US: Thune Sends Democrats His 'Final Offer' To End DHS Shutdown

Senate Majority Leader John Thune (R-SD) has sent Democrats the GOP's 'final offer' in compromise ne...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

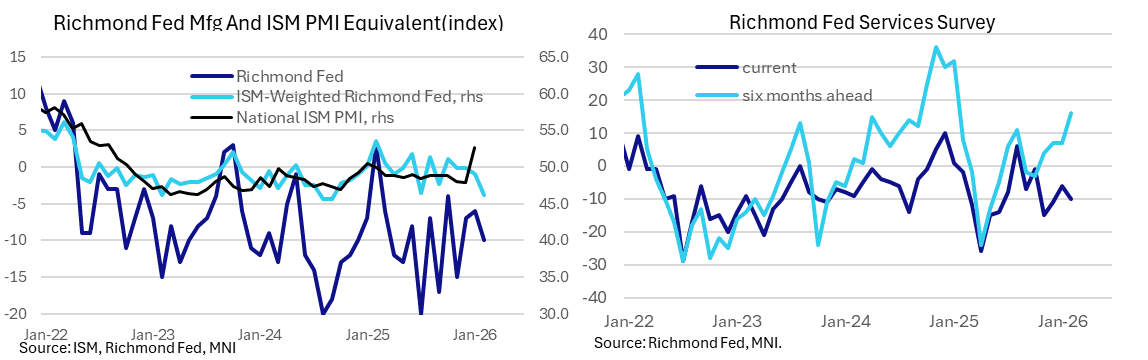

US DATA: Richmond Fed Activity Weak Across Manufacturing And Services (1/2)

The Richmond Fed's Fifth District activity surveys showed deterioration in February vs January, which was particularly acute in the manufacturing report though services were also soft.

- The manufacturing composite index dropped to -10 from -6 (-5 had been expected), with deteriorations in new orders, shipments, and employment.

- By MNI's calculations, the manufacturing subindices reweighted to an ISM equivalent showed a drop to just over 46 from 49 prior, marking the weakest since September 2024. This was in contrast with the NY and Dallas surveys which saw upticks in their ISM manufacturing equivalents in February, though mirrored a decline in Philadelphia.

- There's no ISM equivalent for the regional services survey, but the Richmond Fed's report was weak, with a pullback in the local conditions index to -10 from -6 (-6 had been expected) being identical to that of the manufacturing index, though this was merely a 2-month low. Revenues, demand, and employment all declined.

- The 6-month outlook improved in both cases but this is often the case in months where the current reading is weak, suggesting that firms see improvement from a weaker base of comparison as opposed to delivering a reliable signal of future activity.

- The report doesn't include any anecdotal explanations for the results - the region includes Washington D.C., Maryland, North Carolina, South Carolina, Virginia, and most of West Virginia.

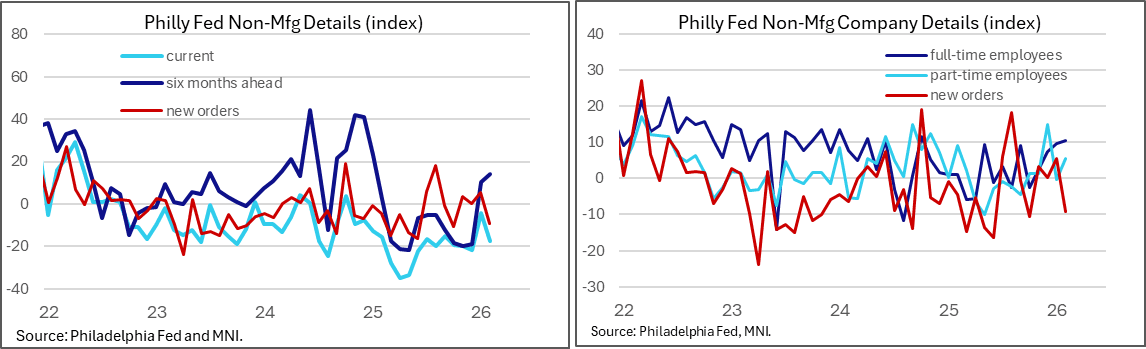

US DATA: Soft Philly Fed Services Activity Comes With Stubborn Price Pressures

The Philadelphia Fed's Nonmanufacturing Business Outlook Survey showed a sharp deterioration in activity in February, with some worrying developments on the inflation front.

- The regional general activity index dropped to -17.3 after a surprisingly high -4.2 in January (which had been a 15-month high). Firm-level activity was also weaker at 5.8 after 16.2.

- New orders fell sharply (-9.3 after 5.5 for the worst reading in 4 months) and sales/revenues dropped 17 points to 8.2, with the key positive development being on the employment front with full-time employees printing a 16-month best 10.6. Additionally, firms expected better activity in six months' time.

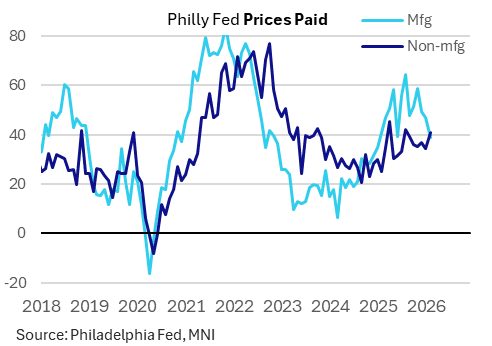

- We took particular note in the sharp rise in price gauges, with paid up to 40.7 for a 6-month high after January's 34.5 marked a 6-month low; prices received rose 9 points to 22 for the highest since May 2023.

- This was the first time the non-manufacturing prices paid gauge exceeded that of manufacturing since October 2024, and corresponded with regional Fed services surveys elsewhere which have shown stubborn prices paid in February (largely in contrast to manufacturing counterparts). The pickup in prices received also suggests services firms are feeling a little more confident in their pricing power.

US TSY FUTURES: Midday March'26-June'26 Roll Update: 2Y Near 75% Complete

Midday Tsy quarterly futures roll volumes from March'26 to June'26 outlined below. Heavy volumes this morning sees most between 60%-65% complete (2s lead at 73%) ahead of Friday's "First Notice" date where the June contract takes lead. Current roll details:

- TUH6/TUM6 appr 1,569,500 from -5.62 to -5.0, -5.12 last; 73% complete

- FVH6/FVM6 appr 2,604,000 from -2.0 to -1.5, -1.5 last; 66% complete

- TYH6/TYM6 appr 2,350,400 from 1.5 to 2.0, 2.0 last; 65% complete

- UXYH6/UXYM6 434,800 from 3.25 to 3.5, 3.5 last; 60% complete

- USH6/USM6 appr 356,000 from 13.0 to 13.75, 13.25 last; 59% complete

- WNH6/WNM6 appr 461,800 from 10.0 to 10.75, 10.0 last; 60% complete

- Reminder, Mar'26 futures don't expire until next month: 10s, 30s and Ultras on March 20, while 2s and 5s expire on March 31.