PHP: Surprise Rate Cut Puts Peso On Defensive

Spot USD/PHP has rallied in reaction to the surprise rate cut delivered by the Philippine central bank and the subsequent rhetoric, with the peso slipping to the bottom five of all 151 currencies tracked by Bloomberg. The pair last deals +0.318 at 58.275 and bulls look for a clearance of Sep 26 high of 58.415 before taking aim at Aug 1 high of 58.563.

- Bangko Sentral ng Pilipinas left its 2025 inflation forecast at +1.7% Y/Y, but revised the outlook for 2026 and 2027 substantially lower, to +3.1% and +2.8% from +3.3% and +3.4%, respectively. It repeatedly stressed that GDP growth may be slowed than anticipated earlier.

- Governor Remolona said that there is now more 'wiggle room' on interest-rate cuts and one more cut is possible before the year-end. He said that the BSP would defend the peso if its depreciation proves sharp, to the extent that it would become inflationary, but would rather not impose capital controls.

- The central bank said that widespread protests over alleged corruption surrounding flood-control projects have dented business confidence, undermining the economic growth outlook. The scandal has had significant political implications, prompting some high-profile resignations - which President Marcos said would not terminate ongoing probes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

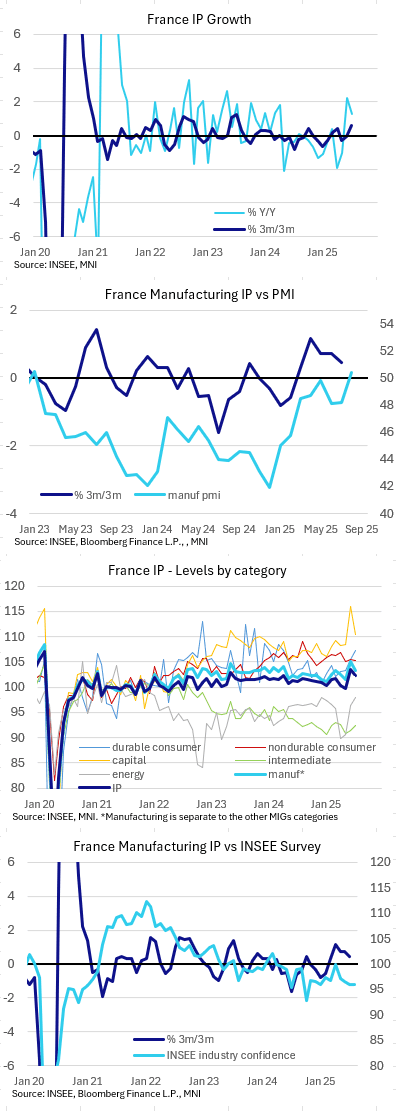

FRANCE DATA: July IP Higher Than Cons Due to Energy / Water; Manufacturing Soft

July France industrial production was stronger than expected, at -1.1% M/M (-1.4% consensus). This followed the strong June (3.7%, revised from 3.8%). However, it appears as though it is energy and water / sewerage driving the upside surprise here with manufacturing softer-than-expected.

- Underlying manufacturing was weaker than the headline print this time, at -1.6% M/M, the lowest sequential reading since May 2024. On a 3m/3m comparison, the sector remains up, at 1.5% (2.6% prior).

- Capital goods production was the mover behind manufacturing, at -4.8% M/M following the very strong +7.0% from June. In July, production fell "in the manufacture of transport equipment (-10.7%) after jumping in June (+16.3%). The decline in this sector was mainly due to the decline in aeronautical and space construction, following a peak in production in June", Insee comments. However, this category in index terms was still the second highest it has been post-Covid, so there could be further pull back next month.

- Durable consumer goods meanwhile were strong again in July, posting their fourth consecutive increase in production, at 1.7% M/M (2.1% prior). Non-durable consumer goods were -0.2% M/M (0.3% prior), while intermediate consumer goods came in at 1.0% M/M (0.6% prior).

- Outside of manufacturing "electricity, gas, steam and air-conditioning supply" rose 1.8%M/M after 5.0%M/M last month (almost matching the high since 2022 in index terms seen in December 2024). Water and sewerage fell 0.9%M/M after the 3.5% rise in June which in index terms is still 2.7% above the Jan-May level. We think that most analysts would have expected further pull back in these categories and these were the main drivers of the upside IP surprise.

- On a yearly comparison, IP was 1.3% (0.7% cons, 2.2% prior, revised from 2.0%).

