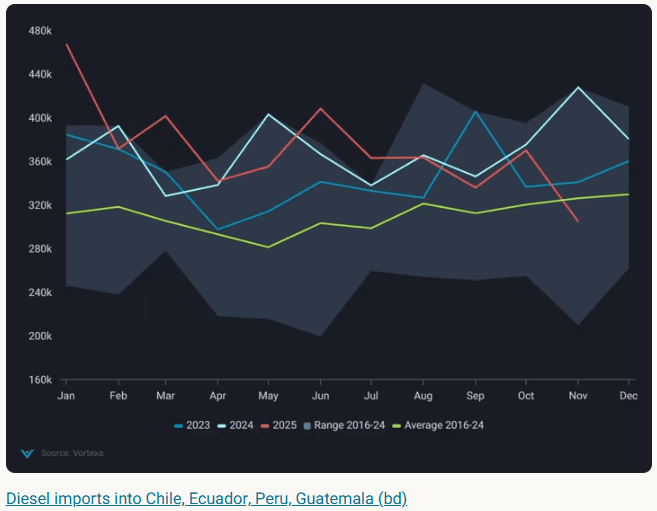

DIESEL: South American Diesel Demand to Support Refiners on US Gulf Coast

Nov-21 10:31

Growing South American diesel demand is likely to support PADD 3 refiners for the medium term, despite diverging trends for South America West Coast and East Coast clean product arrivals, Vortexa said.

- South America West Coast’s top four clean product importers, Chile, Peru, Ecuador, Guatemala, show a multi-year high diesel import program. Arrivals averaged over 30% above the seasonal average for the first six months of 2025 before descending from July-November.

- A typical seasonal increase in demand for power generation could provide support towards the end of the year.

- Rising temperatures have increased cooling demand during the summer in Chile, as diesel usage has progressively shifted from the mining industry in recent decades and droughts have impacted hydro output.

- Diesel demand will continue to add pressure to the Atlantic Basin diesel balance, with nearly 70% of flows into Chile, Peru, Ecuador and Guatemala from US Gulf Coast refiners.

Source: Vortexa

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

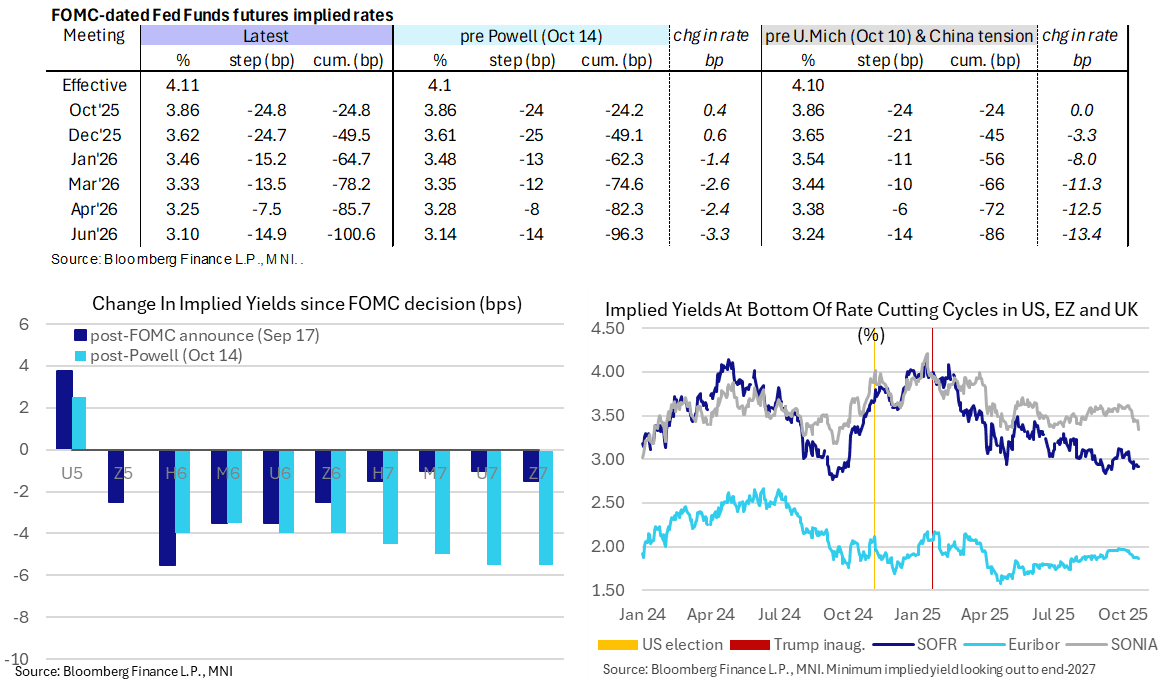

STIR: Back-to-Back Fed 25bp Cuts Still Eyed, Only Mild Impact From Soft UK CPI

Oct-22 10:27

- Fed Funds implied rates are little changed overnight, with back-to-back cuts seen for next week and December meetings before a quarterly pace thereafter to mid-2026.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49.5bp Dec, 64.5bp Jan, 78bp Mar, 85.5bp Apr and 100.5bp Jun.

- SOFR futures are little changed on the day, with only small intraday spillover from a sizeable rally in UK rates on softer than expected UK CPI inflation.

- The SOFR implied terminal yield of 2.915% (SFRH7) is unchanged on the day, close to last week’s lowest close of 2.89% in risk-off moves on regional bank fears. For context, cycle lows were 2.77% back in Sep 2024 in anticipation of an aggressive start to the Fed’s easing cycle at the time.

- It’s a particularly thin data docket today, with just MBA mortgage applications. More notable releases for the week are state-level jobless claims to be released from Thursday afternoon and then the highlight being the delayed September CPI report on Friday.

LOOK AHEAD: Wednesday Data Calendar: 20Y Bond Re-Open

Oct-22 10:26

- US Data/Speaker Calendar (prior, estimate)

- 10/22 0700 MBA Mortgage Applications (-1.8%, --)

- 10/22 1130 US Tsy $69B 17W bill auction

- 10/22 1300 US Tsy $13B 20Y Bond re-open (91210UN6)

- 10/22 1600 Pres Trump meets w/ Secretary General of NATO (closed Press)

- Source: Bloomberg Finance L.P. / MNI

US 10YR FUTURE TECHS: (Z5) Bull Cycle Intact

Oct-22 10:26

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-24 @ 11:15 BST Oct 22

- SUP 1: 113-03+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-22 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

Bullish conditions in Treasuries remain intact. The recent breach of key resistance at 113-29, the Sep 11 high, confirms a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 11303+, the 20-day EMA.