GBPUSD TECHS: Supports Cleared

* RES 4: 1.3868 High Jan 27 and the bull trigger * RES 3: 1.3814 High Jan 30 * RES 2: 1.3733 High Fe...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Intervention Rumours Reverberate, Officials Fail to Confirm

- The Japanese yen has been the main topic of conversation in currency markets Friday, as a sharp turn lower for USDJPY has prompted mounting speculation that the Ministry of Finance may have intervened. This has all followed the Bank of Japan holding rates unchanged during the APAC session, and while maintaining a hiking bias, Governor Ueda failed to provide any firm details surrounding the tightening timeline.

- Highs of 159.23 overnight were met with a sudden 200-point selloff as Europe logged on, and despite a consolidatory period just above the 158.00 handle, an additional round of selling has seen USDJPY fall as low as 155.90 as we approach the weekend close.

- While today’s price has prompted lots of rumours surrounding official rate checks and potential JPY buying from the BOJ/MOF, we would highlight a couple of characteristics that point to it not being intervention.

- First of all, the initial magnitude and net impact was not as large as previous episodes and the timing so close to the BOJ rate decision would be rare. Additionally, although the USDJPY daily adjustment now stands around -1.5%, the moves have come in tandem with the dollar index extending to the lowest level since early October. As a result, the impact on the likes of AUDJPY and GBPJPY has been very moderate. Furthermore, we would highlight that although a 333pip daily range is impressive, USDJPY did post a 228pip daily range in the opposite direction following a BOJ hike in December, adding to the likelihood this could well be a positional squeeze.

- With all of that said, today’s selloff has seen the pair cross both the 20-day and 50-day EMA, with a weekly close below the latter being closely monitored to signal a deeper correction. Below here, 154.35 represents a reversal trigger, the Dec 5 low.

- Elsewhere, the noted greenback weakness has propelled the likes of AUDUSD to a fresh cycle low just below 0.6900 while GBPUSD has printed above the 1.36 handle for the first time since September. EURUSD is pressuring the 1.18 handle, while firmer inflation data in New Zealand looks to have cemented a 3.25% gain for NZDUSD.

- The softer-dollar narrative comes ahead of next week’s Fed meeting and growing speculation over the next Fed chair announcement.

USDJPY TECHS: Trend Needle Points North

- RES 4: 160.21 2.236 proj of the Dec 5 - 9 - 16 price swing

- RES 3: 160.00 3.000 proj of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 159.60 2.000 proj of the Dec 5 - 9 - 16 price swing

- RES 1: 159.45 Jan 14 cycle high and the bull trigger

- PRICE: 158.11 @ 15:58 GMT Jan 23

- SUP 1: 157.60/156.27 20- and 50-day EMA values

- SUP 2: 154.35 Low Dec 5 and a reversal trigger

- SUP 3: 153.62 Low Nov 14

- SUP 4: 152.82 Low Nov 7

The trend structure in USDJPY remains bullish despite the acute vol through Friday morning. Recent gains resulted in a breach of 157.89, the Nov 20 high, to confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Moving average studies remain in a bull-mode position too, highlighting a dominant uptrend. Sights are on the 160.00 handle next, a Fibonacci projection. Key support to watch is 156.27, the 50-day EMA.

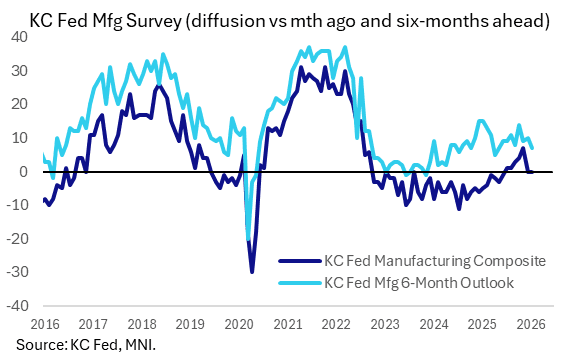

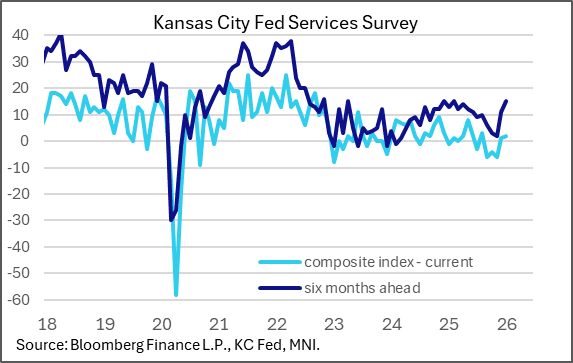

US DATA: Kansas City Fed Surveys Show Little Improvement In January (1/2)

The Kansas City Fed's 10th District regional surveys for January were little changed from December, with Services clearly improving amid renewed stagnation for Manufacturing. Both surveys indicate that average-to-slightly-below-average activity persists though at better levels than seen in the first half of 2025.

- The Manufacturing survey composite saw no change from 0 between December and January, marking the joint-lowest since June. However the Services survey saw a 1 point improvement to 2 from 1 prior, a 5-month high, with 6-month expectations rising 4 points to an 11-month high 15.

- For manufacturing, new orders and employment were unchanged at flat levels, while production expanded and capex decreased. For services, almost all sub-index readings improved vs December, including revenue/sales and wages/benefits, though employment continued to fall.

- Optimism improved in the services survey, but deteriorated for manufacturers.

- These roughly corroborated the S&P Global flash PMIs for January which showed relatively little change in activity across services and manufacturing vs December, but are in contrast to the NY/Philly Fed surveys which showed a solid improvement. We await the Dallas and Richmond Fed readings next week.