CNH: Support Around 6.8600, CNH Outperforms Higher US-CH Yield Spreads

Much like Tuesday's session, USD/CNH ran out of downside momentum around 6.8600 before support emerg...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Sharp Retracement Post Election, But Dip Sub 50-day EMA Supported

USD/JPY tracks near 155.85 in early Tuesday dealings, after the yen rose around 0.85% for Monday's session (around mid point from a G10 standpoint, as broader USD indices fell sharply). Yesterday's early highs at 157.76, followed by subsequent lows at 155.52, has likely done some near term damage to the USD/JPY uptrend. A combination of broader USD weakness, fresh FX jawboning (post the election outcome) and pledges by the Japan government not to boost bond borrowing to fund a tax cut, all worked in yen's favour.

- Still, current levels are fairly close to the 50-day EMA, meaning prices are far from signalling an extension of any downtrend. As such, the medium-term bull cycle remains in play and the pair is holding on to its latest gains. Sights are on 157.72, a Fibonacci retracement point. Clearance of this level would strengthen the bull theme. On the downside note the 100-day EMA is around 154.46.

- Focus will be on whether yen can sustain gains amidst further FX jawboning (and without actual intervention), while broader cross asset trends, like firmer global equities, recovering precious metals, point to yen underperformance against higher beta plays.

- In terms of the BoJ outlook, via our Tokyo based policy team - Takaichi, whose coalition secured a two-thirds supermajority in Sunday’s general election, maintains that decisions on raising borrowing costs rest with the BOJ, despite her strong mandate to tackle the cost-of-living crisis. Market pricing has full hike priced by around June this year, with the March meeting only giving a modest chance to a hike.

- On the data front today we have Jan money stock figures then Jan (preliminary) machine orders data later.

- In the option expiry space, note the following for NY cut later: Y157.00($884mln).

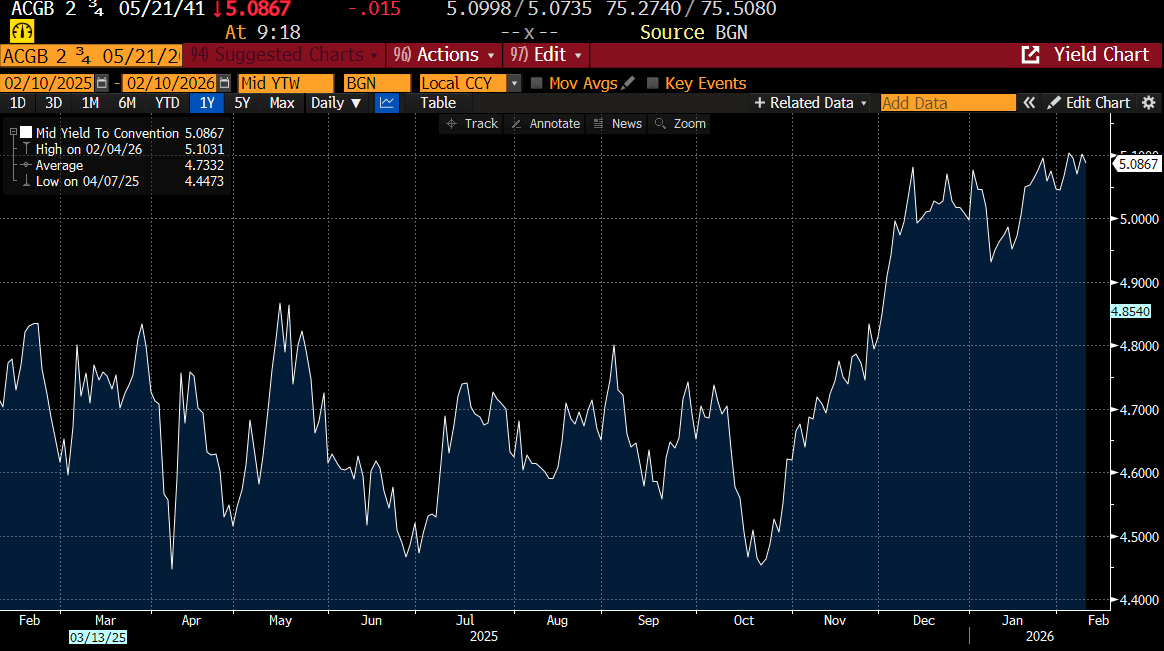

AUSSIE BONDS: Modestly Richer, Confidence Data & May-41 Supply Due

ACGBs (YM +1.5 & XM +1.5) are modestly stronger after a slightly mixed close for US tsys on Monday.

- US NEC Director Hassett posited "you should expect slightly smaller job numbers that are consistent with high GDP growth right now, and that one shouldn't panic if you see a sequence of numbers that are lower than you're used to." explaining that "population growth is going down and productivity growth is skyrocketing.”

- Rate locks and fast$ selling for $20B Alphabet 7pt debt issuance helped keep rates contained on the day.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at +65bps, around its cycle high.

- The bills strip is flat to +2 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 16% for March to 96% by June and 158% by December 2026.

- Today, the local calendar will see Westpac Consumer and NAB Business Confidence measures.

- This week, the AOFM plans to sell A$300mn of the 2.75% 21 May 2041 bond today (see chart), A$700mn of the 3.75% 21 April 2037 bond on Wednesday and A$1000mn of the 2.50% 21 May 2030 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Little Changed After A Slightly Mixed Close For US Tsys

NZGBs are little changed after a slightly mixed close for US tsys on Monday.

- US NEC Director Hassett noted that “there's a pretty big decline in the labor force because of illegals leaving the country. And so the breakeven job number is quite a bit lower than it was under Joe Biden."

- Focus in the US now turns to weekly ADP NER pulse employment numbers, Import/Export Prices, several Fed speakers and a $58B Tsy 3Y note sale.

- Via BBG: "ANZ 2025/26 Farmgate Milk Price Revised Up to NZ$9.50/KgMS", it adds: "Although global dairy supply and demand factors haven't meaningfully improved, dairy prices have rebounded strongly so far in 2026." This follows the recent surge in dairy price auctions, which is supporting the NZ terms of trade backdrop.

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while December 2026 assigns 44bps.

- Today, the local calendar will be empty. The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.