US LABOR MARKET: Strong Payrolls Report, But Supply Vs Demand Debate To Go On

Apr-03 14:59

March's BLS employment report was undoubtedly strong in the main readings, and will have allayed con...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

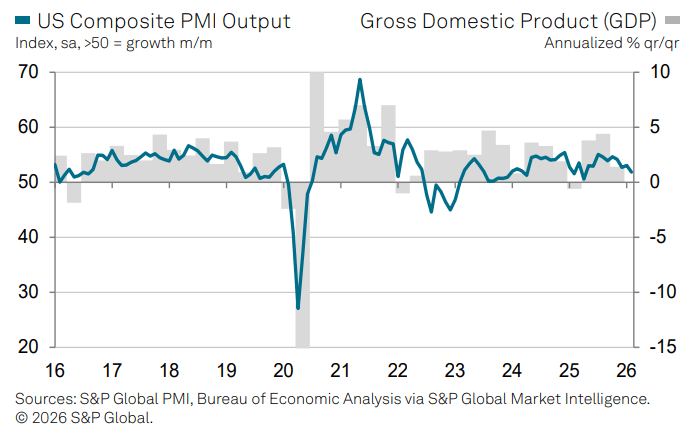

US DATA: Final PMIs Point To Cool Growth In Q1 So Far

Mar-04 14:55

February's final reading of S&P Global flash PMIs brought some slight downgrades from the flash release, including both Services at 51.7 (52.3 flash, 52.7 prior) and Composite at 51.9 (52.3 flash, 53.0 prior).

- That confirmed the weakest Services reading since April 2025 (which coincided with the US Liberation Day tariff announcements), though this series has recently diverged from the ISM Services gauge which has been accelerating in recent months. Recall that S&P Manufacturing PMI fell in February to the lowest since July 2025 (51.6 final vs 52.4 prior).

- The Composite reading implies real GDP growth of just under 1.5% Q/Q annualized, per the report, which would be steady from 1.4% in Q4 (which was considered understated largely due to government shutdown-related factors).

- A few highlights from the Services release (link):

- "muted demand conditions limited hiring activity and kept business confidence below trend"

- "Selling price inflation accelerated on the month, reflecting elevated cost pressures from tariffs and rising employee expenses"

- "New order growth extended into a twenty-second successive month but also cooled from January"

- Backlogs rose to the "greatest extent since May 2022"

- Of interest ahead of February nonfarm payrolls: "February data signaling a second successive monthly increase in headcounts. However, growth was largely associated with filling existing vacancies, and the gain in employment was only fractional amid reports that cost-cutting efforts had constrained hiring activity."

GILTS: Recoveries Capped, 2-Year Yields Still 20bp Higher On The Week

Mar-04 14:54

Pushback from Iran against suggestions that the country’s intelligence service had indirectly reached out to the CIA to “discuss terms for an end to the conflict” provide some demand for energy futures in recent trade, with modest weight applied to core global FI markets

- Recoveries from yesterday’s lows in gilts remains limited when compared to the scale of the week-to-date sell off.

- Futures have failed to break above the 20-day EMA (92.41), leaving yesterday’s high unchallenged. Contract last +48 at 91.95.

- Meanwhile, 2-Year yields are still 20bp higher on the week.

EQUITY OPTIONS: Estoxx Put Fly buyer

Mar-04 14:51

SX5E (20th Mar) 5350/4800/4300p fly, bought for 11 in 10k.