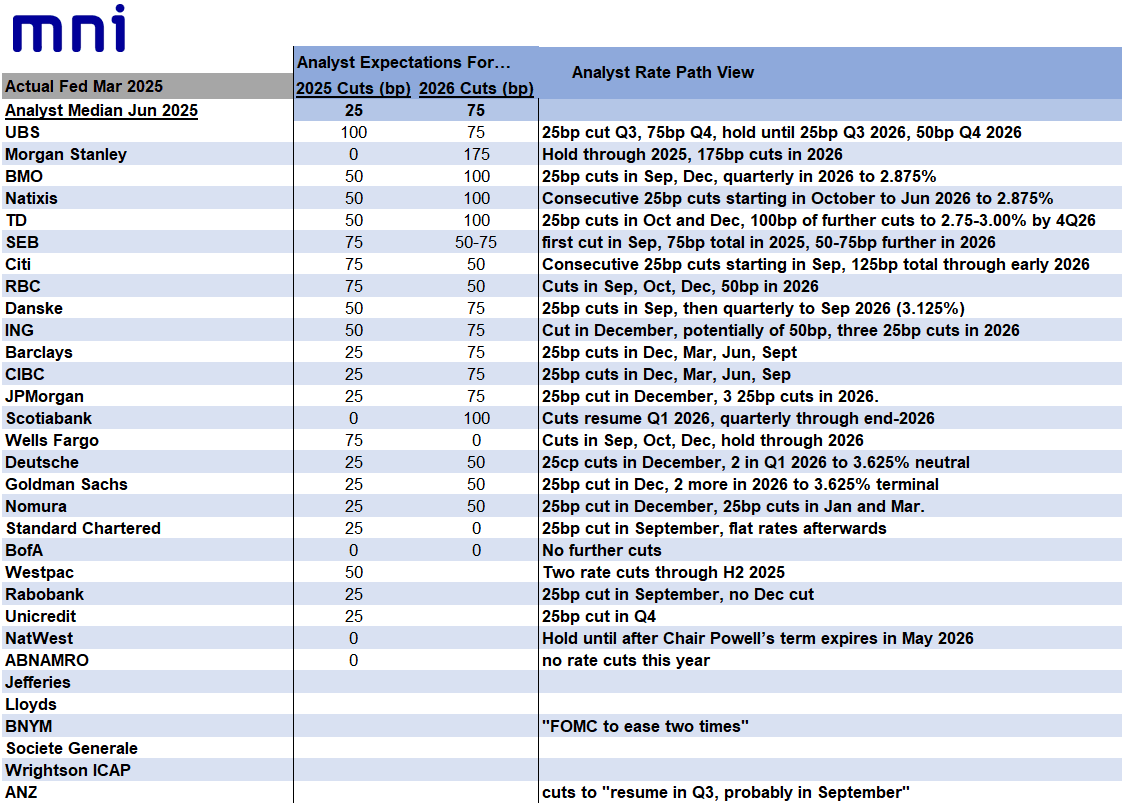

FED: Analysts See 0 To 100bp Of Cuts This Year, Up To 175bp Through 2026 (2/2)

Going into the June FOMC meeting, the median analyst is forecasting the Fed to deliver just 1 cut this year for 25bp of easing, but there is a wide range of opinions which includes 100bp of cuts (UBS) to zero (multiple). See table below.

- Opinion is accordingly split among most analysts about whether the next cut is in September, October, or December.

- The median analyst expectation is for 75bp of cuts in 2026, though again this ranges from no cuts to 175bp of easing (Morgan Stanley).

- The median analyst who has forecasts through both years sees 112.5bp of cuts, or between 4-5.

- UBS and Morgan Stanley see the most total easing (175bp), while BofA sees no further cuts.

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Wages Surprise Hotter

- On the flip side, wage growth has also started to come in hotter. We wouldn’t put too much weight on the surprisingly strong 0.42% M/M increase in average hourly earnings in May in isolation but it followed a strong 6.6% annualized increase in unit labor costs in Q1 (strongest since 1Q24 and before that 3Q22).

- Productivity growth played a role here, falling -1.5% annualized for its first decline since 2Q22 after a period of some particularly strong gains, but the underlying wage growth series was still strong.

- Whilst Powell has previously said he doesn’t expect inflationary pressures to come from the labor market, wage growth is starting to warrant closer inspection.