OIL: SPR Release Has Reverse Effect as Brent Through $100

- Oil prices surged dramatically on Thursday during the Asia trading day, with Brent back above the psychologically significant $100 per barrel mark.

- Th rally occurred despite a historic announcement from the International Energy Agency (IEA) to release 400 million barrels of emergency reserves—the largest in the organisation's history which analysis now shows is insufficient to offset the supply lost thus far.

- Focus remains on the Straits of Hormuz as reports suggests oil tankers have been bombed. Oman’s key oil export terminal was evacuated and two crude tankers were hit in Iraqi waters, as risks to global energy supply from the Middle East war deepened. This as reports that of a 70% collapse in Iraqi production further tightened supply expectations.

- According to Australian Treasury analysis, if oil averages $US100 per barrel for three months, headline inflation could rise by 0.5 percentage points. If it averages $US120, inflation could jump by a full 1.0 percentage point.

- A sustained shock could lead to "stagflation"—a period of high inflation coupled with stagnant economic growth.

- WTI is up +8.55% today at US$94.71 bbl

- Brent is up +9.1% at US$100.44 bbl.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: USTs Take Lead from JGBs, Yields Below Mid Point of 1M Range

USTs have followed the lead of JGBs in thin markets with gains Tuesday ahead of the NFP. Yields are down 1-2bps across the curve with curve movement limited. Bond futures' moves are muted with the 10-Yr up +02 at 112-08.

- The 2-Yr is down -1.2bps at 3.477%

- The 5-Yr is down -1.4bps at 3.732%

- The 10-Yr is down -1.6bps at 4.188%

- The 30-Yr is down -1.9bps at 4.841%

Ahead of the NFP markets get the ADP employment change (prior 7.750k), import / export price index (useful guide for future inflation expectations) and retail sales.

There is a US$90bn 6-week bill auction and a US$58bn 3-Yr bond auction tonight as key focus. Bid to cover on last 3-Yr auction was 2.65x

US yields have shown sensitivity to jobs data of late, making this week's NFP an increasingly important release for the next catalyst for yields.

FOREX: A$ Backs Away From 0.7100 Test, BBDXY Struggles Amidst Yen Gains

The main focus in the G10 space has been a further retracement in USD/JPY, although higher beta FX has given some of the recent gains seen. AUD and NZD are both down 0.25-0.30%. Some retracement in the precious metals rally has likely been a headwind for both currencies. Gold is down around 0.65%, while silver is off a little over 2.5%. AUD/USD has stopped short of a test above 0.7100, with an option expiry at this figure level for NY cut later as well. AUD/USD was last 0.7070/75, NZD/USD in the 0.6035/40 region. The BBDXY index did try to rally in first part of trade but once USD/JPY rolled over it struggled. We were last 1182.6 for the index, little changed for the session (earlier highs were at 1184.46).

- On the data front, the main focus has been on Australian survey measures with both the Westpac consumer sentiment and NAB business surveys released. Consumer sentiment fell, although Westpac noted the response was more muted compared to earlier rate hikes. NAB business conditions eased, but have largely trended sideways since the middle of last year.

- Both measures point to some downside risks to growth momentum, but the RBA arguably needs this help bring inflation back into the target band.

- US equity futures are a touch softer, while US yields are drifting lower (which has likely help cap USD upside). AUD/JPY is back under 110.00, but still above all key EMAs.

- There have been little shifts elsewhere, outside of some weakness in NOK and SEK. EUR/USD has hovered just above 1.1900, while GBP/USD remains sub 1.3700, which capped upside late in Monday trade.

- Looking ahead, US retail sales data headlines Tuesday’s calendar, while markets will then swiftly turn their focus to US employment (Wed) and US CPI (Fri).

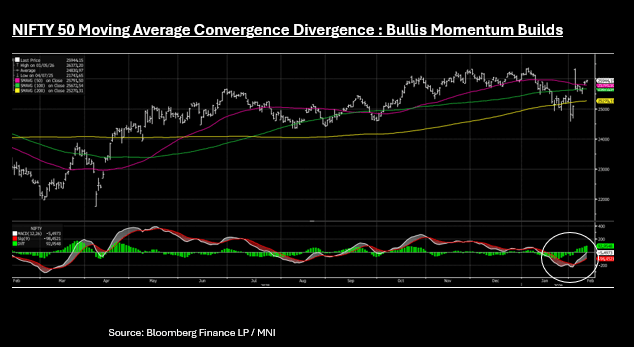

ASIA STOCKS: Japan Effect Sees Regional Gains, NIFTY 50 Strong Uptrend Building

- Stocks in Japan continue to lead today following the election result and optimism over the economy. Investors are pricing in the PMs "Sanaenomics" agenda, which includes a ¥21 trillion stimulus package, potential tax relief (suspending the 8% sales tax on food), and increased defense and AI spending. The ongoing earnings season has exceeded expectations. Heavyweights like SoftBank Group saw shares spike over 10% today after upgrading full-year forecasts. Other major gainers include Furukawa Electric (+22%) and NEC, which announced a significant share buyback. This momentum is supported by structural reforms that have raised Japan's average Return on Equity expectations significantly. This sees the NKY up +2.3% today and nearly 7% in the last three trading days.

- The Japan effect lifted regional bourses with all major indexes up . China was more subdued to modest gains as markets start to wind down ahead of the upcoming holidays and the KOSPI rose by just +0.10%.

- Despite news that FTSE Russell are following the lead by MSCI, the Jakarta Composite brushed off these further concerns with a second day of gains, up +1.1% today.

- India's NIFTY 50 is +0.30% and continues to deliver solid daily gains. Since the announcement of the US trade deal, the NIFTY 50 has gained almost 5% to be near 26,000 again. The bullish momentum is strong for the NIFTY 50 according to the MACD analysis. The short term exponential average is significantly longer than the long term suggesting a strong uptrend is building for the index.