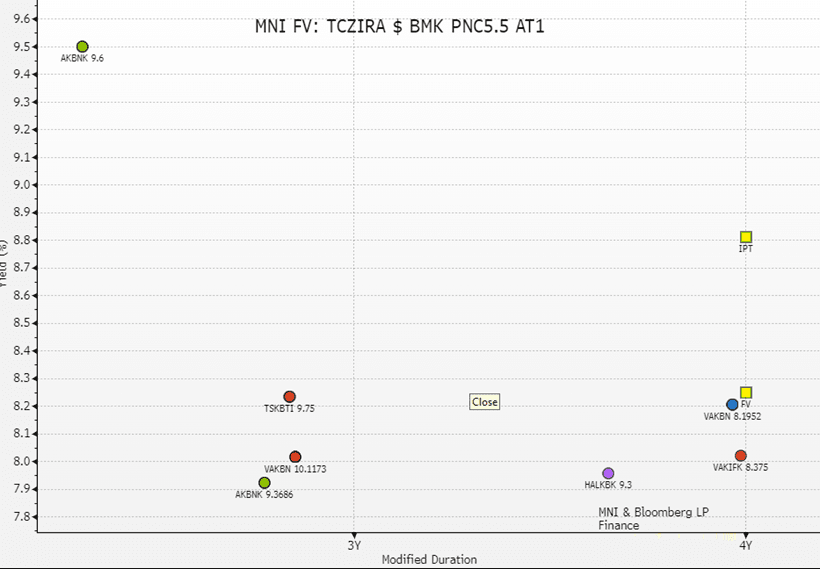

EM CEEMEA CREDIT: T.C. Ziraat Bankasi A.S: $ BMK PNC5.5 AT1

(TCZIRA: Ba3/NR/BB-)

IPT: 8.75%-8.875%

FV: 8.25%

T.C. Ziraat Bankasi issuing a $ BMK PNC 5.5 AT1 bond. We look at the following bonds to assess the FV of the new bonds.

- Vakif Katlim Bankasi (VAKIFK: NR/NR/B+) issued a $ BMK PNC5.5 AT1 sukuk earlier in the month. IPT was 8.875-9% and was priced at 8.375%. The bond is currently around 8.05% yield or z+466b

- Vakifbank (VAKBN: Ba3/-/B+) issued $500mn PNC5.25 AT1 bond in September IPT was 8.5-8.625% and launched at 8.2% and is currently around 8.23% yield or z+485bp.

- AkBank (AKBNK; Ba3/-/BB-) 9.3686% PNCMar29 bond which is yielding 7.93% or z+459bp

- Halk Bank (Ba3/-/B+) 9.3% PNC JUN30 bond which is yielding 7.67% or z+ 430bp

- Turkiye Sinai Kalkinma Bank (TSKBTI; Ba3/-/BB-) 9.75% PNCMar29 bond which is yielding 8.22% or z+488bp.

- We estimate a FV of 8.25% on the new bonds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bears Remain In Control Despite Recovery, BoEspeak Eyed

Gilts have generally looked to cues from wider core global FI markets through early Tuesday trade.

- Gilt futures little changed at ~90.85 with bulls unable to force a test of first resistance at the Sep 24 high (91.28). That leaves bears in technical control, with first support located at the Sep 26 low (90.26).

- Yields essentially flat across the curve, with 2s10s and 5s30s remaining in their steepening trend despite the recent flattening moves.

- BoE-dated OIS still prices less than 5bp of BoE easing through year-end.

- We continue to suggest that the market is underpricing the odds of a cut in Q4, but note that such a move would likely require support from Governor Bailey, as well as Deputy Governor’s Ramsden & Breeden (in addition to dovish dissenters Dhingra & Taylor).

- Ramsden maintained his position as the most dovish MPC member that did not vote for a cut in September via his speech yesterday, with Breeden set to speak today. We will also hear from BoE’s Lombardelli & Mann today.

EGBS: Off Highs, Spreads To Bunds A Little Tighter

Bunds have faded from early session highs after initial technical resistance in futures (128.82-84) went untested and German regional CPI data revealed upside risks to this afternoon’s national data.

- This countered early support stemming from increased U.S. government shutdown risks.

- Slightly firmer-than-expected Italian HICP was then seen, after softer inflation releases from France & Spain within the last 24 hours or so.

- Bund futures last flat at 128.60, bearish technical setup intact, initial support in the 128.29-26 zone.

- German yields are little changed to 1bp higher, curve slightly steeper, with the broader technical steepening theme intact.

- EGB spreads to Bunds are a biased tighter (little changed to ~1bp tighter on the day, Iberians outperform), aided by the German CPI data and the Span noting that it will reduce its net issuance target for the current FY by EUR5bln.

- OATs haven’t reacted to a Les Echos report suggesting that the government is mulling raising the flat tax to as much as 36% from 30%. Such a move could bring in more than EUR1bln in extra revenue, which although welcome, is relatively limited when compared to scale of the wider fiscal issues that France faces.

- Euribor futures are little changed on the day, with ECB-dated OIS steady, pricing around ~9bp of easing through June/July.

- This afternoon’s ECBspeak will come from Lagarde, Nagel & Cipollone.

EQUITY OPTIONS: Commerzbank Longer Dated Put Option

CBK (18/09/26) 24p, bought for 2.05 in 6.25k.