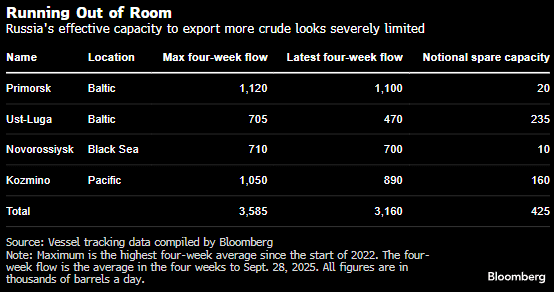

OIL: Spare Capacity at Russia’s Crude Export Terminals May be Limited

Russia’s ability to divert crude to the global market is diminishing as crude export capacity has fallen after recent refinery attacks, according to Bloomberg.

- Drone strikes on Russian refineries and diversion of crude to export terminals may have contributed to a recent increase in shipments.

- Ukraine has targeted at least 15 refineries across the European part of Russia since the start of August.

- Spare capacity at Russia’s crude export terminals may be very limited. Three western ports have about 165kb/d to 265kb/d of spare capacity between them.

- Primorsk and Novorossiysk are now close to their upper limits and shipping near the largest number of barrels on a four-week basis in 18 months.

- Ust-Luga has nominal capacity to increase exports but shipments have been well below a peak all year possibly following repeated attacks on feed pipeline pumping stations. Based on peak shipments Ust-Luga should have about 235kb/d of spare capacity but is around 130kb/d based on this year.

- Other ports are less likely to be useful for crude diverted from damaged refineries or are not connected to the Russia’s pipeline system.

Source: Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

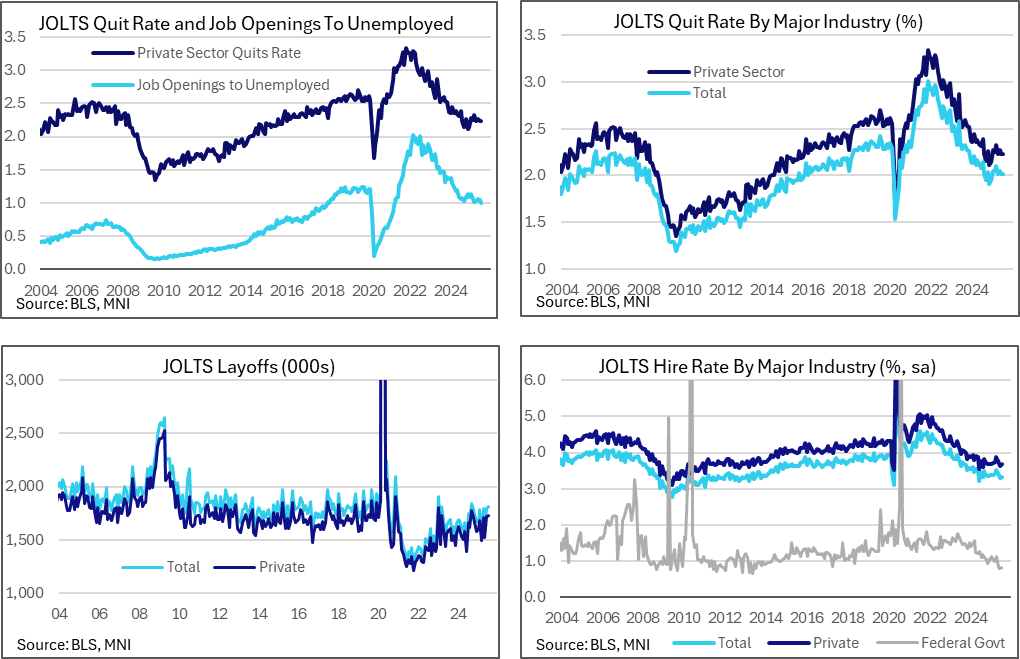

US DATA: A Soft JOLTS Report As Vacancy To Unemployed Tilts Lower

The JOLTS report for July was softer than expected, primarily on the openings front as the ratio of vacancies to unemployed fell to a new recent low. Powell at Jackson Hole had pointed to this metric in the category of little changed to only modestly softer over the past year, leaving sensitivity to any subsequent declines here.

- Job openings were lower than expected at 7181k (sa, cons 7380k) in July after downward revised 7357k (initial 7437k) in June.

- Combined with the already known sizeable rise in unemployment from last month’s payrolls report and the ratio of openings to unemployed fell to 0.99 from 1.05 (initial 1.06).

- That’s the lowest ratio since Apr 2021 having kept to a fairly tight range around an average 1.07 since mid-2024. That said it’s still not wildly different to the 1.02 and 1.03 seen in Mar-April.

- The quit rate was little changed at 2.01% after an upward revised 2.01 (initial 1.97) in June, having averaged 2.0% since Aug 2024.

- These quit rates remain low historically compared to pre-pandemic figures of 2.3% through 2019 and 2.2% through 2017-18, but see a steady trend rather than a further softening. Indeed, they remain above late last year’s recent lows of 1.9%.

- Hire rates meanwhile ticked up marginally to 3.33% from an upward revised 3.30% (initial 3.26), although that does little to reverse a pullback from a recent high of 3.52% in April.

- Layoffs were higher than expected as they increased to 1808k (cons 1675k) from an upward revised 1796k (initial 1604k) although we caution that the consensus comes from only three responses. Nevertheless, that’s still the highest since Sep 2024 and continues a broad uptrend back more clearly to pre-pandemic levels.

- Recall Powell from Jackson Hole (Aug 22): “The unemployment rate, while edging up in July, stands at a historically low level of 4.2 percent and has been broadly stable over the past year. Other indicators of labor market conditions are also little changed or have softened only modestly, including quits, layoffs, the ratio of vacancies to unemployment, and nominal wage growth.”

- Today’s report for July marks a further modest softening in the ratio of vacancies to unemployment although the quits rate has continued to stabilize.

GILTS: Futures Close Tuesday's Gap Lower

Gilt futures close yesterday’s opening gap lower in the wake of the soft U.S. JOLTS jobs data.

- Bulls now look to August 28 & 29 highs (90.84). a break there would start to counter the bearish technical impetus in the contract.

- Yields 3-9bp lower, as the flattening move extends in the wake of the data.

US TSY OPTIONS: Oct'25 2Y Call Buyer Spree

Paper started buying Oct'25 2Y calls overnight - continue to add to positions as underlying futures extend highs post-JOLTS data:

- over 19,300 TUV5 104.5 calls, 6.5 last

- over 38,000 TUV5 104.62 calls, 5.5 last

- over 50,000 TUV5 104.75 calls, 4.5 last