EM ASIA CREDIT: Singapore Telecom: Possible data centre deal

(STSP, A1/A/NR)

"*SINGTEL: ONGOING TALKS IN RELATION TO STT GDC" - BBG

"*SINGTEL: NO CERTAINTY TALKS WILL LEAD TO DEFINITIVE AGREEMENT" - BBG

Singtel confirms talks on USD5bn data centre deal, asset sales likely limits risks

Singtel has responded to a Reuters story linking Singtel and KKR to a bid for ST Telemedia Global Data Centres, with the deal reportedly valued at SGD 5bn (around USD 3.8bn). KKR and Singtel currently own approximately 14% and 4% stakes in ST Telemedia, respectively. Separately, Singtel is said to be considering a partial sale of its Bharti Airtel stake (c. USD1.2bn), which could help fund the data centre acquisition. Singtel’s market capitalisation is about SGD 74bn (USD 57bn), and with expected asset sales, the transaction would likely be rating neutral.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Smooth Digestion Of Mar-36 Supply With More Demand

The latest ACGB Mar-36 auction saw strong demand, with the weighted average yield coming in 0.22bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions.

- Moreover, the cover ratio nudged higher to 3.4917x from 3.3111x.

- As highlighted in our preview, bidding at today’s auction faced an outright yield that was roughly 10-15bps higher than the previous auction level and about 20bps below the late February peak.

- However, the 3/10 yield curve was slightly flatter than the previous auction level and sat 30-35bps flatter than its recent high.

- There has been no material movement in XM or the cash line in post-auction trading.

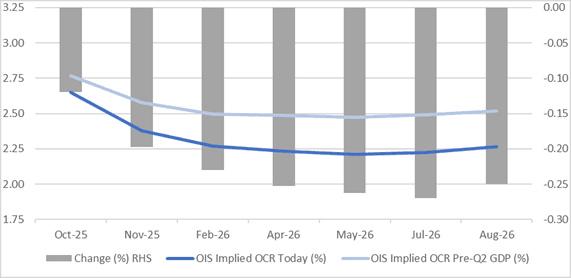

STIR: RBNZ-Dated OIS Set To Move After Today’s RBNZ Decision

RBNZ-dated OIS pricing is slightly firmer across meetings today ahead of today’s RBNZ Policy Decision.

- Easing expectations show 36bps of easing priced for today’s meeting, with a cumulative 63bps by November 2025 and 73bps by February 2026.

- Today’s decision is likely to have a material impact on pricing. A 50bps cut could bring forward the full 75bps of cumulative easing to November, while a 25bps cut would likely push at least half of that 25bps into early 2026.

- Notably, pricing is 12-27bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

AUSSIE BONDS: ACGB Mar-36 Auction Result

The AOFM sells A$1200mn of the 4.25% 21 March 2036 bond:

- Average Yield (%): 4.3788 (prev. 4.2569)

- High Yield (%): 4.3800 (prev. 4.2600)

- Bid/Cover: 3.4917x (prev. 3.3111x)

- Allotted at Highest Accepted Yld as % of Bid at Yld (%): 84.6 (prev. 24.0)

- Bidders: 41 (prev. 33), successful 17 (prev. 16), allocated in full 9 (prev. 13)