CHILE: September Nominal Wages Due, USDCLP Bearish Trend Intact

- The Chilean peso has opened moderately firmer on Thursday, as the broader dollar rally that has been playing out following the FOMC is showing signs of fatigue, with USDCLP edging down by 0.3% to 941.

- The trend condition in USDCLP remains bearish and an extension lower would open 922.67, the Jul 2 low and a key support. On the upside, key short-term resistance is seen at 953.11, the 50-day EMA.

- On the data front today, nominal wage figures for September cross at 1200GMT(0700ET). Wages rose by 6.1% y/y in August, moderating from 6.4% in July. After today, attention turns to tomorrow’s October CPI inflation data which the central bank will be watching closely amid its concerns over the persistence of core inflation pressures. The headline rate is expected to return to within the 2-4% target range, while core CPI is seen edging down from 4.0%, keeping the door open to a possible rate cut in December.

- Sept. Nominal Wage YoY, prior 6.1%

- Meanwhile, the Treasury will sell bills due 2026, peso bonds due 2035 and UF notes due 2028 in a local bond auction today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Legal Expert On Potential Changes To BoE Remuneration On Reserves

An expert House of Lords witness talks about the legality of adjusting the BoE's remuneration on reserves -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.

PIPELINE: Corporate Bond Roundup: Bank of England 5Y on Tap

- Date $MM Issuer (Priced *, Launch #)

- 10/07 $Benchmark Bank of England 5Y +8a

- 10/07 $Benchmark CPPIB 3Y SOFR+39

- 10/07 $Benchmark Angola +5Y 9.75%a, 10Y 10.5%a

- 10/07 $Benchmark Türkiye Garanti Bankası 10.5NC5.5

- 10/07 $Benchmark JDC Dev Bank Kazakhstan +5Y, KZT 3Y investor calls

- Expected Wednesday

- 10/08 $1B Kommunalbanken Norway WNG 3Y SOFR+37

- $9.9B Priced Monday

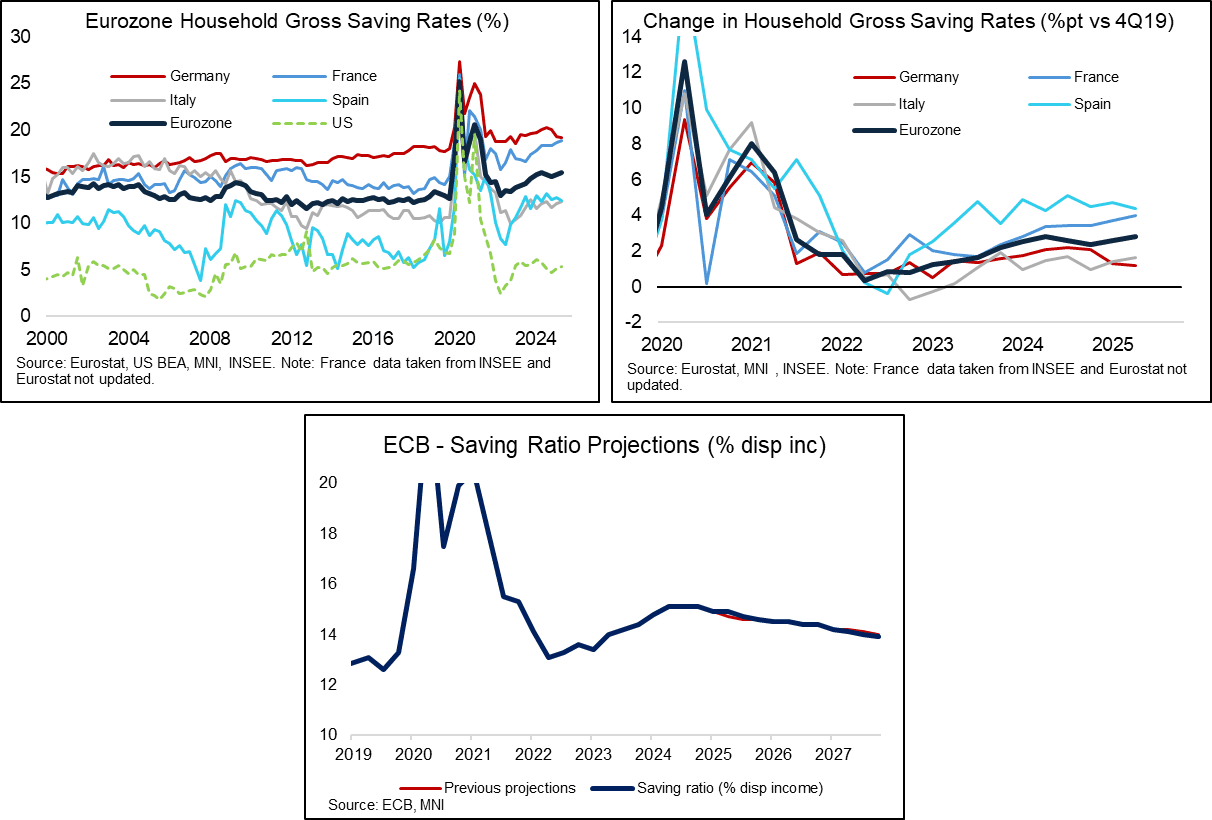

EUROZONE DATA: Q2 Savings Rate Exceeds ECB Projections; France Drifting Higher

The ECB expects higher real disposable incomes and a gradually declining savings ratio to strengthen private consumption in the coming years. In Q2, the household savings rate was estimated at 15.4%, above the ECB’s 14.9% projection and up from 15.2% in Q1. While a slow-moving train, a persistently elevated savings ratio is a dovish input for the ECB’s reaction function, both cyclically (i.e. via lower household consumption outturns) and structurally (i.e. via a lower neutral rate). In the near-term, the case for another rate cut to 1.75% will probably need to be motivated by higher frequency data (e.g. PMIs, inflation), but developments in the savings rate may push against early expectations for a rate hike over the next few years (against a backdrop of higher German fiscal spending).

- Across countries, the savings ratio ticked lower in Germany (19.2% vs 19.3% in Q1, 20.1% in Q4 and 20.2% in Q3) and Spain (12.4% vs 12.8% in Q1). Meanwhile, increases were seen in Italy (12.3% vs 12.1% in Q1) and France (18.9% vs 18.6% prior).

- France has displayed the clearest upward drift in the savings rate in recent quarters, an unsurprising development given ongoing political and fiscal uncertainty. With ex-PM Lecornu’s resignation keeping these risks elevated, and more fiscal consolidation required as part of any budget compromise, it’s hard to envisage a meaningful reversal in this trend anytime soon.

- For comparison, the US savings rate of ~5% remains significantly below that of the Eurozone. That’s in fitting with historical precedent, but Eurozone consumers have had plenty of reasons to remain cautious post-covid (e.g. proximity of the Russia/Ukraine conflict and the related spike in energy prices).

- We wrote more on Eurozone consumption, the savings ratio and related ECBspeak a few weeks ago.