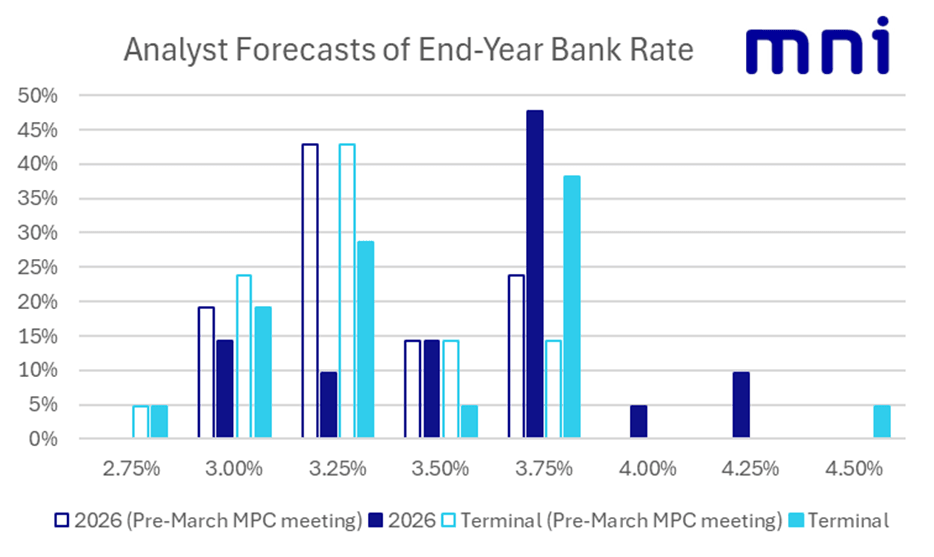

BOE: Summary of Analyst Views

- Just over half (11/21) of the analyst reviews that we have read still look for the next move from the MPC to be a cut. 4/21 look for a hike while 6/21 look for the Bank to remain on hold for their forecast horizon.

- In terms of those expecting hikes Daiwa, JP Morgan and Rabobank all look for the first hike in April with the former two looking for a 4.25% peak and Rabobank looking for a one-and-done. NatWest Markets look for the first hike in Q4-26 but then expect two further hikes in Spring 2027 to the highest peak of 4.50% seen in any analyst base case that we have seen.

- Note that of these analysts, 3/4 (all except NatWest Markets) expect cuts back to a least current levels within their forecast horizon.

- In terms of those looking for the next move to be a cut, none look for a move in April with 5 analysts expecting a June cut, 1 for July, 2 for November and the remaining 3 looking for cuts to begin in 2027.

- UniCredit has the lowest terminal rate, continuing to look for 2.75% while 4/21 analysts look for 3.00% terminal, 6/21 analysts look for 3.25% and 1/21 analyst looks for 3.50%. As noted above, NatWest Markets looks for hikes with no reversal but the remaining 8/21 analysts look for no moves from 3.75% throughout the forecast horizon.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: FOMC Keeping Rate Hike Door Open

- Treasuries dipped - extended lows slightly after the January FOMC minutes release showed most voting members cautioned "disinflation could be slower than expected", while keeping open the possibility that the next Fed rate move could be a hike.

- Currently, TYH6 trades -6 at 112-30 vs. 112-28 low, Initial firm support to watch is 112-09+, the 50-day EMA.

- Mar'26/Jun'26 quarterly Tsy futures roll has accelerated ahead of the Feb 27 first notice date, 5Y leading the move with over 760,000 spreads in late trade.

- Prior to the minutes release, $16B 20Y Bond auction tailed - contributing to weaker Tsys in second half trade: the sale drew a high yield of 4.664% vs 4.644% WI at the cutoff; 2.36x bid-to-cover (lowest since Nov 2024)vs. 2.86x prior. Peripheral stats: indirect take-up falls to 55.17% (lowest since Feb 2021) vs. 64.71% prior.

- Look ahead: Australian employment data highlights Thursday’s calendar, before US jobless claims and Philly fed data. Focus will swiftly turn to Friday’s docket, where European PMIs and US GDP & PCE headline.

