STIR: Tariff Growth Drag/SOFR Curve Shape May Present Euribor Flattening Risks

Markets still lean in favour of one more ECB cut this cycle, but the bar to further easing has been raised since the July decision. With the cutting cycle at or at least close to its end, focus is starting to shift towards 2026, where the growth outlook faces offsetting forces from higher tariffs but also increased fiscal spending.

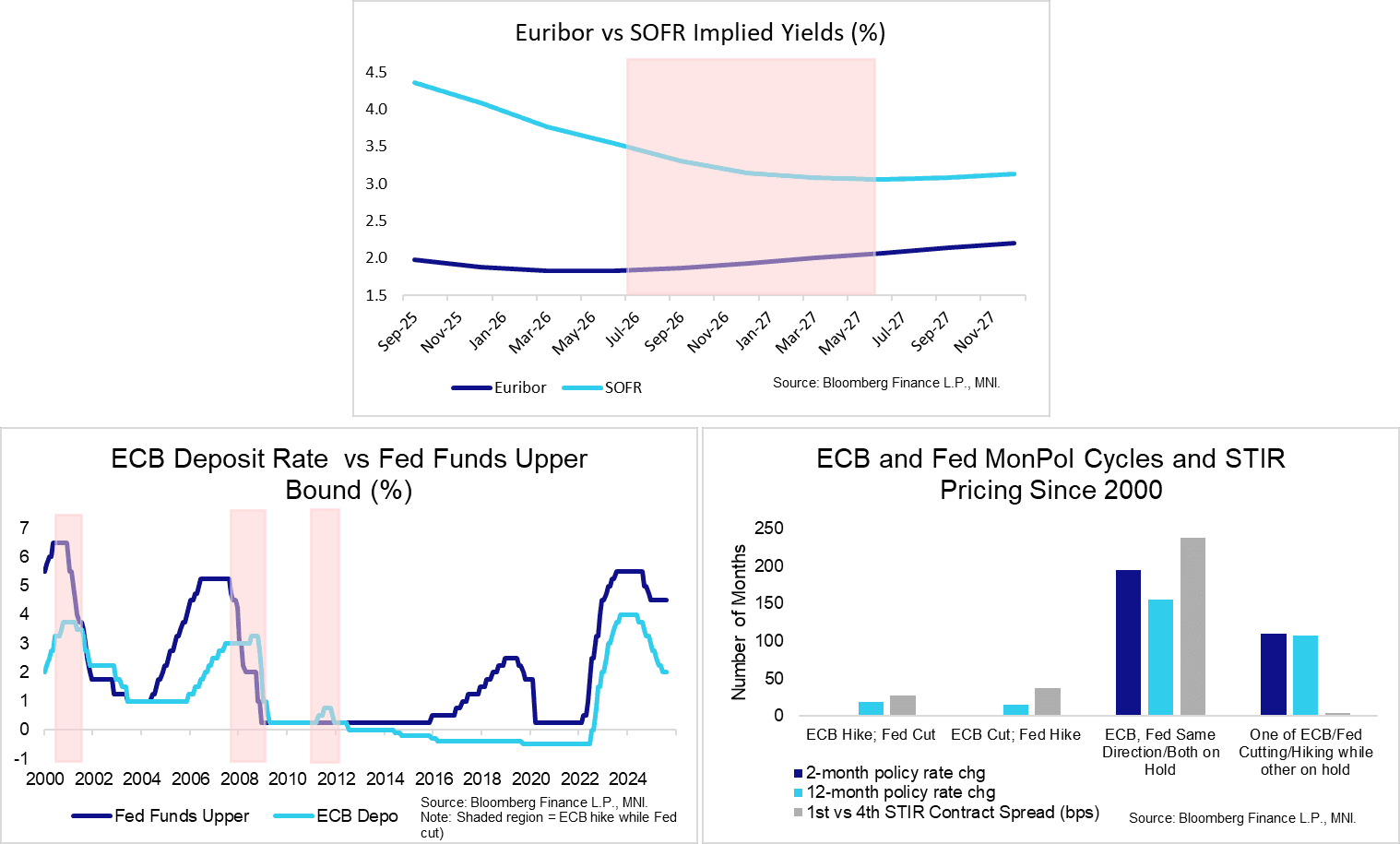

- The anticipated growth impulse from significantly higher EU – especially German – fiscal spending has been reflected in an upward sloping Euribor-implied yield curve from Q2 2026. Euribor futures currently price approximately one full 25bp hike through 2027.

