US STOCKS: Sizeable Outperformance For Nasdaq, Powell Helps ESA Off Record Highs

- Equities pared losses that were initially seen on hawkish comments from Fed Chair Powell around December rate cut prospects, despite little sign of a reversal of the swift sell off in rates.

- S&P 500 futures trade at 6921 for a ~15pt decline since the FOMC decision but are off earlier lows of 6882.25, limiting the day’s decline to -0.1%.

- They remain close to earlier fresh record highs of 6952.00, close to projected resistance at 6953.25 (2.00 proj of Aug 1-15-20 price swing).

- Nvidia sees large gains of 3.0% as it becomes the first company to top a $5tn market cap. Google follows with a 2.4% gain in what’s been a muted session on net for the remainder of the Magnificent Seven.

- Caterpillar shares are a notable mention as well, jumping 12% in the biggest one-day gain since 2009 after reporting stronger-than-expected earnings on surging demand for its power-generation equipment.

- S&P 500 gains were led by IT (+1.1%), communication services (+1.0%) and energy (+0.8%), whilst losses were concentrated in real estate (-2.7%), consumer staples (-2.0%) and materials (-1.8%).

- Released after the close, Alphabet posted solid looking results, with a Q3 EPS of $2.87 vs estimates of $2.26 and Q3 revenue of $102.35bn vs an estimated $99.85bn. Microsoft meanwhile saw revenue of $77.67bn vs an estimate $75.55bn.

- E-mini comparison: S&P 500 (-0.1%), Nasdaq 100 (+0.4%), Dow Jones (-0.2%) and Russell 2000 (-1.0%)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Northbound

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3968 High May 20

- RES 1: 1.3959 High Sep 26

- PRICE: 1.3920 @ 16:19 BST Sep 29

- SUP 1: 1.3885/3805 Low Sep 25 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

Last week’s rally in USDCAD cancels a recent bearish theme and instead strengthens a bullish outlook. The pair has breached a key resistance at 1.3925, the May 20 high and bull trigger. The breach confirms a resumption of the bull cycle that started Jun 16. This paves the way for a climb towards 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3805, the 50-day EMA.

US PREVIEW: ISM Manufacturing: Prices Paid Seen Diminishing A Bit (2/2)

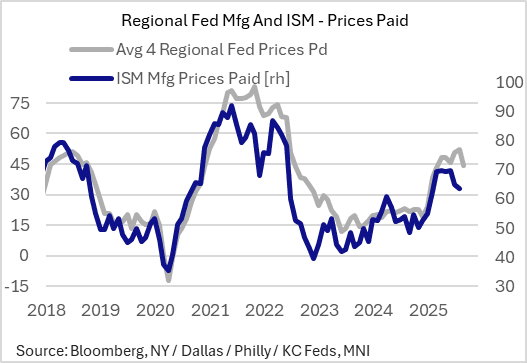

Meanwhile, the ISM Manufacturing Prices Paid gauge is expected to tick down to 62.7 from 63.7 prior. This would mark a second consecutive monthly dip but still keep the prices gauge around the highest levels since late 2022.

- The expectation for a slight downtick in roughly accords with the proxy indicators we have seen.

- September's flash S&P Global PMI report noted "Manufacturing input price inflation remained elevated at one of the highest rates since the pandemic, albeit dipping slightly since August."

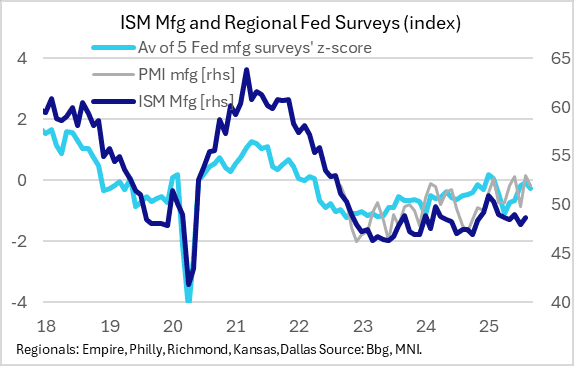

- Regional Fed manufacturing surveys showed pullbacks in NY, Philadelphia, Kansas City, and Dallas (Richmond, which reports % Y/Y changes, was steady).

US PREVIEW: ISM Manufacturing: Marginal Improvement Seen Continuing (1/2)

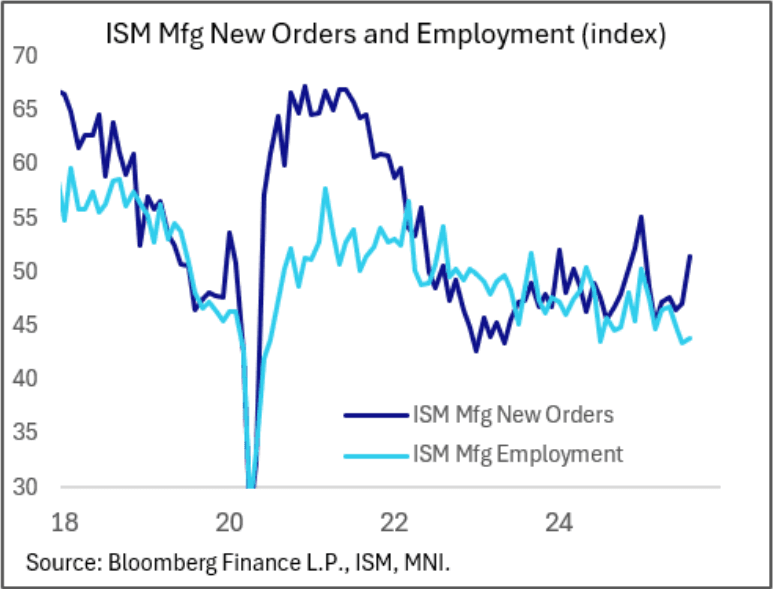

Wednesday's ISM Manufacturing survey (1000ET) is expected to see another rise in the headline index in September, to 49.0 from 48.7 prior for a 2nd successive improvement in activity albeit below the 50 mark for a 7th consecutive month.

- There aren't yet consensus estimates for New Orders (51.4 prior) or Employment (43.8 prior).

- Recall: August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. Overall the ISM survey continues to portray a manufacturing sector that is failing to convincingly regain traction after the summer's tariff-related policy uncertainty. Indeed, tariffs were mentioned extensively in the sector-by-sector anecdotes in the report, and not in a positive light.

- September's flash US PMIs brought a 2-month low for Manufacturing at 52.0 (52.2 consensus, 53.0 prior). That report noted: "Higher output was reported in the manufacturing sector for a fourth consecutive month, but the expansion was much weaker than the strong gain (a 39-month high) seen in August. New order inflows in the goods-producing sector also weakened to only a marginal pace, in part due to an increased rate of loss of exports due to tariffs." The report also reported "lower job gains" in manufacturing in the month, with the sector seeing "more of a focus on job losses due to cost cutting."

- September saw a very mixed round of regional Fed manufacturing surveys: The Dallas, NY, and Richmond Feds saw sizeable pullbacks in current activity vs August, while Philadelphia and KC saw big improvements.