- Earning expected after the close: Coeur Mining, CF Industries, Texas Pacific Land, Edison Int, DoorDash, Occidental Petroleum, Carvana, eBay and Blue Owl Capital.

US TSYS: Late SOFR/Treasury Option Roundup: More Two-Way

Decent two-way SOFR/Treasury option volumes Wednesday, less one-way compared to yesterday's heavy call buying all openers: +140k SFRZ6 98.00 calls, +45k SFRU 98.00 calls, and appr 140k midcurve calls, call spds targeting Jun'27, Sep'27 and Dec'27. Underlying futures weaker, low end narrow range, current projected rate cut pricing consolidating vs. late Tuesday (*): Mar'26 at -1.5bp (-2.1bp), Apr'26 at -5.6bp (-6.6bp), Jun'26 at -19bp (-19.4bp), Jul'26 at -28.6bp (-29.1bp).

- SOFR Options:

- -5,000 0QZ6 98.00/98.50 call spds 3.0

- +6,000 0QM6 96.37 puts, 2.0 vs. 96.91/0.10%

- +5,000 SFRZ6 98.00 calls, 6.5 vs. 96.895/0.14%

- +4,000 SFRZ6 97.25/98.00 1x2 call spds, 1.5 ref 96.90

- +5,000 SFRK6 96.75/96.81 call spds, 0.75 ref 96.55

- -5,000 0QH6 97.00 calls, 6.0

- -18,000 SFRZ6 96.50/96.75 put spds, 10 ref 96.90

- -2,000 SFRZ6 96.87 calls, 25.5 ref 96.91/0.52%

- +12,000 SFRM6 96.56 puts, 11.25 ref 96.55

- +15,000 SFRZ6 98.00 calls, 6.75 vs. 96.905/0.14%

- -20,000 SFRM6 97.25 calls 2.0 vs. 96.54 to -.55/0.10%

- +4,000 0QM6 96.43 puts, 2.0

- -25,000 SFRZ6 97.25/97.75/98.00 broken call trees, 0.75-0.5

- over 5,600 0QH6 96.75 puts, ref 96.95

- 5,000 SFRH6 96.31 puts

- 4,500 SFRH6 96.43 calls ref 96.355

- 1,000 SFRJ6 96.43/96.50/96.56 put flys ref 96.545

- 1,000 0QJ6 96.56/96.68/96.81 2x3x1 put flys ref 96.955

- Treasury Options:

- -5,000 TYM6 113 straddles, 203 vsd. 112-31.5/0.04%

- over 26,000 TYJ6 113.5 calls

- +30,000 TYH6 113.5 calls, 3 ref 112-30.5 (total volume over 60k)

- 5,000 TYJ6 115 calls, 9 ref 112-29

- 13,000 TYK6 110.5/TYM6 110 put calendar spds ref 112-30

- 1,500 USK6 102 puts, 1 ref 117-11

- over 11,300 TYH6 113 calls, 10-12 ref 112-31.5 to 113-01.5

- over 6,700 today's 10Y 113 puts, 5 ref 113-00.5

- over 7,500 today's 10Y 112.75 puts, 1 ref 113-01

- 3,800 TYH6 113.5 calls, 5 ref 113-03 to -03.5

- 2,000 FVH6 110.75 calls, .5 ref 109-19.75

US: Trump To Deliver Remarks At Black History Month Event Shortly

US President Donald Trump is shortly due to deliver remarks at a White House event to mark Black History Month. The remarks are Trump's first public address since last Friday and may offer the first opportunity for reporters to ask questions of the president live on air since February 12. LIVESTREAM

- The event comes amid a significant uncertainty that nuclear talks with Iran can avert direct military conflict. Tension has built throughout the day, with increased speculation that Trump may order large-scale strikes on Iran in the coming days. See: SECURITY: Probability Of US Strike On Iran Spikes Amid Surge Of Military Assets

- If Trump takes questions, he is also likely to be grilled on the status of trilateral Ukraine talks, which wrapped up today without any apparent progress toward a ceasefire agreement.