- While the fiscal policy rationale for such a curve shape in 2026/2027 may appear fair in isolation, it’s important to remember that the EU-US trade agreement constitutes a significant increase in the effective tariff rate on EU exports. The MNI Policy Team’s post-July sources piece also noted that the ECB’s hawkish shift is more limited than markets’ reaction would suggest. As such, a tariff-related growth drag may keep policy rates capped in the coming years, presenting flattening risks to the Euribor curve.

- Additionally, the upward Euribor curve shape comes alongside a downward sloping path for SOFR-implied rates.

- As highlighted by the below charts, it is rare to see Fed and ECB policy overtly diverge from one another - particularly the combination of ECB hiking alongside Fed easing. The few instances where the ECB has hiked rates alongside Fed holds/cuts have generally also been temporary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: SOFR Call Condors

Option desks report mixed flow on lighter volumes as US markets return from extended 4th of July holiday weekend. Recent Oct'25 SOFR call condors blocked. Underlying futures mixed, curves steeper with the sdhort end outperforming at the moment. Projected rate cut pricing largely steady vs last Thursday (*) levels: Jul'25 at -1.2bp, Sep'25 at -18.9bp (-19.1bp), Oct'25 at -34.7bp (-34.2bp), Dec'25 at -53bp (-51.8bp).

- SOFR Options:

- Block/screen 8,000 SFRV5 96.06/96.18/96.31/96.43 call condors, 3.25

- 1,850 SFRU5 95.87 put vs. 95.93/96.12 call spd ref 95.88

- Block, 5,000 SFRV5 96.12/96.18/96.31/96.43 broken call condors, 0.0

- 2,000 SFRH6 96.50/97.00 call spds ref 96.43

- 2,100 SFRN5 95.75/95.81/95.87 put trees

- 3,336 SFRZ5 95.75/95.87/96.25/96.37 put condors ref 96.18

- Treasury Options:

- 2,000 TYV5 122.5 calls, ref 111-04.5

- 2,400 TUQ5 104.5 calls, 0.5 (exp 7/25)

- 2,000 TYU5 111.5 puts

- -20,000 TYQ5 109.5 puts, 4 ref 111-07

SOFR OPTIONS: BLOCK: Oct'25 SOFR Call condor

- 5,000 SFRV5 96.12/96.18/96.31/96.43 broken call condors, 0.0 net ref 96.18 at 0634:55ET

US TSYS: Back From Holiday, Bonds Under Pressure, Midweek FOMC Minutes

- Treasuries looking mixed as US markets resume after extended 4th of July holiday, curves steeper with 10s to Bonds weaker vs mildly higher 2s-5s at the moment (2s10s curve +2.023 at 47.984, 5s30s +2.475 at 94.849), Tsy 10Y yield +.0079 at 4.3537% (4.3201 Low / 4.3556 High).

- At the moment, Sep'25 10Y contract trades -2 at 111-05 - recent overnight low, above key technical support at 110-31, the 50-day EMA, and the Jul 3 low. A clear break of this average would signal scope for a deeper correction and highlight a possible reversal.

- For bulls, a resumption of gains would open 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Initial resistance is at 111-28, the Jul 3 high.

- No economic data or Fed speakers scheduled today, US Treasury will be auctioning $82B 13W & $73B 26W bills at 1130ET.

- Relatively light data calendar compared to last week, focus is on the release of FOMC minutes for the June 18 meeting this Wednesday at 1400ET.