EURGBP TECHS: Trend Outlook Remains Bearish

- RES 4: 0.8448 High Oct 31 and reversal trigger

- RES 3: 0.8376 High Nov 19 and a bull trigger

- RES 2: 0.8356 High Nov 27

- RES 1: 0.8313/29 50-day EMA / High Dec 27

- PRICE: 0.8299 @ 15:18 GMT Jan 3

- SUP 1: 0.8223 Low Dec 19

- SUP 2: 0.8203 Low Mar 7 2022 and a major support

- SUP 3: 0.8200 Round number support

- SUP 4: 0.8188 1.00 proj of the Oct 31 - Nov 11 - 19 price swing

EURGBP is trading closer to its recent highs. Resistance at 0.8313, the 50-day EMA, has recently been pierced - but has so far failed to trigger a sharper move higher. A clear breach of the average would undermine the bear theme and highlight a stronger reversal. A resumption of the primary downtrend would pave the way for a move towards major support at 0.8203, the Mar 7 ‘22 low and the lowest point of a multi-year range.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Thursday Data Calendar: Weekly Claims, Trade Balance, Fed Barkin

- US Data/Speaker Calendar (prior, estimate)

- Dec-5 0730 Challenger Job Cuts YoY (50.9%, --)

- Dec-5 0830 Initial Jobless Claims (213k, 215k)

- Dec-5 0830 Continuing Claims (1.907M, 1.904M)

- Dec-5 0830 Trade Balance (-$84.4B, -$75.0B)

- Dec-5 1130 US Tsy $85B 4W, $80B 8W bill auctions

- Dec-5 1215 Richmond Fed Barkin economic outlook event (no text or media Q&A)

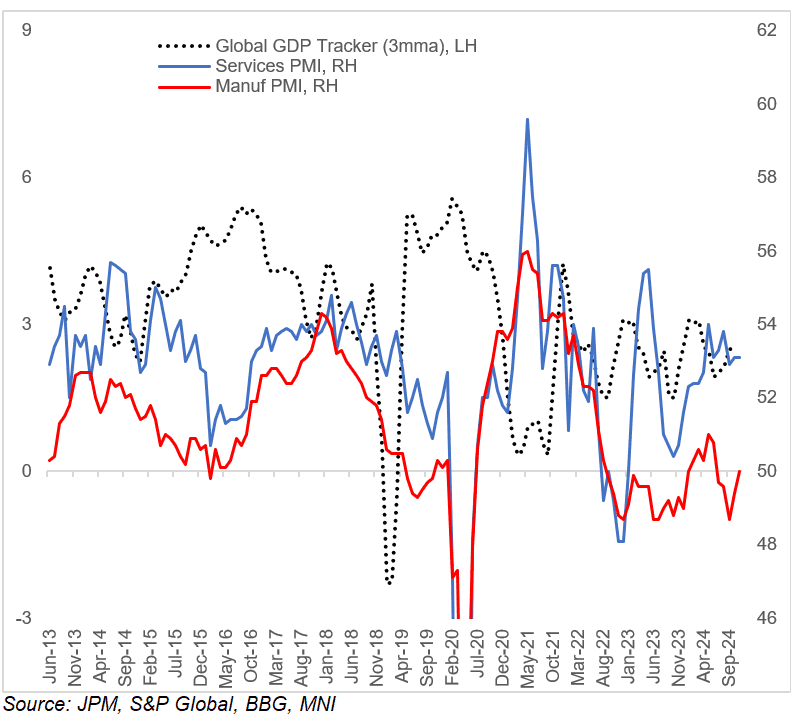

GLOBAL MACRO: Steady Global PMIs Consistent With 2-3% World GDP Growth (1/2)

Global growth was relatively stable in November, per the global aggregate PMIs compiled by JPMorgan/S&P Global made available after Wednesday's publication of final country-by-country data. The Global Composite PMI ticked up 0.1 point to 52.4 - also an improvement from a year earlier when it printed 50.5.

- The improvement was driven by a rise in the manufacturing PMI to 50.0, from 49.4 and marking the first 50+ print since June and indicative of no change vs the previous month. That in turn reflected notable monthly improvements in China and the US, with the Eurozone continuing to lag badly (more on which in a note to follow). Per the report, "output growth remained only marginal at manufacturers, [but] there were some pockets of expansion"

- Services PMI, which has historically been more consistent with overall global GDP growth compared with its manufacturing counterpart, held steady at 53.1. "Solid expansions were seen across the business, consumer and financial services categories, with the strongest rate of increase in the latter."

- Country-by-country composites showed India, Ireland, and the US as the top performers, though China and Japan also expanded - conversely, in the bottom three globally were the Eurozone trio of Germany, France and Italy.

- Inflation looked subdued: input prices fell to the lowest in a year (largely due to weaker costs in developed markets, with EM inflation ricking higher) at 55.7, while output prices (52.1) remained near October's 4-year low.

- Consistent with the composite readings - and the solid sub-categories (particularly Future Output of 62.4, indicating rising optimism) - global real GDP growth looks set to be maintained in the 2-3% range in Q4 - roughly around the levels seen in 2019 pre-pandemic.

STIR: Mixed SOFR Options

- +10,000 SFRH5 95.50/95.75/95.87/96.00 put condors 1.25 ref 95.86

- 11,600 0QZ4 97.00 calls ref 96.27