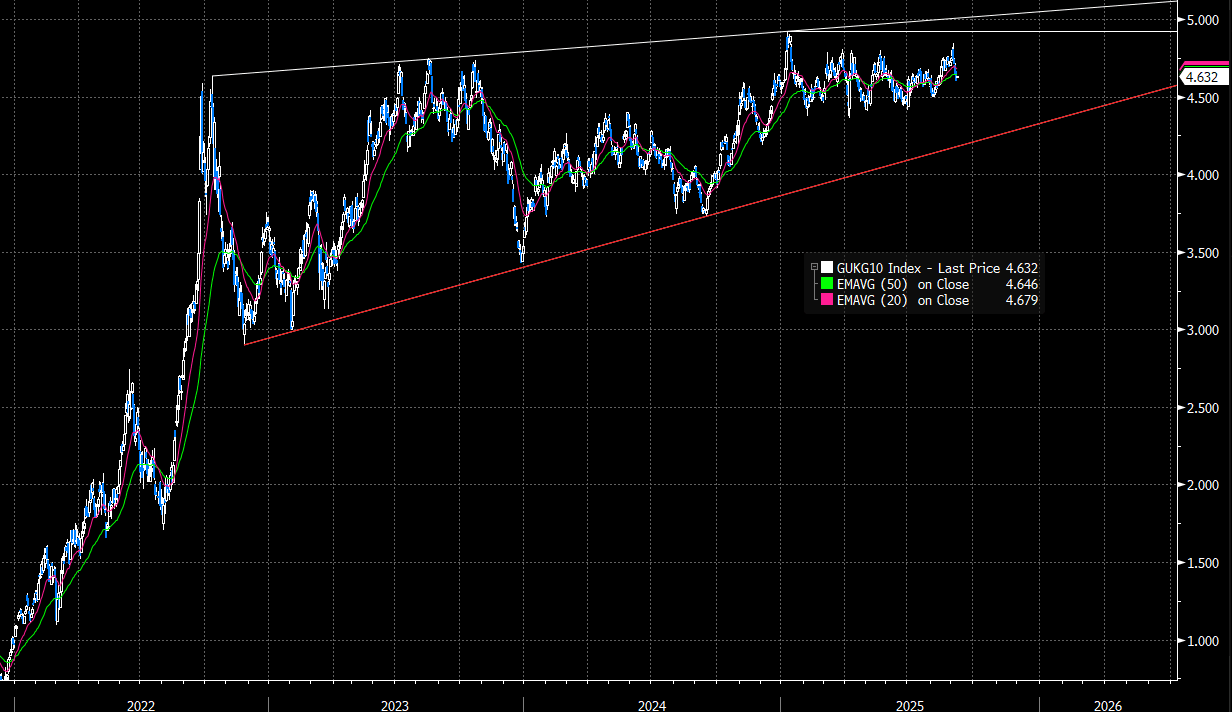

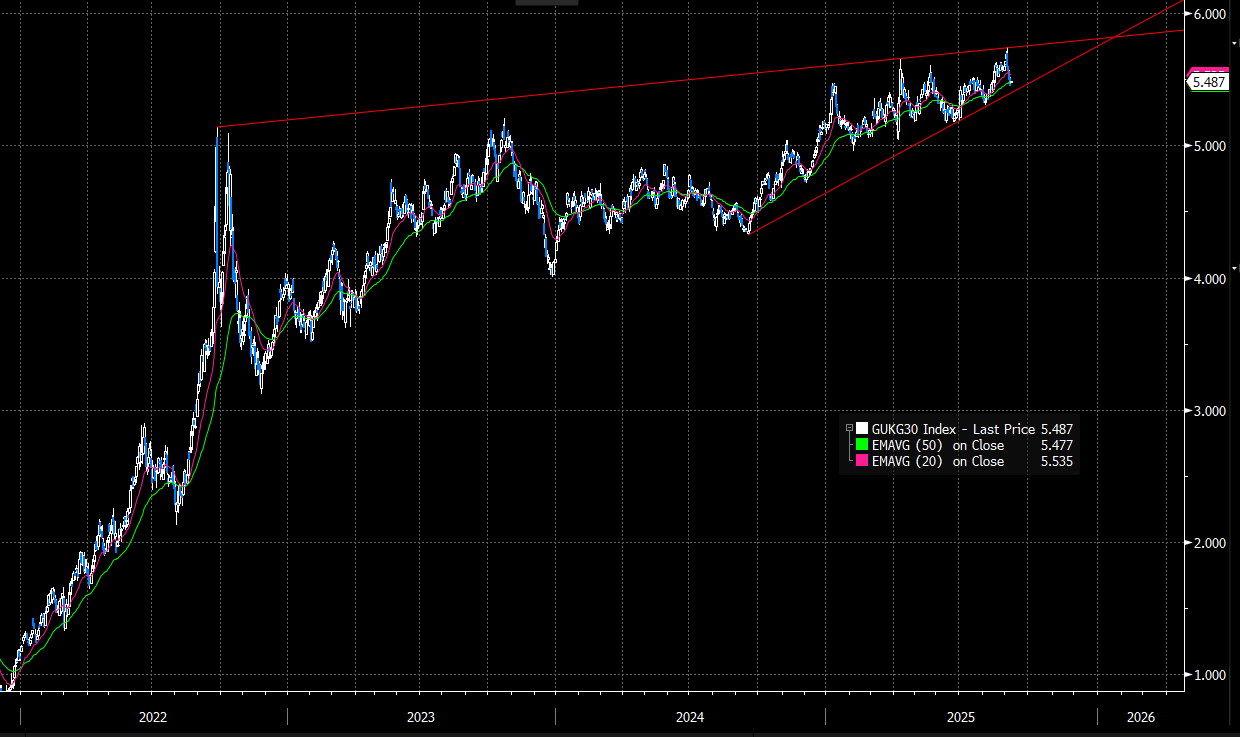

GILTS: Uniform Shift Higher In Curve; Yield Trendline Support Intact For 10s/30s

- The UK curve has seen a fairly uniform shift higher this morning, with yields 2.5-3bps higher across the curve. Gilts underperform Bunds across tenors.

- Although the past four sessions have seen a relief rally in (particularly long-end) Gilts, it’s worth remembering that the technical trend for yields is still to the topside. Both 10s and 30s remain underpinned by trendline support drawn from the September 2024 lows (see charts)

- Gilt futures are -22 ticks at 91.33. However, initial support is not seen till 90.65, the Sep 5 low.

- BRC like-for-like shop sales were 2.9% Y/Y in August, above three analyst estimates ranging from 1.5-2.5%. However, with goods inflation (particularly food inflation) running at a fast pace, sales look a lot less impressive and there may be some boost here from calendar effects.

- The DMO will sell GBP1.75bln of the 4.75% Oct-43 Gilt at 1000BST.

- In our latest Gilt Week Ahead, we look at the recent changes in both UK politics and the potential impacts from the upcoming Labour deputy leader contest. See here

- We will also be focusing on the take up of the STR and ILTR following the gilt redemption; how the market reacts could feed into the MPC's September QT decision.

- SONIA futures are flat to -2.0 ticks through the blues, performing broadly in line with Euribor counterparts. BOE-dated OIS continue to price ~10bps of easing through year-end, with the next full 25bp cut not fully discounted until March.

- Next week’s labour market and inflation data remain vital for the near-term BOE outlook.

Figure 1: 10-year Gilt Yields (Source: Bloomberg Finance L.P)

