AUDUSD TECHS: Tilted Lower into Close

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6499 @ 16:51 BST Oct 10

- SUP 1: 0.6483 Low Oct 10

- SUP 2: 0.6463 Low Aug 27

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

AUD reversed hard into the Friday close, taking out support at 0.6527/21 in the process. These levels mark the 61.8% retracement for the Aug 21 - Sep 17 bull leg and Low Sep 26 respectively. This hinders the near-term outlook, and puts pause to the underlying bullish theme. For bulls, a reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Goldman At High End Of Core CPI Views On Cars, Airfares

From our inflation preview, at the top end of sell-side analysts' unrounded core CPI expectations is Goldman Sachs seeing 0.36% M/M in August, corresponding to a Y/Y rate of 3.13% (vs. +3.1% consensus).

- Four trends to watch:

- Used car prices seen rising 1.2%, “reflecting an increase in auction prices, and new car prices (+0.2%), reflecting a decline in dealer incentives.”

- Car insurance seen rising 0.4% M/M “based on premiums in our online dataset”.

- Airfares seen rising 3% M/M, “reflecting a boost from seasonal distortions and an increase in underlying airfares based on our equity analysts’ tracking of online price data”.

- “We have penciled in upward pressure from tariffs on categories that are particularly exposed, such as communication, household furnishings, and recreation, worth +0.14pp on core inflation.”

- Their forecast is consistent with core PCE inflation of 0.29% M/M in August.

- They see headline CPI at 0.37% M/M, reflecting higher food (+0.35%) and energy (+0.6%) prices.

- “Over the next few months, we expect tariffs to continue to boost monthly inflation and forecast monthly core CPI inflation around 0.3%. Aside from tariff effects, we expect underlying trend inflation to fall further, reflecting shrinking contributions from the housing rental and labor markets.”

- They see core CPI at 3.1% Y/Y and core PCE at 3.2% Y/Y in Dec 2025 “(or +2.3% for both measures excluding the effects of tariffs)”.

US OUTLOOK/OPINION: Mixed Implications For CPI Hit From Tariff Revenues

Core goods inflation is expected to accelerate a little further in August on a M/M basis and tariff revenues still point to further solid increases ahead, but the pace at which tariff revenues have been closing the gap with implied tariff rates has slowed in recent months.

- Monthly core goods CPI inflation is expected to accelerate in tomorrow’s August release, with analyst expectations averaging 0.3% M/M after two months at 0.2% M/M (including July’s undershooting of then expectations of a 0.4% increase).

- It comes as tariff-driven price increases are generally seen to be getting towards the largest for the year. There’s a rough consensus of a three-month lag from tariff implementation to more notable consumer price increases. That factors in the time taken for shipments, a front-loading of imports that built up inventories and points including importers using the automatic payment transfer system being able to delay their tariff payments for up to 1.5 months.

- On a similar note, the July Beige Book noted that “Contacts that plan to pass along tariff-related costs expect to do so within three months” whilst the August Beige Book, published Sep 3, noted that “Nearly all Districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs.”

