ASIA STOCKS: Strong Inflows Continue for India

May-01 02:08

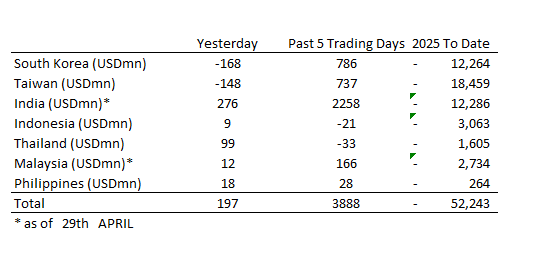

Strong inflows continue with India topping US$2bn of inflows over the last five days.

- South Korea: Recorded outflows of -$168m as of yesterday, bringing the 5-day total to +$786m. 2025 to date flows are -$12,264m. The 5-day average is +$157m, the 20-day average is -$300m and the 100-day average of -$138m.

- Taiwan: Had outflows of -$148m as of yesterday, with total inflows of +$737m over the past 5 days. YTD flows are negative at -$18,459. The 5-day average is +$147m, the 20-day average of -$8m and the 100-day average of -$198m.

- India: Had inflows of +$276m as of the 29th, with total inflows of +$2,258m over the past 5 days. YTD flows are negative -$12,286m. The 5-day average is +$452m, the 20-day average of +$87m and the 100-day average of -$121m.

- Indonesia: Had inflows of +$9m as of yesterday, with total outflows of -$21m over the prior five days. YTD flows are negative -$3,063m. The 5-day average is -$4m, the 20-day average -$52m and the 100-day average -$37m

- Thailand: Recorded inflows of +$99m as of yesterday, outflows totaling -$33m over the past 5 days. YTD flows are negative at -$1,605m. The 5-day average is -$7m, the 20-day average of -$24m the 100-day average of -$19m.

- Malaysia: Recorded inflows of +$12m as of the 29th, totaling +$166m over the past 5 days. YTD flows are negative at -$2,734m. The 5-day average is +$33m, the 20-day average of -$25m and the 100-day average of -$35m.

- Philippines: Saw inflows of +$18m as of yesterday, with net inflows of +$28m over the past 5 days. YTD flows are negative at -$264m. The 5-day average is +$6m, the 20-day average of -$2m the 100-day average of -$4m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Little Changed Ahead Of RBA Policy Decision

Apr-01 02:06

ACGBs (YM flat & XM +0.5) are little changed after today’s data and before the RBA policy decision.

- February retail sales were slightly weaker than expected rising 0.2% m/m after 0.3% with annual growth moderating 0.2pp to 3.6%. Looking through volatility from seasonal discounting, retail spending is in line with rates seen since October but 3-month momentum has slowed. The pickup in consumer confidence from lower inflation & rates should support the upward trend in retail spending going forward.

- The RBA decision is announced at 1430 AEDT today followed by Governor Bullock's press conference at 1530 AEDT. The bank is widely expected to leave rates at 4.10% after cutting 25bp at the last meeting (see MNI RBA Preview here).

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest gains.

- Cash ACGBs are 1bp richer to 3bps cheaper with the AU-US 10-year yield differential at +20bps.

- Swap rates are 1bp lower.

- The bills strip is +1 to +2 across contracts.

CROSS ASSET: Watching Credit Spreads

Apr-01 02:02

US financial conditions are tightening, with most of President Trump's Agenda being bad for growth, outside of deregulation. These policies have the potential to have a bigger impact on asset prices than is being expected.

- Goldman’s has worryingly cut its S&P target for a second time this month and now expects the Index to end the year around 5700.

- Credit spreads which have been relatively well behaved to start the year are now starting to pay attention as the probabilities of stagflation increase.

- HY spreads are approaching the 400 level which in the past if broken has seen periods of extreme volatility and risk aversion.

- An acceleration through here would be a very bad sign for stocks and an indication of much lower levels from here.

- Foreign investors have accumulated huge amounts of US equities since 2010. We have already seen the start of a rotation back to Europe in particular, but this has the potential to gather in pace.

Fig 1: Credit Spreads - High Yield

Source: MNI - Market News/Bloomberg

MNI: CHINA MAR CAIXIN MANUFACTURING PMI 51.2 VS 50.8 IN FEB

Apr-01 01:47

- CHINA MAR CAIXIN MANUFACTURING PMI 51.2 VS 50.8 IN FEB