EM ASIA CREDIT: SK Telecom: reports of CEO departure

(SKM, A3/A-/A-)

"Chosun Ilbo: SK Telecom CEO Replacement Linked to Hacking Incident" - BBG

Reports of CEO departure ahead of results, negative read.

Korean newspaper The Chosun Daily is reporting that the CEO of SK Telecom may step down, a move related to the April cyber-attack, which the CEO stated at the time was the worst hack in history. The cyber-attack on the 18th April allowed hackers access to 23 servers and millions of subscribers data. SK Telecom's Q3 results are expected tomorrow, with particular attention on any additional costs and business losses related to the breach.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: MNI RBA Preview-Sept 2025: Waiting For More Information

- Download full report here

- The RBA decision is announced Tuesday 30 September and we believe that it will maintain its cautious approach to policy and keep rates unchanged at 3.6% in line with a unanimous Bloomberg consensus.

- Given the Board's data dependency and focus on quarterly CPI data, it is likely to want to wait for Q3 CPI on 29 October and other information before easing again.

- With ongoing significant uncertainty around global growth, rates still considered “restrictive” and domestic activity possibly starting to recover, further cuts remains likely at this stage but the timing has become less clear.

- In August, its projections had trimmed mean returning close to the band mid-point with another 25bp of easing by end-2025. A revised staff outlook is published in November.

BRENT TECHS: (X5) Holding On To Its Recent Gains

- RES 4: $79.16 - 2.618 proj of the Apr 9 - 23 - May 5 price swing

- RES 3: $77.28 - 2.382 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $76.39 - High Jun 23 and a bull trigger

- RES 1: $70.76/71.93 - High Sep 29 / High Jul 30 and key resistance

- PRICE: $69.77 @ 07:12 BST Sep 29

- SUP 1: $64.50 - Low Jun 30 and a key short-term support

- SUP 2: $60.82 - Low May 30

- SUP 3: $58.37 - Low May 5

- SUP 4: $57.81 - Low Apr 9 and a key support

Brent futures traded higher last week and the contract is holding on to its recent gains - for now. The breach does strengthen a short-term bullish theme, however, a break of key resistance at $71.93, the Jul 30 high, is required to signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on support at $64.50, the Jun 30 low. Clearance of this level would reinstate a bearish theme.

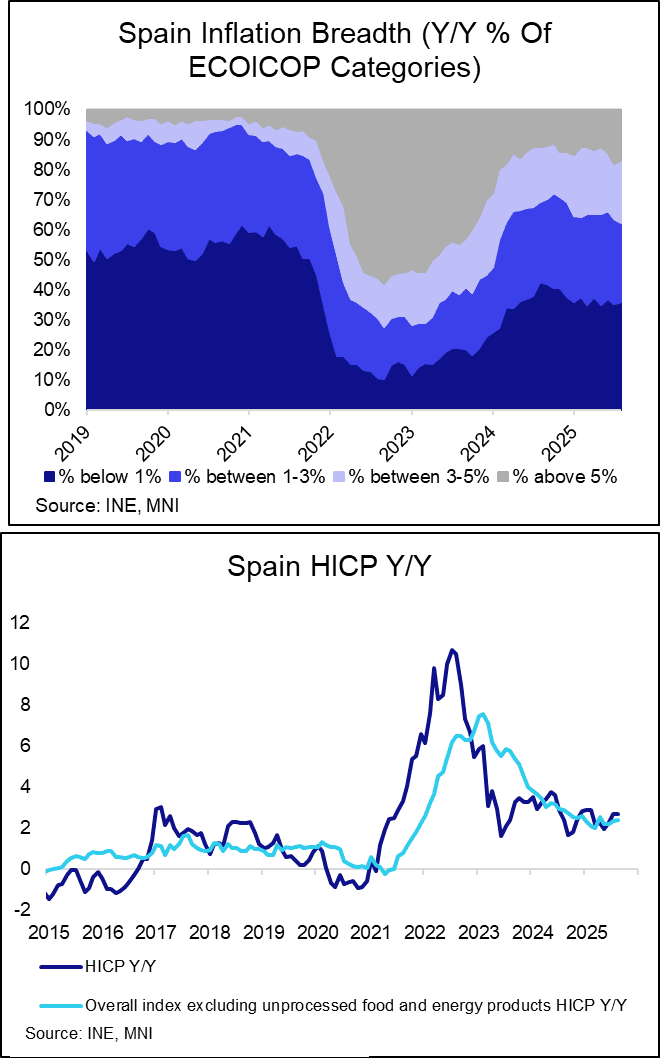

EUROPEAN INFLATION: Spain HICP Preview: Energy Base Effect To Push Headline Up

Spain (12% of EZ HICP in 2025) – 0800BST Monday September 29

- Consensus

- HICP: 3.0% Y/Y 2.7% prior.

- CPI: 3.1% Y/Y vs 2.7% prior (note only 4 estimates at typing)

- Core CPI: 2.5% Y/Y vs 2.4% prior (note only 4 estimates at typing).

- Analyst views:

- Morgan Stanley: “HICP rising to 2.9%Y (from 2.7%Y)”…”Our tracking of utility bills and fuel prices indicate a decline over the month, but they should remain mild compared to last year. Meanwhile, food inflation is likely to stay subdued”…..”Core HICP is expected to ease to 2.6%Y (from 2.7%Y)”.

- Goldman Sachs: “We expect Spanish headline inflation to increase to 2.9%yoy in September from 2.7%yoy in August, and core inflation to tick down to 2.6%yoy”…“ driven by a decline in both year-over-year core goods and services inflation”…“We expect a -17%mom nsa decrease in the package holidays component and a -14%mom nsa print in airfares, unwinding the summer strength, although airport strikes could exert some upward pressure on the component”….”we look for energy inflation to increase to 6.3%yoy from 3.2%yoy in August, driven by a base effect”

- Spanish final August HICP confirmed flash estimates at 2.70% Y/Y (vs 2.70% prior). Excluding energy and unprocessed foods, HICP continued its recent gradual upward trajectory in its third consecutive acceleration, at 2.42 Y/Y (highest rate since April, vs 2.34% prior) on the back of higher services inflation.