AUSTRALIA: Supply/Demand Imbalance Driving Housing Affordability Deterioration

The Australian housing market continues to look robust driven by strong demand and lacklustre new supply. Depressed housing affordability is currently not weighing on the market with the number of new first time home buyer loans rising 10.8% y/y. The RBA doesn’t seem concerned and has not mentioned the risks from positive wealth effects and dropped dwelling investment from the May statement. When easing starts, it is likely to have limited impact on housing affordability given current imbalances.

- The RBA revised down dwelling investment projections to -3.2% y/y for Q2 2024 but Q4 was higher at +0.2% y/y for Q4. 2025 and 2026 were revised down.

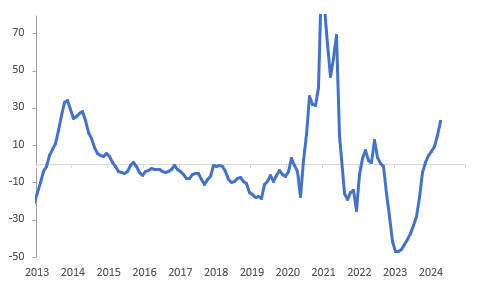

- May CoreLogic house prices rose 0.8% m/m to be up 9% y/y and 24% above trend. They are now 13.8% above the January 2023 trough. The smaller capitals are seeing stronger rises due to “extremely low levels of available supply”, according to CoreLogic.

- Strong demand is also reflected in the rental market with vacancy rates very low and Q1 rents rising 7.8% y/y. It is also seen in strong sales growth, which was 39.3% y/y in April across the 5 states.

Source: MNI - Market News/Refinitiv

- On the supply side, Q1 real dwelling investment fell 0.5% q/q, second consecutive quarterly fall, to be down 3.4% y/y. Building approval data is not signalling the needed recovery with the number of April approvals 19% below pre-pandemic levels and up only 3.5% y/y.

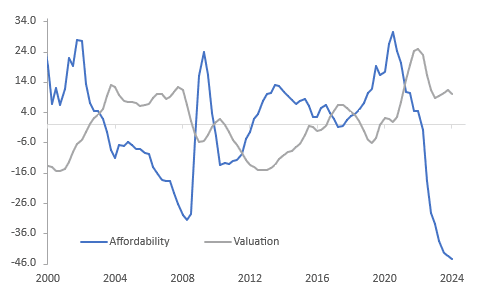

- As a result, housing is now around 10% overvalued based on the house price-to-rents ratio and affordability (HAI) is its worst since our series began in 1980. Higher mortgage rates have contributed to deteriorating affordability but they have been stable over 2024 and Q1 nominal disposable income rose 1.1% q/q, yet there has been a 2pp deterioration in our HAI since Q4 reflecting higher home prices.

Source: MNI - Market News/Refinitiv

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNY Fixing Error Close To Unchanged

The USD/CNY fix printed at 7.1016, versus a Bloomberg consensus of 7.2159.

- Today's fixing error was -1146pips in USD/CNY terms, so little changed versus yesterday's outcome. The actual fix crept further above 7.1000 but remains within recent ranges.

- USD/CNH is drifting higher in the first part of trade, in line with broader USD gains, albeit with a lower beta to such moves. We were last around 7.2280, not yet able to breach the 7.2300 handle.

US TSY FLOWS: US TSY FUTURES: BLOCK, 10Y Likely Seller

- -3,000 TYM4 108-31, post time at 10:56:04 AEST, DV01 $190,000. Contract trades 108-31+ last vs. 109-03 high

JGBS: Off Earlier Highs As Tsys Tick Lower, Ueda Watching FX Moves

There has been little net directional change in JGB futures in the first part of Wednesday dealings. JBM4 was last at 144.78, +.10. This is at the bottom end of today's ranges, but recall early lows yesterday came in at 144.54.

- US Tsy futures sit off earlier highs, which may be driving some downside momentum in JGBs, albeit at the margin.

- BoJ Governor has been before parliament fielding questions. FX is clearly a strong local focus point at the moment. The Governor noted monetary policy can't control FX, but that currency shifts could have a big impact on the economy and thereby drive a policy shift.

- The Governor added they will adjust policy as appropriate if inflation trends towards 2% (as they currently project), or if inflation is at risk of overshooting.

- In the cash JGB space, yields are all lower. 10-30yr tenors are off by 1-2bps. Falls are less prominent at the short end.

- Coming up later we have the 10yr debt auction.