MNI US Inflation Insight: Tariff Evidence Seeping In

Jul-16 20:45By: Tim Cooper and 1 more...

Inflation+ 1

Download Full Report Here

Executive Summary

- June’s softer-than-expected core CPI reading (0.23% M/M vs 0.29% MNI median, 0.13% prior) came with a notable composition in light of mounting tariff pressures.

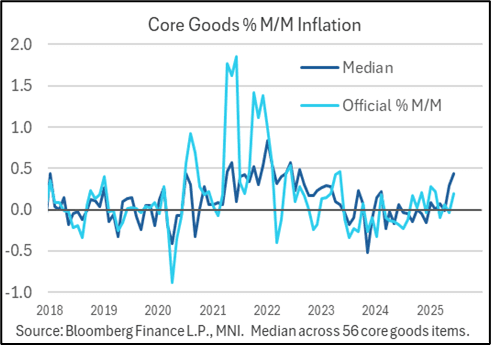

- Namely, core goods inflation was stronger than expected (0.20% M/M vs 0.19% MNI median, -0.04% prior), but that was outweighed by core services slightly on the light side (0.25% M/M vs 0.27% MNI median).

- Ex-vehicle goods inflation jumped in what is arguably the clearest sign yet that tariffs are beginning to seep through into CPI. Indeed there was a broader increase in core goods inflation for a second month, with multiple core goods areas that are seen sensitive to tariffs seeing acceleration including apparel, recreation commodities and household furnishings and supplies.

- Against this backdrop, Regional Fed banks’ estimates of sticky/median Y/Y CPI rates appear to have bottomed in the spring, at least for now, at levels above pre-pandemic averages.

- That said, the June Producer Price Index report was roundly softer than expected - and certainly than feared given the context of rising tariffs - despite some upward revisions to prior. While core goods prices did indeed advance, and there continued to be problematic readings in categories such as durable goods, the rise was consistent with the increases seen over the last 6 months rather than a sudden surge.

- In short, this round of data didn’t settle the question of whether tariff-related price increase would be sufficiently acute to warrant holding rates for an extended period. As noted in the July Beige Book, Fed business contacts’ comments suggested “consumer prices will start to rise more rapidly by late summer."

- Post-PPI estimates of the Fed’s preferred core PCE gauge centered on 0.29% M/M for June vs 0.31% after the CPI report, still an increase from the 0.25% very tentatively eyed ahead of both CPI and PPI releases.

- Through this week’s inflation round, market pricing for Fed easing ended largely steady (with almost 50bp of cuts through end-2025 and a first cut by October), though not before CPI saw cuts pared on the stronger details and then PPI restored some confidence in future easing.

- Overall though, the Fed is set to stay on the sidelines for the summer.