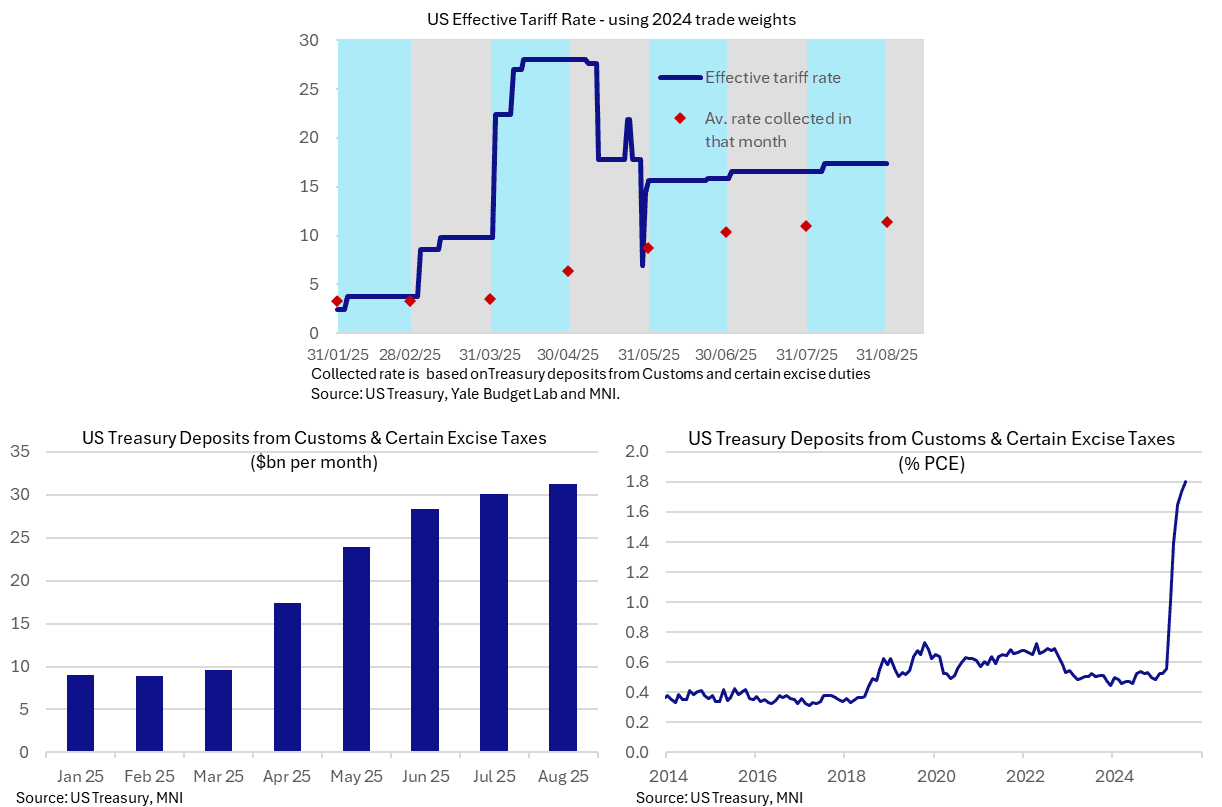

- Latest tariff revenue meanwhile suggests we’re still a little way off seeing the full impact from tariffs on prices. The effective tariff rate currently stands at 17.4% according to Yale Budget Lab calculations (pre-substitution, i.e. keeping trade shares constant) whereas the $31bn of Treasury deposits from customs and certain excise duties in August was worth 11-11.5% of goods imports depending on whether you take 2024 levels for a similar static approach or annualized July data.

- The speed at which the tariff collection rate is increasing has slowed notably in recent months, suggesting it could take a while for this gap to the effective rate to be closed. Indeed, the $31.3bn of tariff revenues is vs $30.1bn in July and $28.4bn in June, after larger increases from $24.0bn in May, $17.4bn in April and $9.6bn in March.

- Alternatively, whilst these tariff revenues are still on the small side compared to what effective rates might suggest, they were still worth a sizeable ~1.8% of overall personal consumption expenditure. That’s an increase of ~1.3pp under the Trump administration so far, but of course doesn’t give insight into burden sharing across importers, businesses and consumers.

US TSYS: Near Post-Auction Highs, Focus on Thu's CPI after Today's Dovish PPI

- Treasuries look to finish near late Thursday session highs after soft PPI data and a strong 10Y Treasury auction re-open, futures back near last Friday highs ahead of tomorrow's headline CPI inflation data.

- After the bell, Dec'25 10Y futures trades +8 at 113-19 vs. 113-20.5 high, initial technical resistance at 113-21+ High Sep 5, followed by 113-26.5 (2.764 proj of the Jul 15 - 22 - 28 price swing).

- The main headline PPI final demand unexpectedly fell by 0.1% M/M (+0.3% expected, with a prior rev to 0.7% from 0.9% prior). The ex-food/energy metric posted identical figures, including the downward revision. This was the lowest for each since April.

- Treasuries climbed higher after the strong $39B 10Y note auction re-open (91282CNT4) stopped through: drawing 4.033% high yield vs. 4.047% WI; 2.65x bid-to-cover vs. 2.35x prior. Dec'25 10Y futures extended highs: 113-20.5, 4.0321% yld, before drawing some fast$ selling.

- Despite the dovish adjustment for US yields in the aftermath of the US PPI report, the impact on the USD index has been more muted, with just a 0.05% move lower on the session.

- Focus turns to Thursday's ECB rate decision/press conference and the key US CPI release: Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded). Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimated of 0.29% to 0.36%.