ASIA STOCKS: Taiwan Stocks Surge On TSMC, US-Taiwan Trade Deal, China Softer

Asia Pac equities are mixed, with Japan and China/HK markets struggling. Tech led plays in terms of Taiwan and South Korea are outperforming, aided by TSMC's strong results from yesterday, along with the US-Taiwan trade deal announcement. US Equity futures are drifting higher, but remain within recent ranges. Eminis were last near 7000, while Nasdaq futures were up a little over 0.30%.

- Japan markets look to remain in consolidation mode after the earlier surge in the week amid speculation of an early election (we should find out more on this at the start of next week). The NKY was last just under 54k. Today has also seen a strong yen backdrop, amid a fresh FX intervention warning from the FinMin. Offshore investors continue to purchase local equities per weekly flow data.

- In China, BBG reported the authorities were clamping down on high frequency traders. This follows the earlier move this week around increasing margin requirements. Via BBG: "Some of the exchange‑traded funds heavily owned by China’s so‑called national team saw record outflows." The CSI 300 was up earlier today, but now sits down modestly, with near term resistance still evident above 4800. The HSI in HK is off around 0.30%.

- Taiwan's Taiex has risen to fresh record highs. We were last around +1.8%, putting the index above 31300. TSMC's bumper profit result late yesterday, particularly in terms of the capex and sales outlook for 2026, is aiding broader chip/AI related sentiment. The Kospi continues to rally, up a further 0.60%.

- In South East Asia most markets are higher except for the Philippines and Malaysia. Gains elsewhere are less than 0.50% at this stage though. Offshore investors have been net buyers of Indonesian and Malaysia stocks so far this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

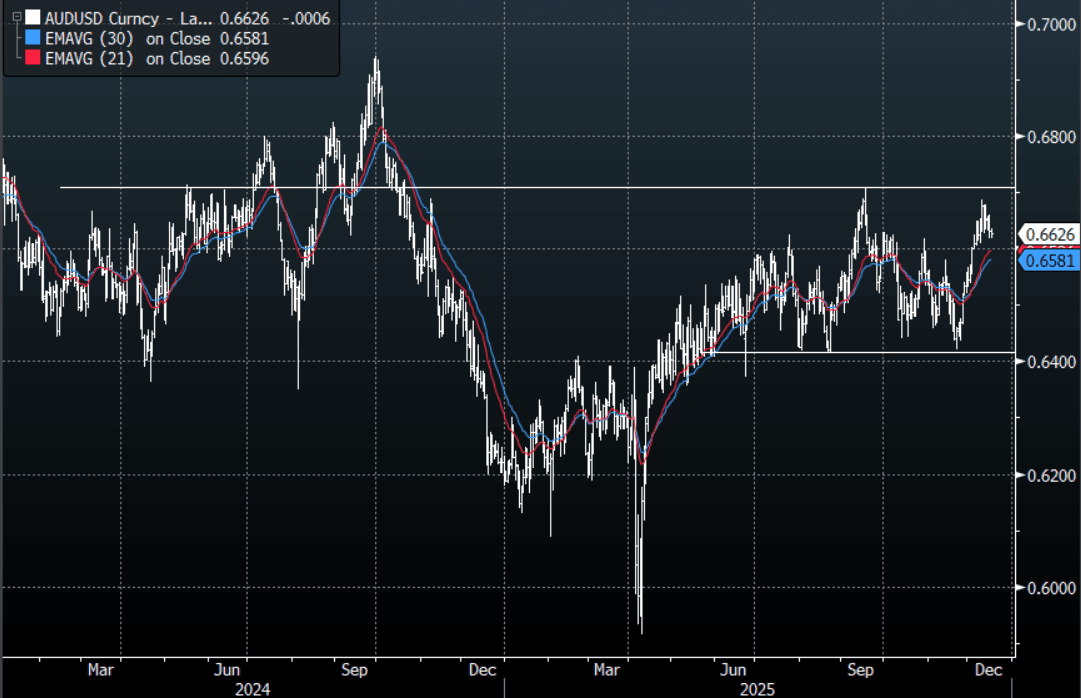

AUD: AUD/USD - Consolidating Above 0.6600-0.6630

The AUD/USD has had a range today of 0.6619 - 0.6635 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD slipped lower as risk took a turn for the worst in Asia on the US blockade of Venezuela, risk has since pared back those losses but the USD has remained bid for now. The AUD price action remains constructive and while the AUD remains above 0.6500-0.6550 I suspect dips could continue to be supported. On the day, while the 0.6600-0.6630 area continues to provide support I would probably be skewed long looking for a move back toward the 0.6660-80 resistance. If this support area does not hold it could signal a deeper pullback toward the 0.6550 area.

- "AUSTRALIA NOV. WESTPAC LEADING INDEX FALLS 0.04% M/M" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6590(AUD680m), 0.6700(AUD655m). Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD1.1b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Bond Futures Steady as Equities Rebound

- As equities rebound after two days of losses, bond futures are steady this morning moving only marginally higher.

- The China 10-Yr future is up +0.06 at 107.96 as it nears the 20-day EMA of 107.99.

- The 2-Yr future is up +0.01 at 102.42, atop the 20-day EMA of 102.42. Were it to break below, downside resistance is via the 50-day EMA of 102.40.

- Cash is steady with the 10-Yr at 1.84%, down -0.5bps this morning and the 2-Yr at 1.39%

JGBS: Futures Holding Weaker At Lunchtime Break, JGB Yields Steady

At the lunchtime break, JGB futures are holding negative, 133.29, -.14 versus settlement levels. Recent lows at 133.18 remain intact, while upticks continue to be faded, with a negative technical bias in play. US bond futures have failed to kick on from the overnight lead in and are down modestly during the morning session in Asia, which may be spilling over to JGBs at the margin.

- JGB yields are little changed in the first part of Thursday dealings. The 10yr was last near 1.97%, up a touch but short of recent cycle highs (close to 1.98%). The 2yr is around 1.07%, as Friday's BoJ meeting outcome comes into focus.

- The market is fully priced for a hike. Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as "1-2.5%," signalling that policy normalisation is likely to continue gradually rather than end at 1%. See our preview here:

- Earlier data was firmer on the export side and core machine orders, but isn't likely to shift BoJ thinking around the economic backdrop.