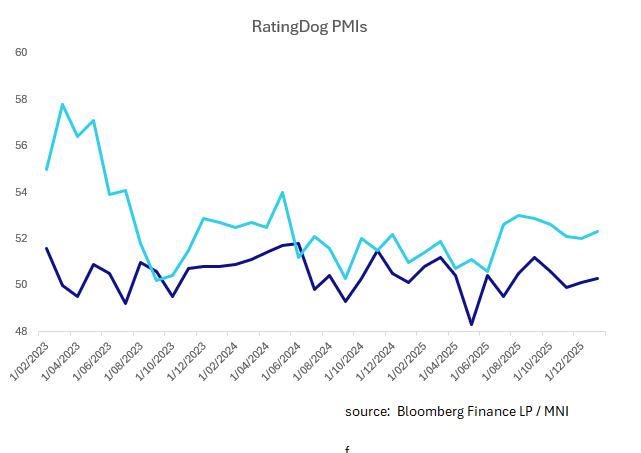

CHINA: Services PMI Up, Supports No Rush for Monetary Policy Moves

- The RatingDog China Services PMI increased to 52.3 in January 2026 from 52.0 in December, marking the strongest expansion in services activity in three months and the 37th consecutive month of growth.

- Stronger new business, including a rise in new export orders contributed to the upturn, leading services firms to increase staffing levels for the first time since July 2025

- The result is a modest respite for authorities given the multi decline in house prices and recent volatility in equities and commodities.

- The result follows Monday's RatingDog China Manufacturing January release which saw a modest improvement to +50.3 (prior +50.1).

- This sees the composite up to +51.6, its highest in 3 months.

- There appears no immediate pressure for monetary policy intervention. News reports of the interest rate on MLF hitting new lows, supports lending and is consistent with the view of incremental changes to support the transfer mechanism for rates instead of an imminent rate cut.

- CGB 10-Yr has edged lower in yield today, currently at 1.805%. Leading into Lunar New Year, could test 1.80% as liquidity is added to support markets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

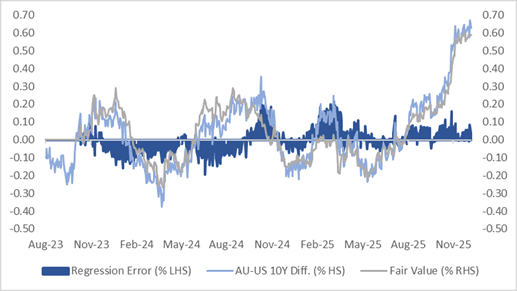

AUSSIE BONDS: AU-US 10Y Differential Remains At Cycle Highs

The cash 10-year ACGB is dealing 1bp richer today, but with the AU-US 10-year yield differential at +64bps.

- At this level, the differential sits around its cycle high, the widest since mid-2022.

- December’s price action has consolidated the differential’s breakout above the ±30bps range that had prevailed since November 2022.

- This widening has occurred alongside a steady increase in market-implied expectations for the RBA cash rate.

- However, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) spread over the past two years suggests the current differential is around 4bps above regression fair value (see chart).

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Bloomberg Finance LP / MNI

CROSS ASSET: Oil Dip Supported, Venezuelan Leader Vows Cooperation With US

The early softness in oil prices proved to be short lived, after opening lower, we sit back close to $61/bbl in latest dealings (session lows at $60.00/bbl). The market is likely not expecting much higher oil supply in the near term, while better equity sentiment and higher metals may be driving some positive spillover for oil as well. Comments have crossed from US President Trump around Venezuela, which largely re-iterate weekend comments. He added there is no need for a second round of military action and that the focus is on getting more oil out of the country (although no time line was given). Venezuela's Rodriguez also spoke and she invites the US government to work together (to form agenda for cooperation) - these comments appearing more conciliatory than other remarks made by Venezuelan officials in recent days.

- Trump also stated something has to do done about Mexico and the strong drug inflows to the US. USD/MXN is around session highs at 17.96/97 but remains within recent ranges.

- Elsewhere in the FX space, the USD is slightly higher, the BBDXY index back close to 1206. USD/JPY has risen back through 157.00, reversing the earlier risk off tone. Still, AUD and NZD are holding modest losses, despite a generally positive equity mood, led by the tech side. Most USD/Asia pairs are also higher.

- Precious metals are also higher, up +1.65% for gold, through $4400, while silver is around 4% higher, not really impacted by the firmer USD tone, or higher equities. Copper is also tracking higher

- US Tsy yields are down a touch. 10yr outright last around 4.18%.

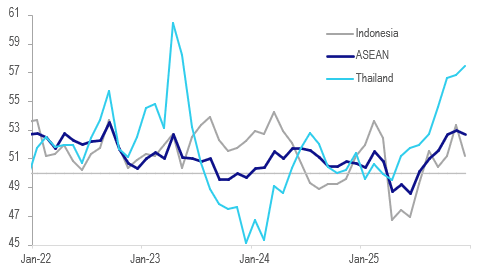

ASIA: Stronger ASEAN Manufacturing Into End 2025 Led By Thailand

December manufacturing PMIs across Asia showed that the sector saw stronger or steady activity with all countries at the 50-breakeven level or above. The ASEAN aggregate moderated to 52.7 from 53.0 but continued to show growth in the sector driven by output and domestic orders but export orders remained weak. Confidence in the outlook rose to a 10-month high. The Q4 average PMI was almost 2 points higher than Q3 signalling activity improved into year end.

- ASEAN outperformed northern Asia in December, which recorded outcomes around 50, while Thailand outperformed the region as a whole.

- The S&P Global Thai manufacturing PMI rose to 57.4 from 56.8, the strongest growth in activity since May 2023. The index trended higher over 2025 with the Q4 average at 56.9 up from Q3’s 53.1. Strong domestic new orders growth following increased marketing and improved “underlying demand conditions” which boosted production and as a result an increase in purchasing. This suggests that the Bank of Thailand’s 100bp of easing in 2025 may be have an effect.

- Despite strong manufacturing growth there wasn’t a pick up in hiring in fact it contracted slightly after increasing since March, which added to backlogs.

- Export orders remained weak recording the fifth consecutive monthly contraction. Increased US trade protectionism has distorted global trade trends.

- Cost inflation rose driven by raw materials and intermediate goods but Thai manufacturers reduced selling prices slightly to boost demand.

- The rest of ASEAN is more lacklustre with Indonesia, Vietnam and Myanmar recording falls but remaining above 50, while the Philippines and Malaysia are around breakeven.

ASEAN S&P Global manufacturing PMI sa