AUSSIE BONDS: Softer Futures, But Sep Highs Still Close, RBA's Hunter Speaks

Early Wednesday trade has Aussie bond futures down modestly, although we are still holding onto the bulk of recent gains seen this week. 3yr futures were last 96.50 (+2.5bps), while 10yr were at 95.73 (+2bps ). For 3yr recent Sep highs remain intact at 96.615, while for the 10yr the upside focus point is 95.78. Clearance of these levels would reinstate a bullish theme.

- Focus is on US-China tensions, which softened as Tuesday's session unfolded, with the USTR stating trade talks are on-going. Recall yesterday, risk off gripped markets as China announced shipping curbs/investigation.

- Whilst tomorrow the Sep Jobs data prints. We do hear from the RBA's Hunter later this morning, but the central bank is in data watch mode at this stage and still painting a cautious outlook (in terms of further cuts). A full 25bps cut is not priced in until Feb/Mar next year.

- ACGB cash yields sit around 2bps firmer across the benchmarks in the first part of Wednesday trade. The 3yr back to 3.48%, after finding support near 3.45%.

- The 3/10s curve is +77bps, slightly flatter. The AU-US 10yr spread has stabilized ahead of +20bps.

- Note today we also get the Westpac Leading index for Sep, while we also have a 2035 bond sale.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Bounces on NFP

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.805/960 - High Aug 8 / High Apr 7

- PRICE: 95.735 @ 15:48 BST Sep 12

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.720 - 1.0% 10-dma envelope

Aussie 10-yr futures remain above their recent lows, aided by Treasury strength on the weak NFP number and into this week’s Fed decision. To the upside, the next resistance is at 96.207, a Fibonacci retracement point. Initial near-term resistance is seen at 95.805, the Aug 4 high. A break of this hurdle would be a bullish development. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

NEW ZEALAND: Q2 GDP Released This Week & Forecast To Contract 0.3% q/q

The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- BNZ August performance of services is released Monday. It rose 1.3 points to 48.9 in July but has printed below the breakeven-50 level since November 2023.

- August monthly price series including food, electricity, rent, petrol and travel print on Tuesday. Food price inflation has been picking up. There is a risk that Q3 CPI inflation exceeds the 3% top of the RBNZ’s target band. The bank is forecasting 3% for the quarter.

- On Wednesday, Q3 current account data is out and the deficit is expected to narrow to 4.8% of GDP but with it widening to $2.7bn from $2.32bn in Q2.

- There is also Westpac Q3 consumer confidence on Wednesday.

- August trade data are published on Friday. The improvement in the deficit stalled around mid-year.

US TSYS: Yields Retrace Higher Friday Night, Led By The Long-End

TYZ5 reopens at 113-05, down 0-04 from closing levels in today’s Asia-Pac session.

- Friday night the US 10-year yield had a range of 4.0280% - 4.0816%, closing around 4.64%.

- Treasury yields retraced higher on Friday; the long-end led the move(2s10s +3.17 at 50.452, 5s30s -1.11 at 104.534).

- MNI US DATA: U Mich Consumer Sentiment Slips With High Likelihood Of Job Losses. Sentiment surprised lower in the report, at 55.4(cons 58) after 58.2 in Aug.

- MNI US DATA: Little Reaction To Stronger Preliminary U Mich 5-10Y Inflation Expectations. 5-10Y Inflation expectations: 3.9%(cons 3.4) in Sep prelim- after 3.5% in Aug. Previously such an upside surprise for long-term inflation expectations would have sparked a market reaction but not this time. We suspect that's after August and less so July preliminary readings were marked lower in the final.

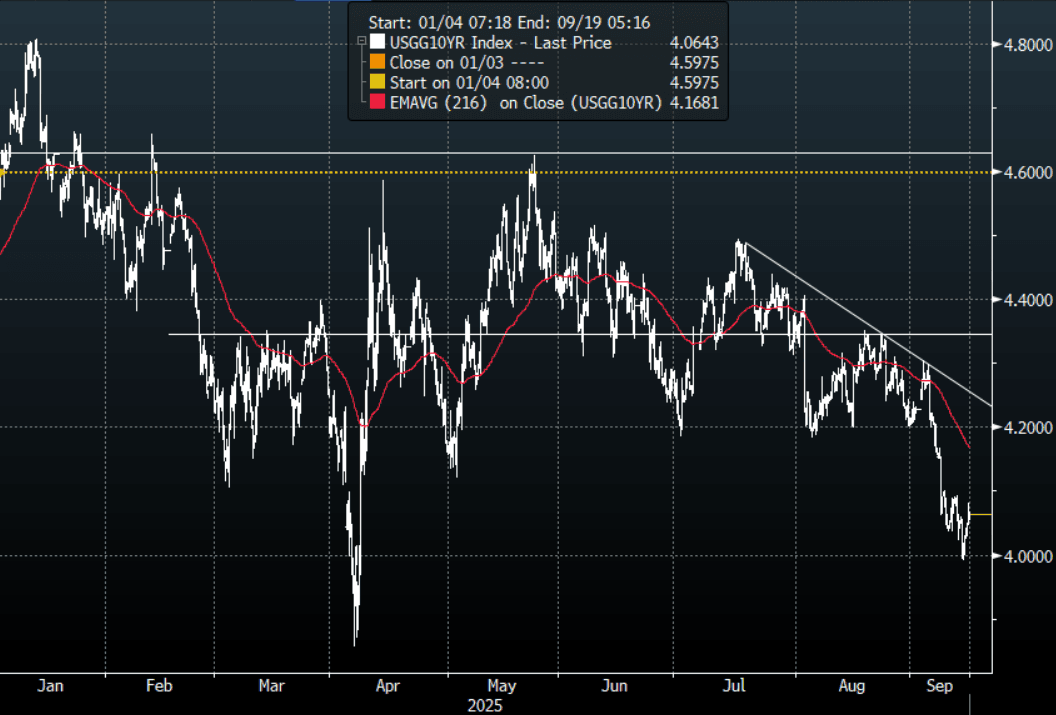

- 10-Year Yields found some supply around 4.00% and have retraced a little as the market looks towards the FOMC this week. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P