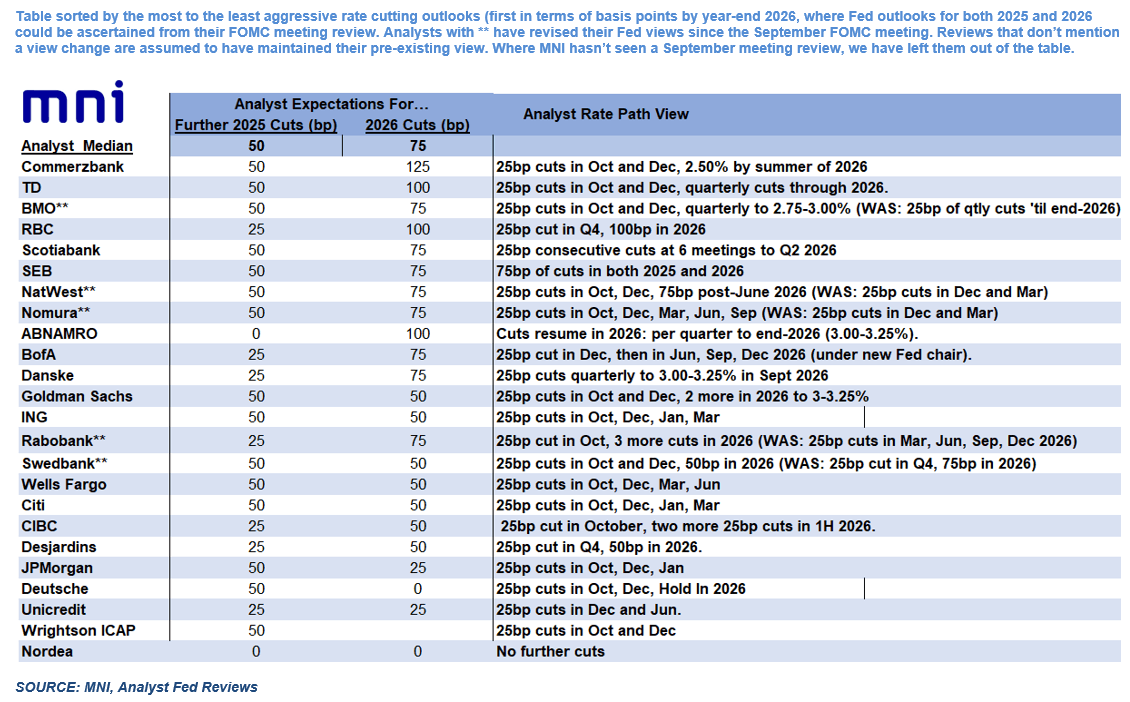

FED: September FOMC Spurs Analysts To Expect More Easing (1/3)

We've seen a few analysts change their house views on the path of Fed rates since Wednesday's FOMC meeting. These are all in a more dovish direction, with the most common change being a more front-loaded easing cycle expected than previously. We go through the revisions in a subsequent note. The table below summarizes current views, to the best of MNI's knowledge.

- Analysts' views for further cuts this year range from zero to 50bp, with the median analyst seeing 50bp (Oct and Dec cuts), aligning with the FOMC's latest Dot Plot. This is an increase in the median seen in our Fed preview which saw an even split between 25 and 50bp of further cuts beyond October.

- At the same time, the forecast revisions have tipped the median toward seeing slightly more 2026 cuts vs pre-meeting: now 75bp (albeit it's still almost an even split between the number of those seeing 50 and those seeing 75bp), vs 50bp median pre-meeting.

- Median total further easing between now and end-2026 is 100bp, ranging from zero to 175bp.

- MNI's review of the September FOMC is here (PDF).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

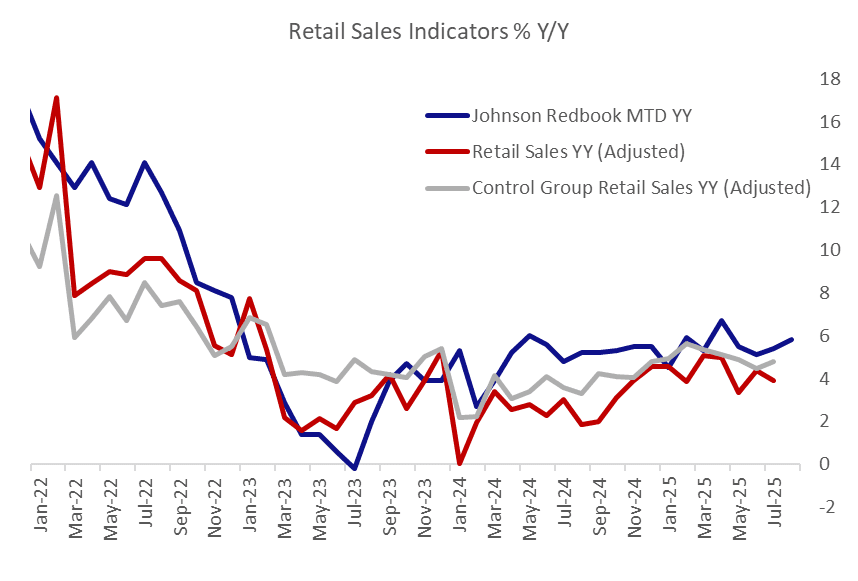

US DATA: Redbook Retail Sales Remain Solid Through Mid-August

Retail sales as measured by the Johnson Redbook index rose 5.9% Y/Y in the week ending August 16, up from 5.7% the prior week and bringing the month-to-date rise to 5.8%.