Figure 2: 30-year Gilt Yields (Source: Bloomberg Finance L.P)

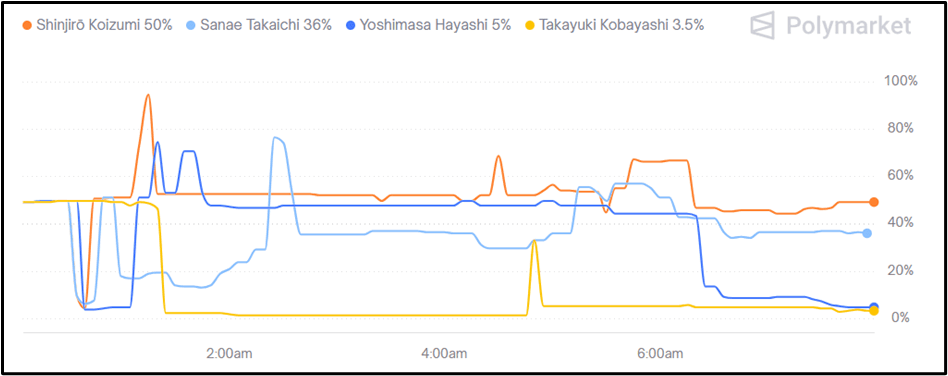

JAPAN: LDP Considering 'Full Spec' Leadership Election On October 4

Japan’s ruling Liberal Democratic Party is considering a ‘full spec’ leadership election on Oct. 4 to elevate a successor to outgoing PM Shigeru Ishiba. The Ishiba government will convene a special parliamentary session to formalise the new government within a few days of the vote.

- Bloomberg notes the election format would give "each of the 295 LDP parliamentary lawmakers one vote each and allocate an equal number of votes to party members. The LDP had 1.03 million members in 2024. That leaves the contenders fighting over 590 ballots."

- Nikkei notes, “If no candidate is able to win a majority, a [FPTP] run-off will be held among the top two candidates... If different candidates are nominated by the two houses, the decision of the lower house prevails.” As the LDP does not control a majority in parliament, there is a remote possibility that a minority coalition could elect a non-LDP candidate via majority vote.

- Polymarket gives pro-reform Agriculture Minister Shinjiro Koizumi a slight edge over conservative Internal Affairs Minister Sanae Takaichi. A third, lower-profile, frontrunning candidate, Chief Cabinet Secretary Yoshimasa Hayashi, receded this morning.

- Nikkei notes that two short-lived PMs have raised concerns of a reversion to 'revolving-door prime ministers', suggesting that political stability will be a key feature of the campaign. An expert told Nikkei that a snap general election in the short term is unlikely, with the new leader likely to hold at least one parliamentary session this autumn before calling an election -- next year at the earliest.

Figure 1: Next Japanese Prime Minister

Source: Polymarket