ITALY: S&P Affirm Italy at BBB, Outlook Stable

Oct-20 20:07

- *S&P: ITALY 'BBB/A-2' RATINGS AFFIRMED; OUTLOOK STABLE (BBG)

- The following commentary was attached to the report:

- "By 2025, S&P project that Italy's real GDP growth will recover to above 1%, helped by accelerated deployment of the Next Generation EU funds, which we believe will likely extend beyond 2026"

- "Economic growth will decelerate in 2023 and 2024 on the back of rising private sector savings, tightening credit conditions, slowing manufacturing, and weakening global trade: S&P"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Quantifying The Impact Of Student Loan Repayment Restart

Sep-22 18:15

- The more than three-year moratorium on federal student loans comes to an end at the end of next week, with payments resuming on Oct 1.

- It will impact the 29 million recipients of student loans currently in forbearance, amounting to $1.1tn as of June 30, 2023 (https://studentaid.gov/data-center/student/portfolio)

- The Fed notes that the average interest payment in 2019 was between $200-$299 per month (covering about 70% of adults with student loans). If all borrowers in forbearance were to restart payments in line with these past ranges, it would be the equivalent of $5.9B to $8.8B per month ($71-106B per year). That scales to an annualized 0.35-0.5% of disposable income or 0.4-0.55% of nominal spending as of the July personal income report.

- On the subject, MS have previously written that the new income-driven payment plan, SAVE, can lower the average federal loan payment closer to $200/month in July 2024. The impact to consumer spending in 4Q23 is mitigated somewhat by the 12-month grace period implemented by the Biden Administration. Assuming 50% of borrowers will begin making some payment in 4Q23, a 70% pass-through to consumer spending would result in a 0.8pp drag to real PCE growth in 4Q23, followed by a 0.3pp drag to 1Q24 consumption.

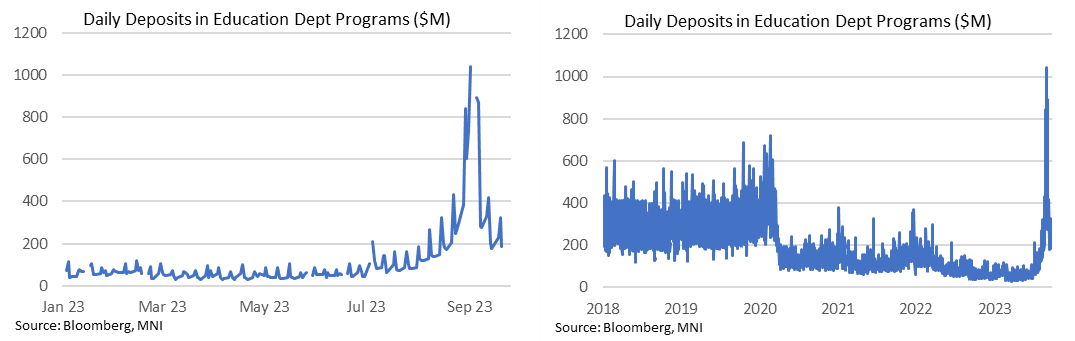

- Some of this Q4 impact might however have been brought forward into Q3, with a surprise jump higher in the daily deposits seen at the Department of Education marking a likely indicator of early repayments. They started to build in earnest in August before peaking with a historically high increase of $1.04B on Sep 1.

- It has meant

daily deposits summing to $13.9B in Q3 to date, up from $3.4B through Q2.

STIR: BLOCK, Mar'24 SOFR Ratio Put Spread

Sep-20 19:55

- Total 20,000 SFRH4 93.75/94.5 2x1 put spds at 11.5 ref 94.56 at1542:50ET

AUDUSD TECHS: Key Short-Term Resistance Remains Intact

Sep-20 19:55

- RES 4: 0.6630 High Aug 2

- RES 3: 0.6616 High Aug 16

- RES 2: 0.6522 High Aug 30 and Sep 1, and the key resistance

- RES 1: 0.6511 50-day EMA and High Sep 20

- PRICE: 0.6447 @ 20:51 BST Sep 20

- SUP 1: 0.6357 Low Sep 6 and the bear trigger

- SUP 2: 0.6287 2.00 proj of the Jun 16 - Jun 29 - Jul 13 price swing

- SUP 3: 0.6272 Low Nov 3 2022 and a key support

- SUP 4: 0.6215 2.236 proj of the Jun 16 - Jun 29 - Jul 13 price swing

The AUDUSD trend condition is unchanged and the trend outlook remains bearish. Key support and the bear trigger at 0.6365, the Aug 17 low, has recently been pierced. A clear break of this level would confirm a resumption of the downtrend and open 0.6272, the Nov 3 2022 low. Key short-term resistance has been defined at 0.6522, the Aug 30 and Sep 1 high. A break would signal likely short-term trend reversal.