- That's very solid outright, albeit somewhat below retailers' targeted 6.2% gain. Per the report's anecdotes: "Early back-to-school sales results have generally fallen short of expectations. Some markets, particularly in the Midwest and Southeast, have already begun their back-to-school season, while others have not yet started. Additionally, the tail-end of state tax-free holidays in Florida, Maryland, Massachusetts, Ohio, and Texas has contributed to increased traffic and sales. Due to regional differences in school calendars and variations in merchandising schedules, the rollout of new seasonal programs has varied from store to store; it is still too early to gauge consumer reactions to these programs. Many major retailers are set to report their second-quarter earnings this week and next week, which may provide insights into how tariffs are affecting value-conscious consumers and consumer spending overall."

- On a Y/Y basis, Census Bureau retail sales came in at 3.9% overall in July, down from 4.4% prior, though control group sales picked up to 4.8% from 4.5%. While the Johnson Redbook has tended to "over-estimate" Census Bureau sales on this basis, sustained growth continues to suggest solid consumption dynamics through the middle of Q3 (with the usual caveat that these are in nominal and not price-adjusted terms).

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Aug21 $1.1600(E1.3bln), $1.1700(E1.6bln), $1.1750(E2.0bln), $1.1800(E3.0bln); Aug25 $1.1640-55(E2.0bln)

- USD/JPY: Aug21 Y145.95-00($1.2bln), Y146.70-80($1.8bln); Aug22 Y147.90($1.4bln)

- AUD/USD: Aug21 $0.6590-00(A$1.8bln); Aug25 $0.6510-25(A$1.1bln)

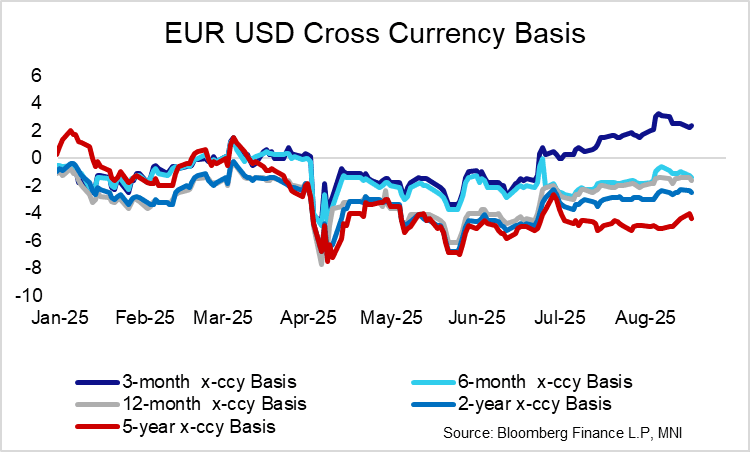

BASIS: 3-month EUR/USD X-ccy Basis Has Diverged From Longer Tenors

3-month EUR/USD x-ccy basis has drifted into positive territory since the end of June, currently just over 2bps and visibly diverging from 6/12-month (and longer) tenors. This divergence suggests short-term funding dynamics are likely at play (i.e. more demand for EUR funding vs USD funding on the margin).

- The divergence has notably aligned with the latest raising of the US debt ceiling, which appears unintuitive since the resulting TGA rebuild is expected to sap USD liquidity from the market (and hence filter be reflected in a wider basis in USD’s favour).

- However, we’ve highlighted in recent posts that despite the ongoing TGA rebuild, bank reserve balances remain relatively steady around $3.3trln. That may be averting concerns around near-term USD funding pressure (though September quarter end will be a more important time to monitor these dynamics).

- Bill issuance related to the TGA rebuild is instead being absorbed through reduced ON RRP usage. It’s possible that some hedging dynamics amongst foreign repo agents have shifted during this process, which may be feeding through to the front of the x-ccy basis curve, but it’s difficult to find concrete evidence in favour of such an argument.

- Instead, some desks have highlighted recent increases in demand for long EUR spot positions, which need to be funded on an overnight basis and are consequently pushing up relative EUR funding costs.

- Danske Bank have written that “the market seems to extend the experience from last year, where trading over year-end in XCCY basis was smooth sailing, with tranquil credit markets and still overall relatively easy liquidity conditions. While this may be the right call, the outcome space, based on historical evidence, looks quite asymmetric. There is limited room for further tightening of basis over year-end, while plenty of room for a widening, should a shock hit the market, e.g. a sudden deterioration of risk sentiment and widening of credit spreads”

- They go on to note that “we think the EFFR-ESTR pricing for the rest of the year looks about fair and considering the tight basis over year-end, we see a good case for EUR-denominated investors hedging USD-assets extending maturing EUR/USD FX swaps over year-end”.