EM CEEMEA CREDIT: SOIAZ: green bond in USD on local mkt

Jan-10 09:48

"*AZERI SOCAR TO ISSUE $200M OF GREEN BONDS ON LOCAL MARKET" - BBG

UoP: clean energy projects

Tenor 5Y

CPN: 6%

Source: BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: No Real Spill Over From JGBs, Uptick In Oil Weighs

Dec-11 09:48

Little in the way of spill over into wider core global FI markets when it comes to the latest BoJ sources piece from BBG.

- Fresh session highs in crude oil futures help push Bund & TY futures back towards session lows.

JGBS: Quick Two-Way Flow On BBG BoJ Sources Piece That Ultimately Leans Dovish

Dec-11 09:36

Price action in JGB futures similar to what was seen in XXX/JPY FX pairs following the BBG source report.

- JGB futures initially sold off on the headline noting that "some BoJ officials not against rate hike in Dec", before recovering on the headline stating that the "BoJ is said to see little cost to waiting for next hike.”

- JBH5 based at 142.14, before a rally through Tokyo highs, peaking at 142.39 thus far.

- While the article suggested that officials vow it as “only a matter of time” until the next BoJ hike is delivered, the dovish references within it (and dovish title of the piece) seem to outweigh any hawkish snippets.

- A reminder that our Tokyo policy team had already flagged their understanding that “the potential political reaction to rate hikes is making senior Bank of Japan officials tend towards normalising policy more slowly, despite data showing it is moving towards achieving its inflation target”…“The Bank’s concerns over politics, and also over how markets might react to higher rates, means that an increase to the 0.25% policy rate at the Dec 18-19 meeting will be unlikely unless the yen weakens to JPY160 against the dollar.”

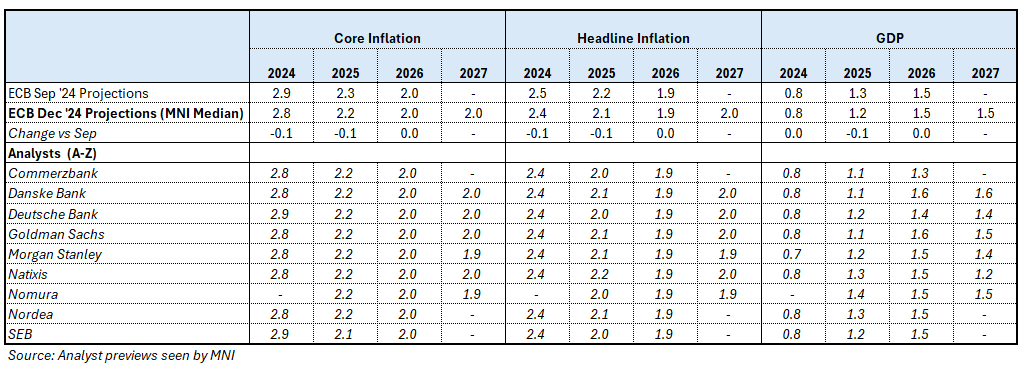

ECB: Analysts Expect Small Downward Revisions To Headline, Core and GDP F'casts

Dec-11 09:23

Analysts expect the ECB to make small downward revisions to its inflation and GDP projections in the December projection round, which has been compiled by Eurosystem (i.e. national central bank) staff. Note that 2027 projections will also be presented for the first time.

- Based on the previews MNI has seen, the median expectation for 2025 core inflation is 2.2% (vs 2.3% in the September projection round). The core inflation projection is expected to be 2.0% in 2026 and 2027. Morgan Stanley and Nomura see the 2027 core inflation projection at 1.9%.

- The 2025 headline inflation projection is expected at 2.1% (vs 2.2% in September).

- Although crude oil futures were around 6% lower around the December projection cut-off date compared to September, analysts note that this is offset by higher gas/electricity prices and a weaker Euro.

- Q3 GDP exceeded ECB forecasts at 0.4% Q/Q (vs 0.2% projected), but this was in part due to temporary effects from the Paris Olympics. Weak momentum into Q4, alongside heightened uncertainty from US trade policy and French/German politics means analysts expect a downward revision to the ECB’s 2025 real GDP forecast to 1.2% (vs 1.3% in September). 2027 real GDP projection expectations range from 1.2% (Natixis) to 1.6% (Danske).

- See the table below for a full summary. MNI’s ECB preview is here.

Related bullets

Related by topic

SOIAZ

Azerbaijan

EU Credit Energy

Credit Sector