EM CEEMEA CREDIT: Seplat Energy: Outlook to Positve at S&P

Nov-19 08:44

(SEPLLN; B2/B/B)

- Not a surprise, Seplat Energy’s rating outlook has been changed from stable to positive by S&P aft-mkt close y’day. This follows the change in outlook to positive for Nigeria’s sovereign ratings over the weekend. In secondary markets, our screen feeds show SEPLLN 9.125 Mar30 charting at 8.40% or z+500bp area, near the local lows (source: Bloomberg).

- In its rationale, the rating agency cites the cap to single-B on the back of geographical concentration, as the Co. operates exclusively in Nigeria. The one notch uplift vs sovereign relies among other factors on Seplat Energy’s “policy of holding at least 70% of cash in hard currency and at least 70% of that offshore”.

- On a standalone basis, the agency expects credit metrics to remain broadly stable, with EBITDA of USD 1.2bn to 1.4bn over ’25-’26 under a base case assumption of Brent at $60/bbl. See link to our earlier Q3 earnings analysis: https://mni.marketnews.com/4hAb0Rb.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: Cash Basis Trade

Oct-20 08:25

Bund Basis trade, suggest Cash seller:

- RXZ5 7k at 129.83.

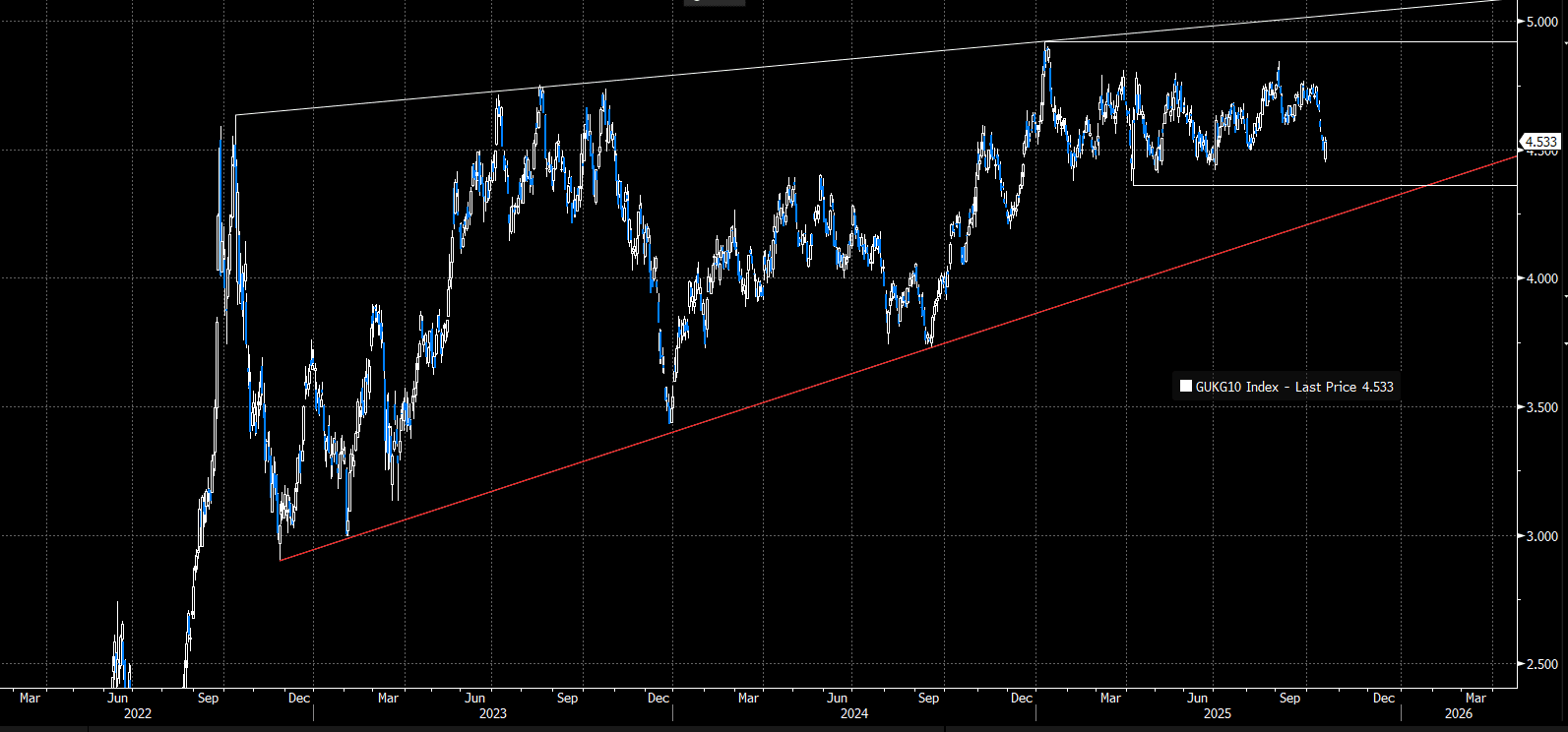

GILTS: Steady Open; Trend In 10-year Yields Still To The Upside

Oct-20 08:22

A fairly steady open for Gilts ahead of an important week for UK data. Futures are -4 ticks at 92.42. A short-term bull cycle in futures remains intact though, with initial resistance at Friday’s high of 93.17.

- Yields are up to 1bp higher across the curve. 10-year yields are currently 4.536%, down from this month’s 4.758% high. Despite this month’s fall in yields, the medium-term trend for the 10-year is still to the upside. Initial support is the April 7 low at 4.363%, which shields trendline support drawn from the November 2022 low at 4.232% today.

- See MNI’s Tech Trend Monitor for more, which also includes charts on the 30-year Gilt yield.

- Fiscal policy remains a key focus for the Gilt market ahead of the Nov 26th budget. The main fiscal headlines from the weekend have suggested that VAT may be removed from energy bills.

- September public sector finance data is due on Tuesday. After correcting for a VAT error in last month’s release, PSNB is currently tracking GBP9.4bln below the OBR’s forecast year-to-date.

- This release, alongside Wednesday’s CPI report (important for the near-term BOE outlook) will feed into the OBR’s Round 3 forecast on October 31 ( see here for more).

Figure 1: 10-year Gilt Yields (Source: Bloomberg Finance L.P)

FOREX: FX OPTION EXPIRY

Oct-20 08:14

Of note:

USDJPY ~2bn at 150.00/150.05.

EURUSD ~1bn at 1.1700 (tue).

NZDUSD 1.1bn at 0.5700 (wed).

AUDUSD 1.49bn at 0.6450 (fri).

- EURUSD: 1.1645 (665mln), 1.1650 (331mln), 1.1670 (211mln), 1.1700 (346mln), 1.1705 (206mln), 1.1715 (740mln).

- USDJPY: 150.00 (1.28bn), 150.05 (823mln), 150.25 (600mln), 150.50 (355mln), 151.00 (779mln), 151.70 (1.1bn).

- USDCAD: 1.4000 (718mln).

- AUDUSD: 0.6500 (340mln).

- AUDNZD: 1.1325 (400mln).