IRAN: Snr Official Larijani-Iran Won't Relent Until US Pays A Price

Chair of the Supreme National Security Council, Ali Larijani, posts on X: "Trump returned to say: "We must win this war quickly." But starting wars is an easy matter, whereas ending them does not happen with a few tweets. We will not relent until you admit your mistake and pay the price." Larijani's bellicose comments mirror those from the new Supreme Leader, Mojtaba Khamenei, who issued in a statement earlier today (see IRAN: First Statement From Iranian Supreme Leader Threatens Escalation).

- All public statements and comments from senior figures in the Iranian regime have indicated that Tehran has no intention of de-escalating the situation in the Middle East, with threats that the Strait of Hormuz must remain off limits, that US bases in the region must close, and that it will continue to strike Israel. This has been matched by Iranian action, with commercial ships and tankers set ablaze in the Gulf, and military, civilian, and energy infrastructure targeted across the Middle East.

- Earlier in the week, Ebrahim Zolfaqari, spokesperson for Khatam al-Anbiya Central Headquarters, threatened the US with USD200/bbl oil. Comments from an Iranian foreign ministry spox claiming that ships can pass through the Strait of Hormuz if they coordinate with the Iranian navy are likely to be viewed with extreme caution, given speculation that Iran has laid/is laying mines in the Strait (despite official denials).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Feb12 $1.1750-60(E2.1bln); Feb13 $1.1800(E2.7bln), $1.1850(E3.7bln), $1.1950(E2.2bln)

- USD/JPY: Feb12 Y154.00($1.3bln); Feb13 Y154.00($1.2bln), Y155.00($1.2bln), Y156.00($1.4bln), Y158.50($1.6bln), Y159.00($2.0bln), Y160.00($3.1bln)

- GBP/USD: Feb13 $1.3470-75(Gbp1.0bln)

- EUR/GBP: Feb13 Gbp0.8736-45(E1.0bln)

- AUD/USD: Feb13 $0.6800(A$1.6bln)

- USD/CAD: Feb13 C$1.3770-75($1.0bln)

- USD/CNY: Feb12 Cny6.9000($1.1bln); Feb13 Cny6.9000($1.2bln), Cny6.9700($1.2bln)

US TSY FUTURES: Revisiting Session Highs

Treasury futures are back at this morning's highs, trading desks note heavier buying, appr 30k TYH6 from 112-18 to -18.5, 112-19 last (+13). Extension higher would undermine the bear theme, focus on resistance at 112.-22, the Jan 7 high.

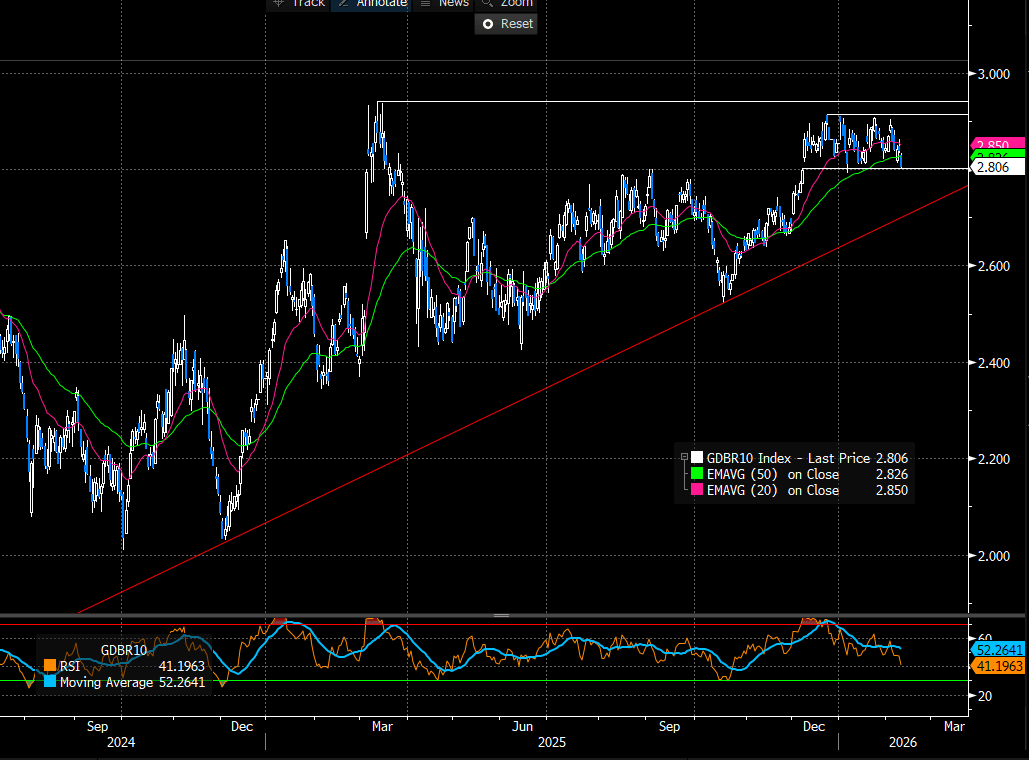

EGBS: 2.80% Contains Downside In 10-year Bund Yields

Downside in 10-year Bund yields has stalled a little around the 2.80% level, keeping the broad 2.80-2.90% range seen since the middle of December intact for now. Bunds face several cross currents this year, with well-documented domestic fiscal/issuance risks potentially offset by lingering geopolitical uncertainty and shifting investor demand patterns (e.g. away from 30-year maturities and towards the 10-15-year segment). Meanwhile, the ECB outlook is broadly steady, with rates set to be in a “good place” at 2% for some time.

- Today’s 3.5bp decline has come despite a heavy sovereign and corporate supply calendar (the EU’s E11bln dual tranche syndication has just priced). Bunds have largely taken cues from global peers, with JGBs stabilising overnight, Gilts benefitting from some near-term political reprieve and USTs supported by a soft retail sales report.

- Earlier today, we highlighted some analyst views suggesting CTA reaction functions were skewed towards fixed income buying, which may be another factor supporting the pullback in global yields.

- Tomorrow’s Eurozone calendar includes syndications from France (30Y) and Slovakia (20Y), alongside conventional issuance from Greece, Germany and Portugal. In data, the ECB’s latest wage tracker is released. President Lagarde noted in last Thursday’s press conference that “Negotiated wage growth and forward-looking indicators, such as the ECB’s wage tracker and surveys on wage expectations, point to a continued moderation in labour costs. However, the contribution to overall wage growth from payments over and above the negotiated wage component remains uncertain.”

- The US labour market report remains the primary global market focus tomorrow.

Figure 1: 10-year Bund Yields (Source: Bloomberg Finance L.P)