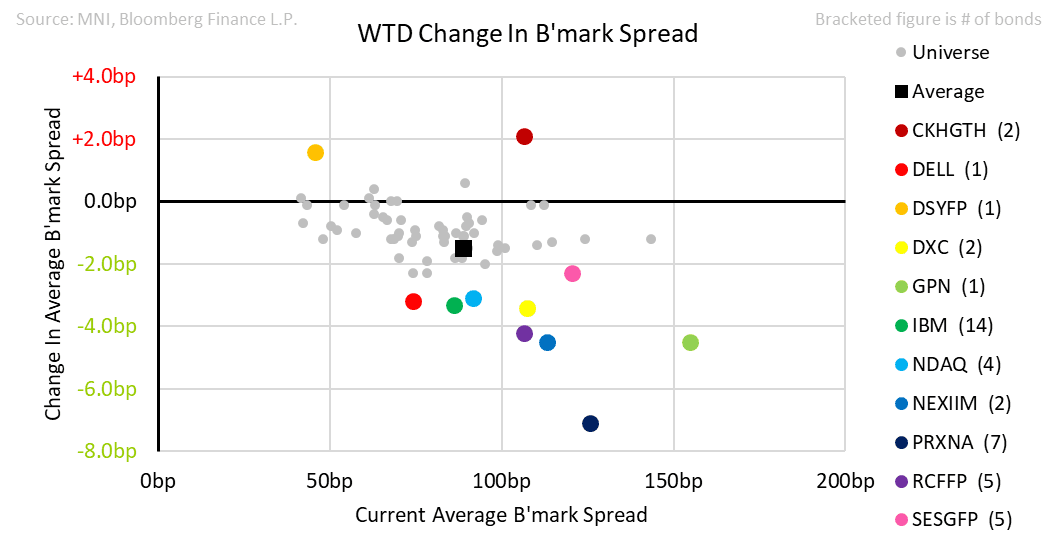

EU TECHNOLOGY: TMT: Week In Review

Aug-15 12:22

- No supply this week. Sole rating action was an upgrade for Nasdaq by S&P.

- Earnings slowed, with only Telstra and CK Hutchison reporting.

- Telstra results were marginally soft but broadly credit neutral with S&P coming out to confirm that higher buybacks will have limited impact on the credit profile.

- CK Hutchison posted steady growth rates. The bottom line was soft on 3-Vodafone integration costs though adjusting for these, the group results were in line. Comments on the call indicated that a ports deal may not materialise this year. Telco-specific presentation here.

- Not much in the way of corporate news given the time of the year; we flagged reports on a Perplexity bid for Google Chrome though the market is very sceptical of a deal materialising.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: MNI POLITICAL RISK - Trump Downplays More Trade Deals By Aug 1

Jul-16 12:21

Download Full Report Here

- President Donald Trump will meet the Crown Prince of Bahrain for an investment-focused bilateral meeting, then sign bills at 15:00 ET 20:00 BST.

- Trump said pharmaceutical tariffs could be announced on August 1, starting low and building to a "very high tariff".

- Trump announced a deal with Indonesia, but downplayed the likelihood of more deals before August 1. He said he could strike “two or three” deals before the deadline and would “probably” impose a little over 10% on smaller countries that did not receive tailored rates.

- Canadian PM Mark Carney conceded that a US trade deal is unlikely to lift all tariffs.

- Lack of retaliation from trading partners has allowed the US to collect duties at a rate that implies USD$240 billion additional revenue per year.

- The Senate will vote on Trump's rescission package this evening after overcoming Republican opposition. Speaker Mike Johnson (R-LA) will take a second run at advancing three crypto bills, after conservatives tanked a rule vote yesterday.

- Trump and OMB Director Vought are hinting that mismanagement of a renovation project could justify Fed Chair Powell's dismissal.

- Trump said he did not advise Ukraine to strike targets deep inside Russia.

- The Pentagon has withdrawn senior officials from the Aspen Security Forum, citing ideological differences. The US and 18 allies began military exercises in Australia.

- Poll of the Day: Favourable views of China have increased, but most countries prioritise strong ties with the US.

Full Article: US DAILY BRIEF

SONIA OPTIONS: SFIZ5 95.75/96.00/96.25 Call Fly Sold

Jul-16 12:15

SFIZ5 95.75/96.00/96.25 call fly 5.5K given at 4.5.

BONDS: Lower Oil Prices Still Providing Support

Jul-16 12:13

Continued downside in crude oil provides background support for core global FI markets, although the recovery from session lows can hardly be deemed a meaningful rally at this stage.

- Overnight/early London highs capped the recovery in TY futures, while Bund futures remain below their pre-CPI UK session highs.

- Little to note in terms of meaningful macro cues since the UK data, with focus on the impending U.S. PPI release after yesterday’s CPI data pointed towards tariff feedthrough into some core goods categories. The usual focus on readthrough into the Fed’s preferred PCE inflation measure will be seen In the wake of the release.

- General themes of fiscal worry remain evident, despite the relief rally in the long end of the JGB curve in Tokyo hours and stabilisation away from lows in wider core global FI through the London morning.

- That leaves bond bears in control from a technical perspective, even with major 10-Year benchmark yields comfortably off year-to-date highs.

- Note that 30-Year German yields remain less than 5bp off their ’23 high, located at 3.263%.